Month’s Highlights

- Moody’s raised concerns over the considerable interest payments Central Bank of Kenya (CBK) has been offering to treasury bond investors. Between July and September 2020, investors have been offered Treasury Bonds worth KSh 220 Billion. Average interest rates offered have been rising from 10.26% to 11.87%. The amount of Treasury Bills auctioned is enormous, at 8.7 % of GDP. This leaves Kenya vulnerable to a rise in its borrowing costs. Government debt levels have risen from KSh 5.8 trillion in July 2019 to KSh 6.7 trillion as of 20 June 2020. Moodys is recommending that the state embarks on a credible fiscal consolidation plan that will determine its ability to contain any rise in borrowing costs and liquidity or rollover risk.

- Treasury plans to target KSh524.69 billion in fresh debt from domestic investors, 6.0% more than the KSh494.98 billion it had estimated at the beginning of the financial year in July. Mr Yatani has this month cut the total tax collection forecast for this financial year ending June 2021 by KSh91.2 billion to KSh1.42 trillion compared with his earlier estimates of KSh1.51 trillion in June because of persistent adverse effects of the Covid-19 pandemic on economic activity. It is also expected that the government to continue to rely more on longer-term debt issuance rather than Treasury bills due to the flattening of the yield curve.

- KRA lost track of Sh896bn in wired offshore wealth. The KRA records show 3,543 Kenyans repatriated Sh118 billion as of August 30. The applicants took advantage of the three-year amnesty window to repatriate the billions tax-free in a period when they were not required to declare the source of their wealth or even account for previous years’ tax arrears. The amnesty, which was announced in 2016, was aimed at attracting wealthy Kenyan investors who had opted for offshore investments in an attempt to mask the source of their wealth.

- Tanzania, Rwanda and Uganda are proceeding with plans to electronically interlink their respective stock exchanges, leaving out the Nairobi Securities Exchange(NSE). Equity investors in Tanzania, Uganda, and Rwanda will be able to trade shares of any firm listed in any of these countries without going through different stockbrokers.

- The Kenya Bankers Association’s 9th Annual Banking Research Conference kicked off under the theme Banking and Social Development: Market Structure, Behavioural Evolution, and Financial Sector Dynamics. The papers presented shared a wide range of insights on how the banking industry’s structure – along with the behavioural dynamics of non-financial economic agents’ expectations – influence credit pricing in the economy. The presentations further examined how the structure of the banking system impacts credit allocation and pricing.

- Uganda and French oil conglomerate Total have inked a deal that will open the way for construction of an oil pipeline to neighbouring Tanzania. The proposed 1,445-km (900-mile) East African Crude Oil Pipeline, costing US$3.5 billion, is expected to pass through neighbouring Tanzania to the Indian Ocean port of Tanga. Kenya is still stuck in squabbles with UK-based Tullow over taxation and other incentives with Tullow threatening to quit oil exploration in Turkana. Tullow has since lifted the freeze it had placed on the oil exploration project.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 3.75% to stand at USD 8.63 billion(5.23 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

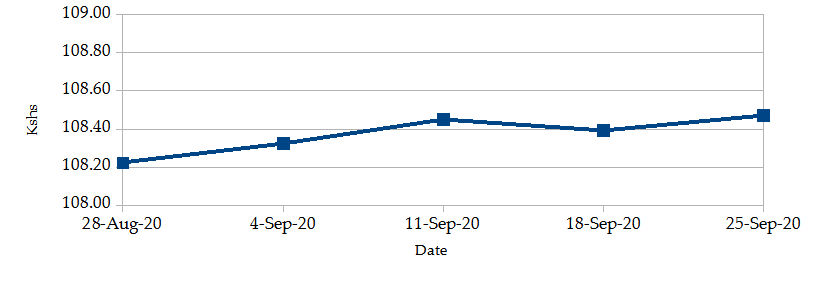

Currency

The Kenyan Shilling remained relatively stable against the USD, declining marginally by 0.30%, exchanging at Kshs 108.47 at the end of the month up from Kshs 108.15 in the previous month. There has been a slower spread of the Covid-19 pandemic reported which may be improving investor sentiment in the market.

USD Vs KSHS

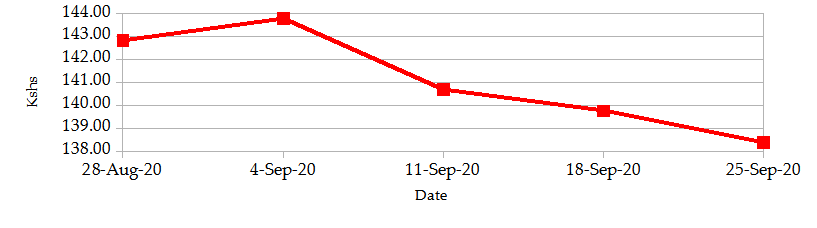

The Kenyan Shilling remained gained against the Sterling Pound, gaining by 2.68%, exchanging at Kshs 138.38 at the end of the month down from Kshs 142.20 in the previous month. This may be due to the resurgence of the Covid pandemic in the European region.

STERLING POUND Vs KSHS

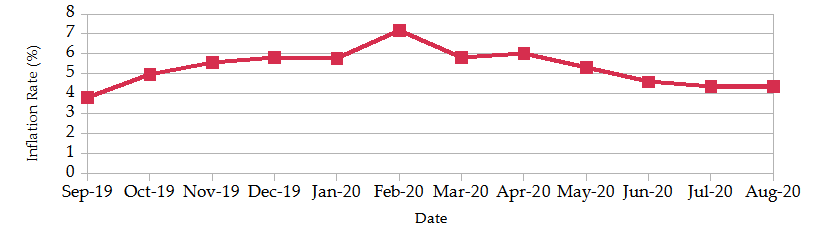

Inflation

The overall year-on-year inflation held at 4.36% in the month of August from a revised figure of 4.36% in July. The intensification of measures taken to curb the spread of Covid-19 has resulted in an easing of the downward pressure on the CPI. The food and non-alcoholic index fell by 1% even as food year-on-year inflation rose by 5.43% in August.

INFLATION EVOLUTION

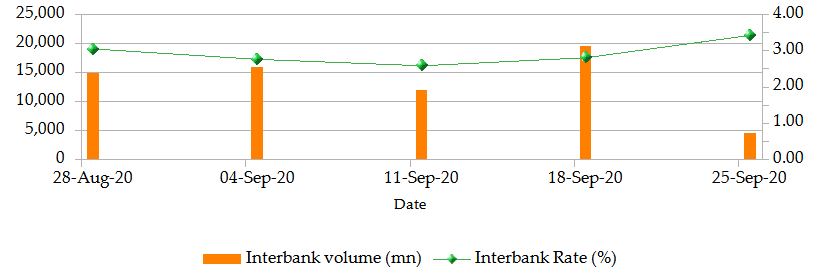

Liquidity

During the month, liquidity decreased as a result of tax remittances which more than offset government payments. The inter-bank rate increased to 3.27% up from 3.01%. The volume of inter-bank transactions decreased from Kshs 16.52 billion to Kshs 10.35 billion. Commercial banks’ excess reserves decreased to Kshs 14.10 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

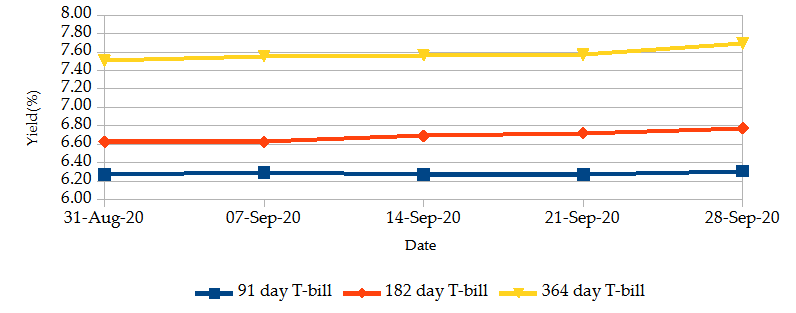

T-Bills

The T-bills recorded an overall subscription rate of 54.40% at the end of September, compared to 52.33% recorded in the previous month. The under-subscription is partly attributable to lower liquidity in the money market and investor preference for Treasury bonds which have higher yields. The subscription rate of the 91-day, 182-day and 364-day papers stand at 101.2%, 34.9% and 55.2% respectively. On a monthly basis, the yields on the 182-day and 364-day papers increased by 2.23% and 2.44% respectively to 6.77% and 7.69%. On the other hand, the yield on the 91-day paper remained relatively unchanged at 6.31%.

T-BILLS

T-Bonds

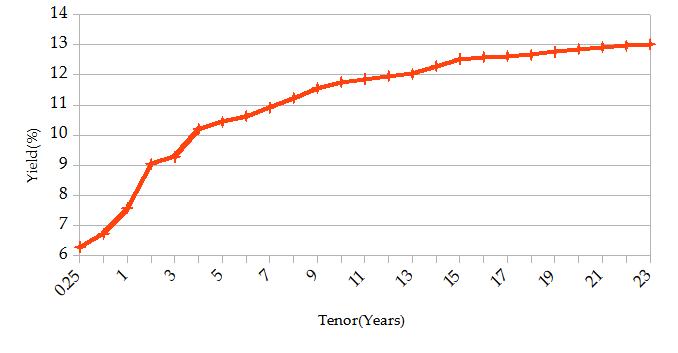

For the month of September, the government has floated triple issues, namely, FXD2/2010/15, FXD1/2020/15 and FXD1/2011/20 with effective tenors of 5.3, 15.3 and 11.3 years respectively, for a total value of Kshs 50bn for budgetary support. The bonds have coupon rates of 9.0%, 12.8% and 10.0%, respectively with the period of sale set to end on 21 September 2020.

At the end of September, the T-Bonds registered 1,895 bond deals valued at Kshs 81.39 billion. This represents a monthly decrease and increase of 4.53% and 38.05% respectively. The yields on government securities in the secondary market remained relatively stable in September.

In the international market, yields on Kenya’s Eurobonds increased by an average of 74.9 basis points.

YIELD CURVE

EQUITIES

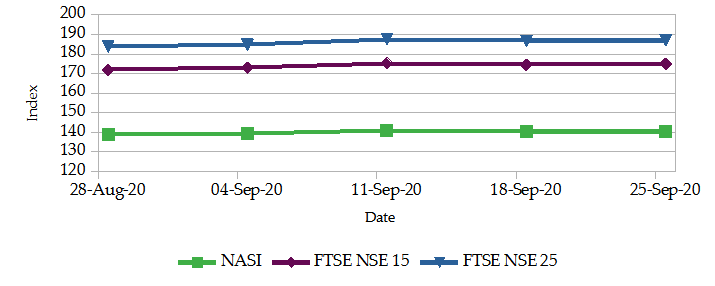

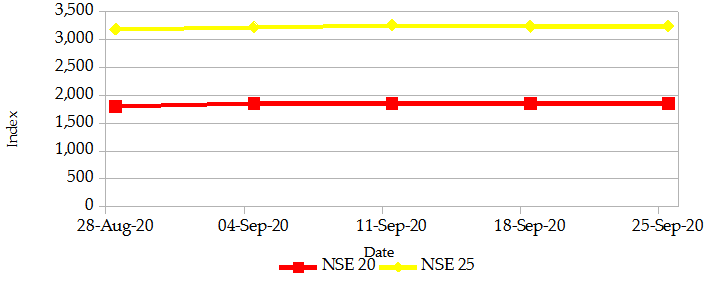

During the month of September, the market capitalization rose by 1.18% to Kshs 2.16 trillion. However, total shares traded and equity turnover plunged by 21.4% and 25.0% respectively to 20 million shares and Kshs 501million. NASI and NSE 25 gained by 1.2% and 1.7% in that order, and NSE 20 gained by 3.00% on a monthly basis. On a weekly basis, the NASI and NSE 25 gained by 0.09% and 0.11% respectively and NSE 20 gained by 0.01%. The gain in NASI is a result of the appreciation of large-cap stocks such as Equity Group, KCB Group and Co-operative Bank.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25TS

ALTERNATIVE INVESTMENTS

- During the last week of the month, the I-REITs market recorded a turnover of Kshs 2.9million with 121 contracts. The Derivatives market registered a turnover of Kshs 596,150 with 19 contracts.

- Rwanda’s Kasha, a multicategory retailer of women’s products, raised $1 million in a Serie A funding round from the United States Development Finance Corporation (DFC), as part of the development bank’s $3.6 billion disbursements to advance development in emerging markets.

- Nigeria’s Airsmat, an AI-enabled software provider for drone data management raised $0.1 million in seed funding from Zetogon. The company will use the funds to support the launch of its flagship product SmatCrows, which will debut in October in Nigeria and launch in Q2 2021 in other African countries.

- Egypt’s Anubis Gaming raised $0.3 million in seed funding by China Renaissance Group, and Loyal Valley Capital among other investors, bringing its total raised funding to $0.45 million. The e-sports players organization startup that participates in video game tournaments plans to use the funding to recruit more players and form new teams, launch their apparel line, and add an international coaching staff.

- Platform Capital (Platform), a leading growth markets investor, is pleased to announce its investment in Big Cabal Media (BCM), a leading digital media publisher in Africa, operating out of Nigeria.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -1.43% | -6.73% |

| STOXX Europe 600 | -3.60% | -3.60% |

| Shanghai Composite (SSEC) | -3.56% | -5.42% |

| MSCI Emerging Market Index | -4.58% | -5.69% |

| MSCI World Index | -2.86% | -6.37% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -0.32% | -0.49% |

| JSE All Share | -1.97% | -36.53% |

| NSE All Share (NGSE) | 2.92% | 3.99% |

| DSEI (Tanzania) | -0.25% | 0.98% |

| ALSIUG (Uganda) | 0.64% | 1.95% |

- During the month, major global markets declined driven in part by the resurgence of the COVID-19 pandemic in Europe. In the USA, the S&P 500 and Dow Jones indices plunged by 6.73% and 5.92% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and UK’s FTSE 100 declined by 3.60% and 2.03% respectively.

- On a regional front, most markets were on an upward trend as Tanzania, Rwanda and Uganda proceeded with plans to electronically interlink their respective stock exchanges. The FTSE ASEA Pan African index, representing the overall African markets, dropped by 0.49% from the month of August. South Africa’s JSE All Share plunged by 36.53%, Nigeria’s All-share index rose by 3.99% and Tanzania’s DSEI increased by 0.98%. Also, Uganda’s All Share Index increased by 1.95%.

- On the global commodities markets, the oil futures indices declined, in part due to the impact of the coronavirus-related lockdowns in Europe raising expectations for weaker energy demand. The Crude Oil WTI futures plunged by 6.33% from the previous month of August. However, the ICE Brent Crude Oil increased in value by 27.90% amid hopes that the US Congress will resume discussions over a new stimulus deal.

- Gold reported a significant drop in price as the dollar continued to rise amid concerns about the second wave of the Covid-19 pandemic in most parts of Europe. The rising cases in Europe and the USA have unsettled investors about the global economic recovery, driving investors into dollars. Additionally, investors have also unwound some of their gold holdings as part of equity market turbulence this week, which added to the pressures around the commodity. Some bond investors who switched to gold and stocks are now reinvesting in bonds in small amounts, expecting bond yields to rise in the final quarter of the year.

Get future reports

Please provide your details below to get future reports: