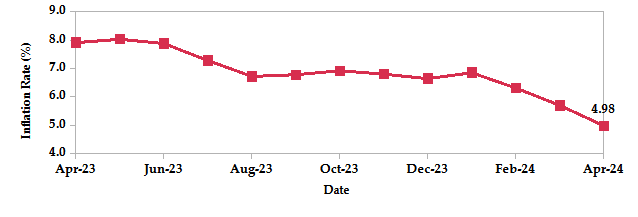

Inflation declined to 4.98% in April 2024 from 5.70% in March. This was primarily driven by lower food and fuel prices. The food and non-alcoholic beverages index declined to 5.6% from 5.8%, attributed to lower food prices. The housing, water, electricity, gas and other fuels index decreased to 3.8% from 8.0%, mainly due to lower electricity costs and pump prices. Furthermore, the transport index decreased to 9.2% from 9.7%.

The Central Bank of Kenya (CBK) held the benchmark lending rate at 13% during its 3rd April meeting. This decision aims to solidify recent progress in curbing inflation, which dipped to a two-year low of 5.7% in March. The Monetary Policy Committee (MPC) expressed confidence in its past measures that addressed exchange rate pressures and inflationary expectations. The committee anticipates inflation to slow down in the near term, supported by lower food and fuel prices alongside a strengthening Shilling. Additionally, the MPC stated that the CBK will remain vigilant, monitoring economic developments and adjusting the rate if necessary.

Kenya secured a significant $500 million investment from the Abu Dhabi Developmental Holding Company (ADQ), a United Arab Emirates (UAE) sovereign wealth fund, aiming to fund key projects in the region. This strategic partnership goes beyond just funding, establishing a framework for future collaboration and enabling the exploration of potential investments and joint ventures across Kenya’s diverse economy. This aligns with country’s position as a pioneer in African-UAE trade relations, having initiated bilateral trade negotiations in 2022. The deal strengthens the already robust economic ties between the two nations. Earlier in 2024, Kenya and the UAE signed a Comprehensive Economic Partnership Agreement (CEPA) to facilitate trade in various sectors, including food production, mining, technology and logistics.

The Kenya Power and Lightning Company Limited (KPLC) announced a reduction in electricity prices in April 2024, bringing relief to Kenyan consumers. This was primarily attributed to a stronger Kenyan Shilling and a significant decrease in fuel costs used for power generation. The fuel cost charge dropped from Kshs 4.64 in March to Kshs 3.26 in April, while the foreign exchange adjustment charge also saw a notable decline, from Kshs 3.68 to Kshs 1.96. These factors translate to real savings for households, with reductions ranging from 9.7% to 13.7% depending on their consumption band. The positive trend is expected to continue due to favorable economic conditions and a shift towards less expensive hydropower generation.

The International Finance Corporation (IFC) is investing $165 million into Airtel Africa, a leading telecom provider, to enhance network infrastructure in Kenya, Rwanda and the Democratic Republic of Congo. This investment will modernise Airtel’s networks through 4G equipment purchases, improve overall connectivity for users and refinance existing debt, marking a continued partnership between the IFC and Airtel Africa following a successful collaboration in 2022.

UK’s inflation rate decreased to 3.2% in March 2024, exceeding market expectations but remaining above the Bank of England’s 2% target. This marks the lowest rate since September 2021 and was primarily driven by a slowdown in the rate of food and hospitality price increases. However, transport costs rebounded slightly, highlighting continued inflationary pressures. While the core inflation rate, excluding food and energy, also fell to a 16-month low. The Bank of England may need to maintain its current interest rate policy to ensure inflation continues to decline.

The Caixin China General Manufacturing PMI rose to 51.4 in April 2024 from 51.1 in March, exceeding the estimates of 51. This marked the sixth consecutive month of expansion and the fastest pace since February 2023, driven by the strongest output growth since May 2023. Notably, new orders and foreign sales surged to their highest levels in over a year and three-and-a-half years respectively. However, despite increased purchasing activity and rising stockpiles, employment continued to decline. While input costs soared, selling prices dipped due to competition, leading to a slight weakening in sentiment among manufacturers.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign exchange reserves increased by 2.03% to settle at $7.23 billion (3.80 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

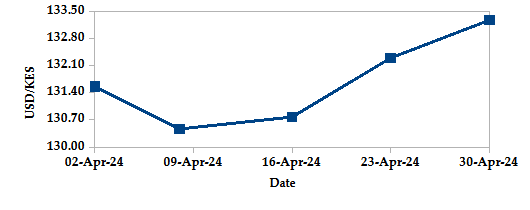

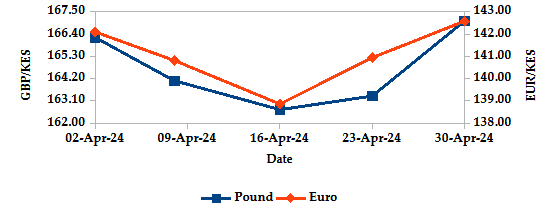

The Kenyan Shilling depreciated against the USD and the Sterling Pound by 1.12% and 0.30% but appreciated against the Euro by 0.06%, exchanging at Kshs 133.28, Kshs 167.05 and Kshs 142.58 respectively at the end of the month, from Kshs 131.80, Kshs 166.55 and Kshs 142.67 in the previous month. The observed depreciation against the Dollar is attributed to a high demand for the currency.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation decreased to 4.98% in April from 5.70% in March. This was primarily driven by reduced fuel, electricity and food prices.

INFLATION EVOLUTION

Liquidity

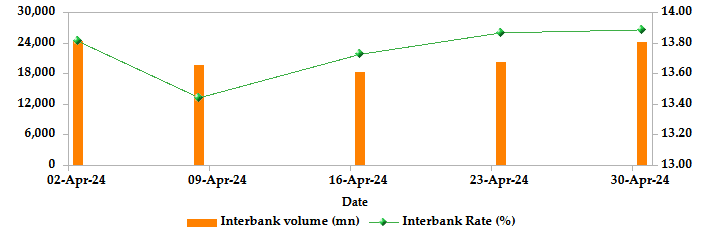

During the month, liquidity tightened as a result of tax remittances which more than offset government payments. The average inter-bank rate increased from 13.48% to 13.71%. The volume of inter-bank transactions decreased from Kshs 26.64 billion to Kshs 22.35 billion. Commercial banks excess reserves increased from Kshs 18.30 billion to Kshs 22.60 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

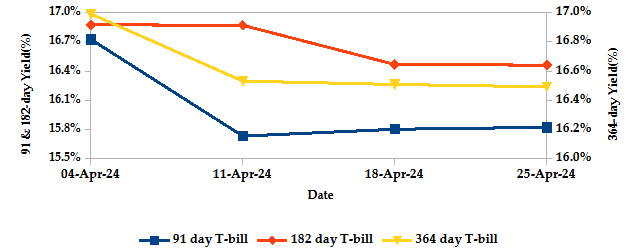

T-bills recorded an overall subscription rate of 129.58% during the month of April, compared to 109.13% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 231.87%, 77.95% and 140.28% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers decreased by 5.42%, 2.53% and 2.93% to 15.82%, 16.46% and 16.49% respectively.

T-BILLS

T-Bonds

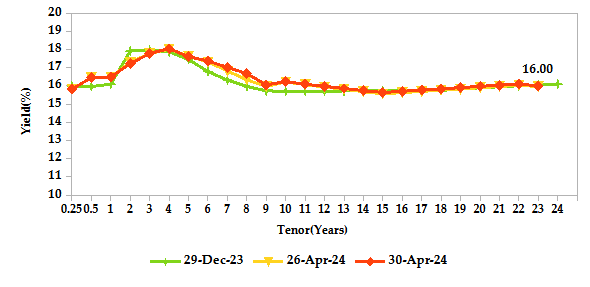

During the month, T-Bonds registered a total turnover of Kshs 93.45 billion from 2,674 bond deals. This represents a monthly decrease of 25.52% and 13.49% respectively. The yields on government securities in the secondary market decreased during the month of April.

In the primary bond market, CBK re-opened a 10-year bond FXD1/2024/10, targeting to raise Kshs 25.0 billion. The coupon rate was 16.00%. The issue received bids worth Kshs 14.98 billion, representing a subscription rate of 59.92%. Of these, Kshs 11.00 billion worth of bids were accepted at a weighted average rate of 16.23%.

In the international market, yields on Kenya’s Eurobonds increased by an average of 58 basis points.

YIELD CURVE

EQUITIES

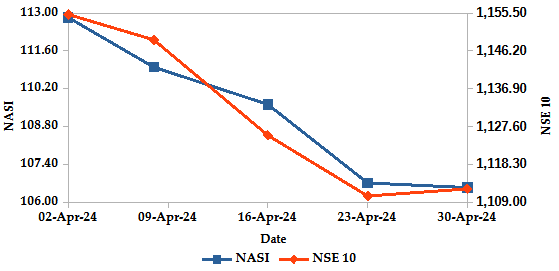

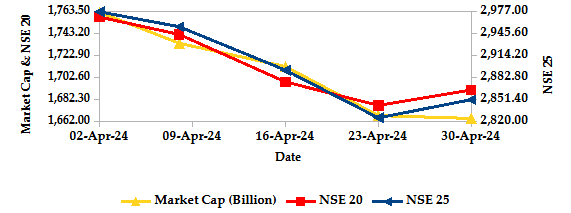

During the month, market capitalization lost 5.80% to settle at Kshs 1.66 trillion. Total shares traded decreased by 53.06% to 301.35 million shares and equity turnover also decreased by 34.66% to close at Kshs 7.33 billion. On a monthly basis, NASI, NSE 20, NSE 25 and NSE 10 settled 5.79%, 3.51%, 4.18% and 3.73% lower. The performance was as a result of losses recorded by large cap stocks such as Co-operative, Standard Chartered, Safaricom and Equity of 17.00%, 15.30%, 10.14% and 9.76% respectively. This was however mitigated by gain recorded by EABL of 22.22%.

NASI and NSE 10

Market Capitalization, NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

The derivatives market, over the month, recorded a turnover of Kshs 9.55 million with 62 contracts, which was a decrease from Kshs 29.16 million with 86 contracts recorded in the previous month.

I-REIT market, had no transaction over the month, from Kshs 550 million with 1 deal recorded in the previous month..

The ETF market, over the month, recorded a turnover of Kshs 0.29 million with 1 contract which was a decrease from Kshs 0.55 million with 2 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

Global Markets

Weekly Change

Monthly Change

S&P 500

-4.16%

6.17%

STOXX Europe 600

-1.52%

5.51%

Shanghai Composite (SSEC)

2.09%

4.81%

MSCI Emerging Market Index

0.26%

2.08%

MSCI World

-3.85%

4.29%

Regional Markets

Weekly Change

Monthly Change

FTSE ASEA Pan African Index

257.38%

244.10%

JSE All Share

2.31%

0.85%

NSE All Share (NGSE)

-6.06%

29.26%

DSEI (Tanzania)

-0.30%

1.18%

ALSIUG (Uganda)

-3.05%

19.28%

Global markets were volatile during the month. In the US, the S&P 500 lost 4.16% and the Dow Jones index lost 5.00%, as investors grappled with rising treasury yields and diminishing hopes for near-term interest rate cuts by the Federal Reserve. In Europe, the STOXX Europe 600 edged 1.52% lower, while the UK’s FTSE 100 index closed higher by 2.41%, as investors digested unexpected low earnings from carmakers, while positive economic data and a potential bank merger offered signs of a potential economic recovery. The Shanghai Composite (SSEC) index gained 2.09%, buoyed by a rally in Chinese stocks. This was primarily driven by recovering earnings, attractive valuations and signs of new government policies aimed at alleviating the prolonged property crisis in China.

On a regional front, markets were volatile during the month. The FTSE ASEA Pan African index, representing the overall African markets gained 257.38% from March. South Africa’s JSE All Share Index gained 2.31% while Nigeria’s All share index lost 6.06%. Furthermore, Tanzania’s DSEI and Uganda’s All Share index decreased by 0.30% and 3.05% respectively.

On the global commodities markets, oil futures indices were volatile ,fueled by Saudi Arabia’s aggressive price hike for crude oil which signaled confidence in OPEC+ implementing planned production cuts, potentially leading to a future decrease in supply and pushing prices upwards. Additionally, renewed regional conflict and the closure of a key Gaza crossing raised concerns about potential disruptions to oil supply routes, further contributing to price fluctuations and uncertainty in the market. Crude Oil WTI futures settled 1.49% lower while ICE Brent Crude Oil settled 0.99% higher to close at $81.93 and $87.86 respectively.

Get future reports

Please provide your details below to get future reports: