MONTH’S HIGHLIGHTS

- The Energy & Petroleum Regulatory Authority (EPRA) retained the prices of petroleum products that will prevail for the period between February and March 2022. Additionally, EPRA released energy and petroleum statistics for 2021. The report noted a general increase in demand for petroleum products in the second half of 2021 is attributed to eased COVID-19 restrictions.

- During the month, Russia invaded Ukraine, a move that has adversely impacted Equity markets and oil prices. Moody’s Analytics noted significant escalation of the Ukraine-Russia conflict rattled equity markets and led to an increase in global oil prices to more than $100 per barrel for the first time since 2014.

- The Capital Market Authority (CMA) provided approval for the Central Depository and Settlement Corporation (CDSC) to exit the regulatory sandbox and offer Securities Lending and Borrowing (SLB) in a live market environment.

- Yields on Kenyan Eurobonds spiked towards the end of the month as investors fled the safe haven of Western bonds as a result of the Russia – Ukraine crisis. The yields recorded a 0.86% increase in line with the general African market bond performance.

- The National Treasury reopened three bonds, FXD1/2021/05, FXD1/2020/15 and FXD1/2021/25 seeking to raise Kshs. 50 billion for budgetary support. The infrastructure bond IFB1/2022/19 that was sold during the month was oversubscribed with bids of Shs. 132.26 Billion against the targeted Sh. 75 Billion.

- Mobile money transactions in Kenya surged 32% to KSh 6.8 trillion in 2021 compared to KSh 5.2 trillion in 2020, attributable to an increase in the use of cashless transactions by firms and households. This comes at a time when the country is steadily recovering from the pandemic-induced disruptions.

- Fertiliser prices in Kenya are likely to drastically increase on fears that Russia’s invasion of Ukraine will curtail global supplies. Russia was the world’s largest exporter of nitrogen products or planting fertiliser in 2021. Those higher costs could therefore be passed onto customers through higher food prices.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 1.89% to stand at USD 8.13 billion(4.97 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

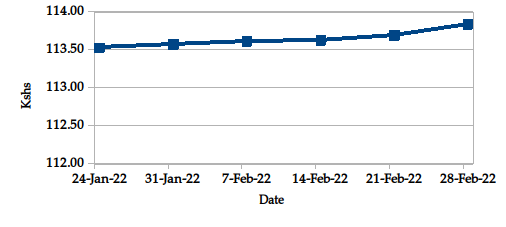

The Kenyan Shilling depreciated against the USD by 0.23%, exchanging at Kshs 113.84 at the end of the month up from Kshs 113.57 in the previous month. The depreciation is due to an increase in costs of imported products including oil, machinery and other capital goods. Bottlenecks in global supply chains have pushed up container and shipping costs. Recent developments with Russia’s military action in Ukraine have increased geopolitical tensions which could see a hike in fuel pump prices in Kenya.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

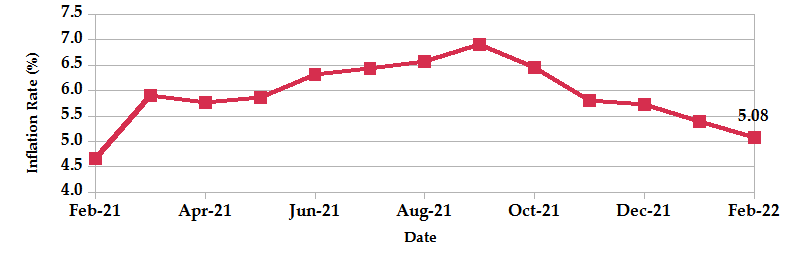

The overall year-on-year inflation decreased to 5.08% in the month of February down from a revised figure of 5.39% in January. The decrease is attributable to a slowdown in prices of food & non-alcoholic beverages and housing & utilities due to a 15% cut on electricity tariff effective January.

INFLATION EVOLUTION

Liquidity

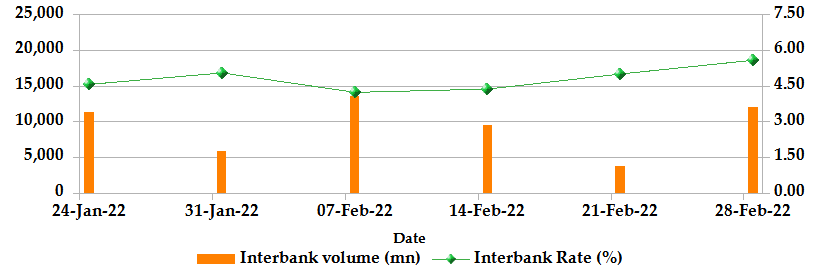

During the month, liquidity tightened as a result of the government and corporate bond issue during the month. The inter-bank rate increased to 4.72% up from 4.49%. The volume of inter-bank transactions increased to Kshs 12.02 billion from Kshs 5.04 billion. Commercial banks’ excess reserves increased to Kshs 17.00 billion from Kshs 8.00 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

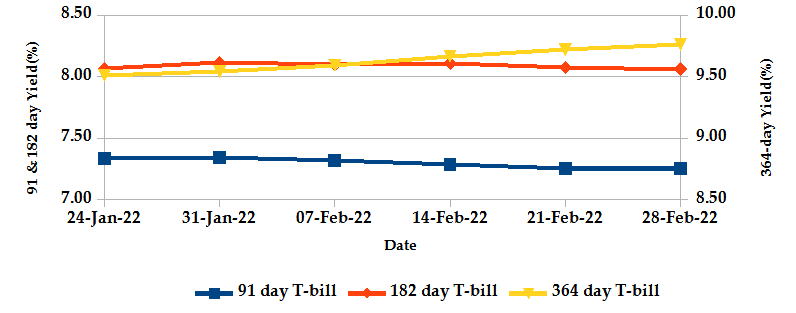

T-Bills

The T-bills recorded an overall subscription rate of 93.63% at the end of the month of February, compared to 120.09% recorded in the previous month. The under-subscription is partly attributable to tightened liquidity in the money markets. The performance of the 91-day, 182-day and 364-day papers stands at 61.1%, 72.1% and 128.2% respectively. On a monthly basis, the yields on the 91-day and 182-day papers decreased by 1.21% and 0.62% respectively to 7.25% and 8.06%. On the other hand, the yield on the 364-day paper increased by 2.31% to 9.76%.

T-BILLS

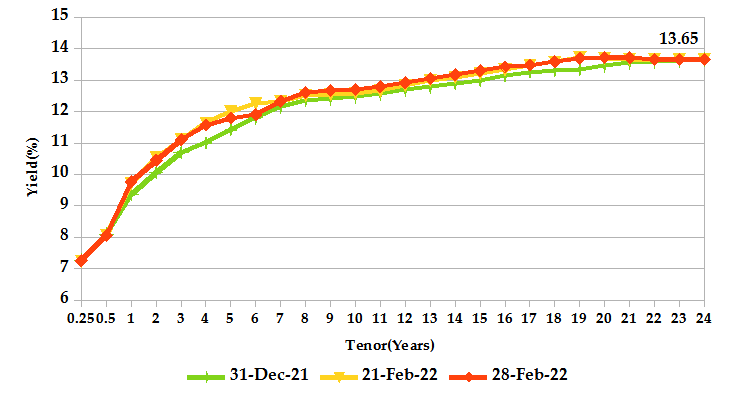

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 10.96 billion from 843 bond deals. This represents a weekly increase of 3.87 billion in turnover and 560 in deals respectively. The yields on government securities in the secondary market remained relatively stable during the month of February.

In the international market, yields on Kenya’s Eurobonds rose by an average of 86.6 basis points.

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 105 contracts having a turnover of Kshs 14.7 million which was an increase from 85 contracts having a turnover of Kshs 9.8 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.7 million with 193 deals which was an increase from Kshs 1.5 million with 218 deals recorded over the last month.

- The ETF market recorded no activity over the month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 1.60% | -3.14% |

| STOXX Europe 600 | -0.44% | -3.36% |

| Shanghai Composite (SSEC) | 0.15% | 3.00% |

| MSCI Emerging Market Index | -2.93% | -3.06% |

| MSCI World Index | 0.07% | -2.65% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -2.79% | 0.82% |

| JSE All Share | 1.09% | 2.66% |

| NSE All Share (NGSE) | 0.34% | 1.65% |

| DSEI (Tanzania) | -0.24% | 1.59% |

| ALSIUG (Uganda) | 1.35% | 1.63% |

- During the month, major global markets declined as rising tensions between Ukraine and Russia continued to unsettle global investors causing a significant increase in economic uncertainty which poses a risk to growth and pandemic recovery. In the USA, the S&P 500 and Dow Jones indices declined by 3.14% and 3.53% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 declined by 3.36% and 0.08% respectively.

- On a regional front, most markets had marginal gains however the impact of the recent Ukraine crisis and its impact on oil prices are likely to affect investor returns. The FTSE ASEA Pan African index, representing the overall African markets, gained by 0.82% from the month of January. South Africa’s JSE All Share went up by 2.66%, Nigeria’s All Share Index rose by 1.65%, Tanzania’s DSEI increased by 1.59% and Uganda’s All Share Index increased by 1.63%.

- On the global commodities markets, the oil futures indices continued to experience trade disruption and shipping issues from Western sanctions against Russia. This drove supply worries while U.S. crude supplies fell to a multi-year low. The OPEC, which includes Russia, decided to maintain an increase in output by 400,000 barrels per day seemingly ignoring surging prices, the invasion, and calls from some stakeholders to increase supply. The Crude Oil WTI futures surged by 8.59% and the ICE Brent Crude Oil increased in value by 10.72% from the previous month of January.

YIELD CURVE

EQUITIES

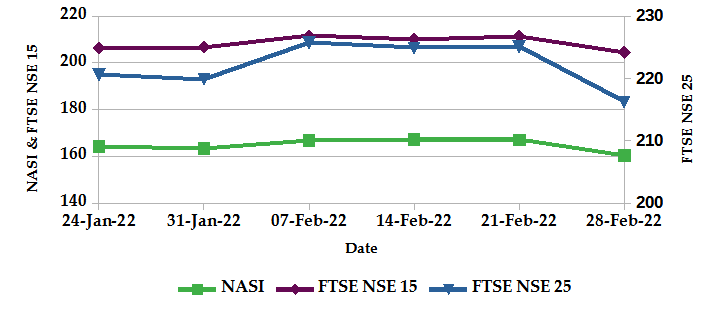

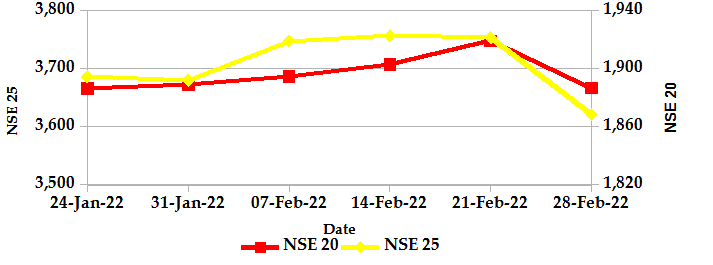

During the month of February, the market capitalization declined by 1.87% to 2.50 trillion. However, total shares traded increased by 16.0% to 72 million shares while equity turnover declined by 11.0% to Kshs 2.3 billion. NASI, NSE 20 and NSE 25 declined by 1.9%, 0.1% and 1.6% in that order on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 declined by 4.1%, 1.7% and 3.5% respectively. The decline in NASI is a result of a decline of large-cap stocks such as EABL, Kengen Company and Safaricom.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

Get future reports

Please provide your details below to get future reports: