MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) met on November 29, 2021, against the backdrop of the COVID-19 pandemic, the continued rollout of vaccination programs and the emerging developments regarding the new COVID-19 variant. Inflation is expected to remain anchored within the target range in the near term with muted demand pressures. Leading economic indicators have shown continued robust performance. The MPC concluded that the current accommodative monetary policy stance remains appropriate, and therefore decided to retain the Central Bank Rate (CBR) at 7%.

- The global economy continues to strengthen, largely supported by the ongoing deployment of vaccines, improved business investment and consumer spending, and accommodative policy measures. However, the pace of recovery remains uneven across countries, in part due to an uneven distribution of vaccines, varied supply chain constraints, and disparate policy support measures.

- Inflation in the advanced economies and emerging markets has risen sharply, driven in part by rising global oil prices and raising concerns about the policy response to the Covid-19 pandemic.

- The recently released GDP data indicates that the Kenyan economy rebounded strongly in the first half of 2021, mainly reflecting the recovery in economic activity following the easing of COVID-19 restrictions.

- The three surveys conducted for the MPC meeting—Private Sector Market Perceptions Survey, CEOs Survey, and the Survey of Hotels—revealed the highest level of optimism about economic growth prospects since March 2021. Respondents attributed this optimism to sustained recovery across different sectors, the lifting of the curfew, reduced COVID-19 infection numbers and increased vaccinations, continued government infrastructure spending, and the global economic recovery which is expected to boost export demand.

- The CBK foreign exchange reserves, which currently stand at USD 8,768 million (5.36 months of import cover), continue to provide adequate cover and a buffer against short-term shocks in the foreign exchange market.

- The banking sector remains stable and resilient, with strong liquidity and capital adequacy ratios. The ratio of gross non-performing loans (NPLs) to gross loans stood at 13.6% in October compared to 13.9% in August.

- Growth in private sector credit increased to 7.8% in October 2021, from 7.0% in August. Strong credit growth was observed in the following sectors: manufacturing (10.9%), transport and communication (9.6%), business services (8.2%) and consumer durables (16.5%).

- Fuel prices will remain the same in this month’s review even with rising crude oil costs, subsidized by the Petroleum Development Levy. Last month, The National Assembly Committee on Finance recommended a reduction in taxes and levies through tax law amendments to cushion Kenyans from the spike in fuel prices in recent months. Fuel consumers have been contributing to the levy kitty provided for fuel price stabilization in the country, with the highest contribution per litre of fuel being Kh5.40 under the Petroleum Development Levy Fund Order (2020).

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 4.77% to stand at USD 8.74 billion (5.34 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

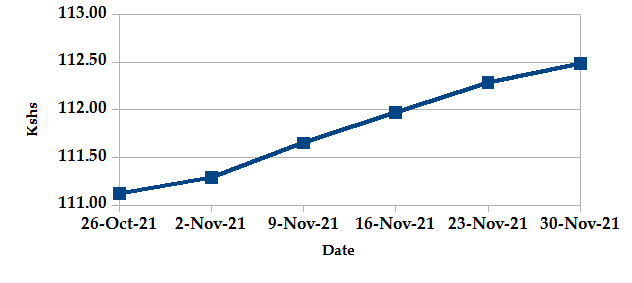

The Kenyan Shilling depreciated against the USD by 1.15%, exchanging at Kshs 112.49 at the end of the month up from Kshs 111.21 in the previous month. The depreciation is due to increased dollar demand and rising global inflation rising from supply chain constraints which result in heightened demand relative to supply.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

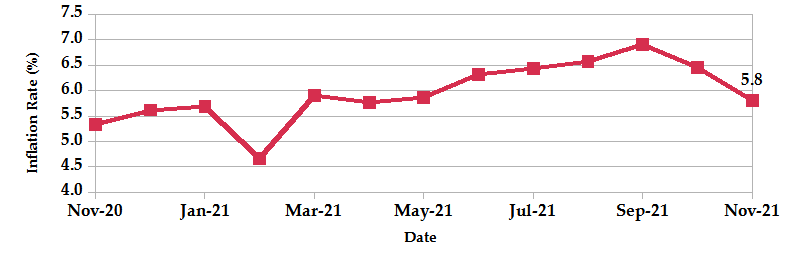

The overall year-on-year inflation decreased to 5.80% in the month of November down from a revised figure of 6.45% in October. The inflation is attributable to an increase in prices of food and non-alcoholic beverages by 0.91% due to an increase in prices of sugar, cooking oil and irish potatoes. The transport index decreased by 0.16%. The Housing, Water, Electricity, Gas and Other Fuels’ Index, increased by 0.49% between October 2021 and November 2021. This was mainly attributed to the increase in prices of cooking gas (LPG) and house rent for single rooms that went up by 3.88% and 0.53%, respectively

INFLATION EVOLUTION

Liquidity

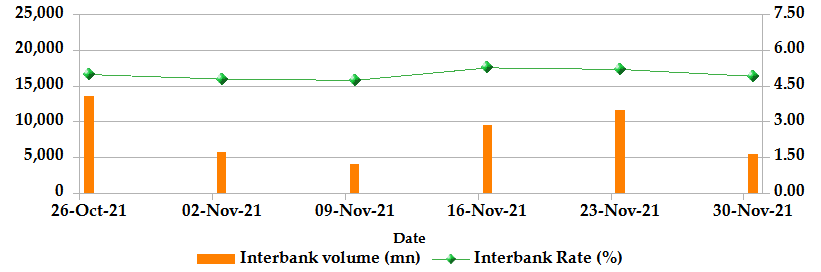

During the month, liquidity tightened as a result of tax remittances which partly offset government payments. The inter-bank rate marginally decreased to 4.90% down from 4.98%. The volume of inter-bank transactions decreased from Kshs 13.51 billion to Kshs 5.35 billion. Commercial banks’ excess reserves decreased to Kshs 13.90 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

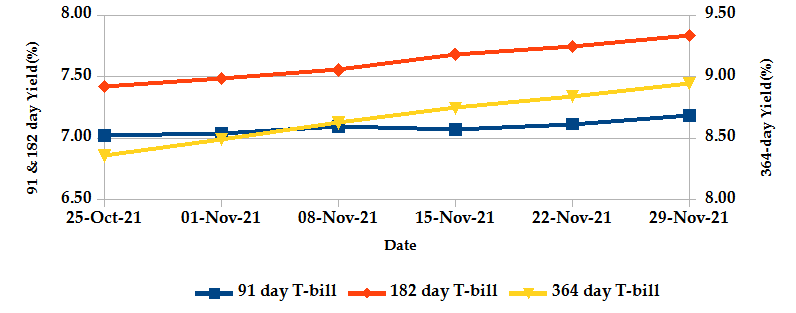

The T-bills recorded an overall subscription rate of 79.7% at the end of the month of November, compared to 56.68% recorded in the previous month. The under-subscription is partly attributable to investors’ preference for T-Bonds due to higher yields on the longer papers. The performance of the 91-day, 182-day and 364-day papers stand at 142.4%, 59.0% and 75.2% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 2.2%, 4.1% and 7.2% respectively to 7.10%, 7.66% and 8.73%.

T-BILLS

T-Bonds

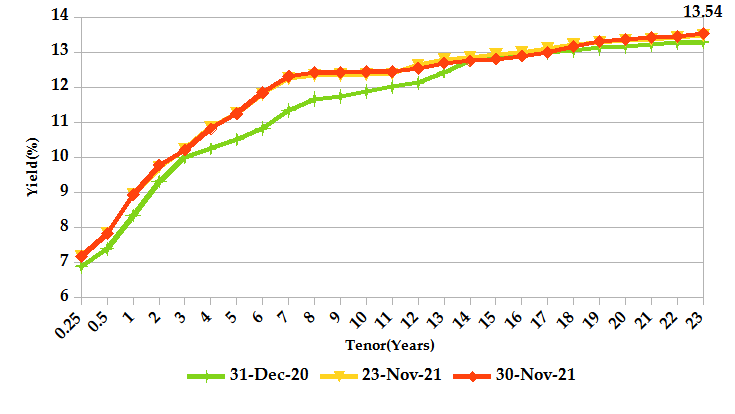

At the end of the month, the T-Bonds registered a total turnover of Kshs 18.82 billion from 529 bond deals. This represents a monthly decrease of 18.2% and 18.1% respectively. The yields on government securities in the secondary market remained relatively stable during the month of November.

In the international market, yields on Kenya’s Eurobonds increased by an average of 14.4 basis points.

YIELD CURVE

EQUITIES

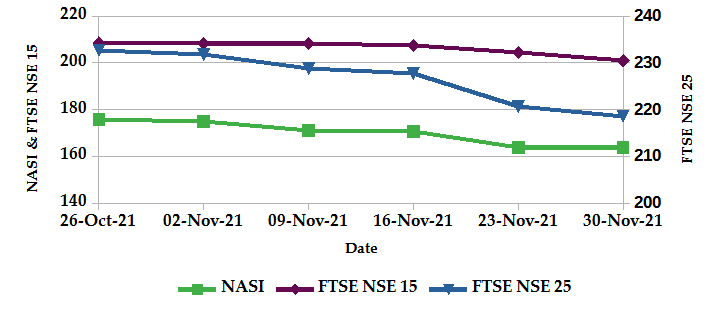

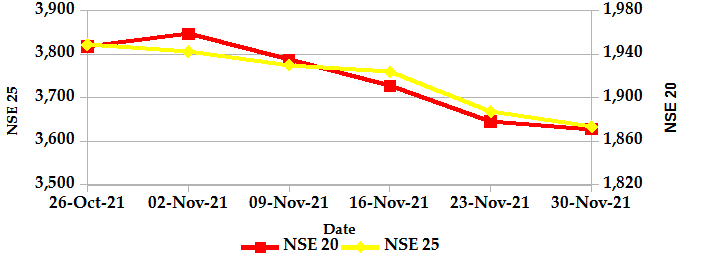

During the month of November, the market capitalization declined by 8.07% to Kshs 2.52 trillion. However, total shares traded and equity turnover increased from 50.94 million shares and Kshs 1.95 billion respectively to 169.40 million shares and Kshs 5.96 billion. NASI, NSE 20 and NSE 25 declined by 7.9%, 4.6% and 5.7% respectively on a monthly basis. On a weekly basis, the NASI gained by 0.07% while NSE 20 and NSE 25 declined by 0.38% and 0.94% respectively. The decline in NASI is a result of the depreciation of large-cap stocks such as Safaricom, East Africa Breweries Limited (EABL) and Kengen.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 176 contracts having a turnover of Kshs 19.0 million which was an increase from 201 contracts having a turnover of Kshs 11.0 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.6 million with 175 deals which was a decrease from Kshs 2.8 million with 198 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 11.0 million with 4 deals which was an increase from the last month which recorded no activity.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -2.64% | -0.83% |

| STOXX Europe 600 | -3.40% | -2.64% |

| Shanghai Composite (SSEC) | -0.70% | 0.47% |

| MSCI Emerging Market Index | -3.42% | -4.14% |

| MSCI World Index | -2.97% | -2.30% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -1.20% | -4.67% |

| JSE All Share | -0.78% | 5.35% |

| NSE All Share (NGSE) | -0.02% | 2.88% |

| DSEI (Tanzania) | -0.98% | -2.53% |

| ALSIUG (Uganda) | -2.37% | -2.88% |

- During the month, major global markets declined as investors’ uncertainty over the emerging Covid-19 variant Omicron took hold. In the USA, the S&P 500 and Dow Jones indices declined by 0.83% and 3.73% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 declined by 2.64% and 2.46% respectively.

- On a regional front, most markets had mixed performance. The FTSE ASEA Pan African index, representing the overall African markets, plunged by 4.67% from the month of October over investor concerns over the spread of the Omicron variant of COVID-19. South Africa’s JSE All Share gained by 5.35% over the month attributable to risk appetite returning somewhat to markets, with investors betting that the Omicron Covid-19 variant would not derail the economic recovery.

- On the global commodities markets, oil prices fell sharply as Russia was said to propose OPEC+ (a grouping of the Organization of the Petroleum Exporting Countries) sticks with a planned 400,000 barrel-a-day production hike for January. The group has been incrementally increasing oil production since August as it continues to unwind the deep production cuts it agreed to when oil prices crashed in the opening months of the pandemic. The Crude Oil WTI futures plunged by 20.81% from the previous month of October and the ICE Brent Crude Oil declined in value by 16.37%.

Get future reports

Please provide your details below to get future reports: