Foreign Exchange reserves

The CBK’s usable foreign exchange reserves continued to strengthen from the precedingweeks to remain adequate at USD 8.532 billion (5.14 months of import cover).This meetsCBK’s statutory requirement to endeavor to maintain at least 4.0 months of import cover,and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

During the week, the Kenyan Shilling remained relatively stable against major global andregional currencies, trading against the USD at Kshs 106.81 up from Kshs 106.01 in theprevious week.

Liquidity

The money market remained relatively liquid underpinned by government payments whichmore than offset tax receipts. The weekly mean of the daily weighted average inter-bank ratesetled at 4.17% compared to 4.13% in the previous week. The value transacted improved fromKshs 7.80 billion to Kshs 12.93 billion. Commercial banks’ excess reserves decreased to Kshs36.50 billion down from Kshs 39.90 billion.

Fixed Income

T-Bills

T-bills were oversubscribed at a rate of 100.37%. All the papers recorded increased subscriptionfrom the previous week. The 91-day and 364-day papers were oversubscribed at 191.77% and119.32% respectively, while the 182-day paper was undersubscribed at 44.85%. The yields onthe 91-day and 364-day papers increased by 10 basis points to stand at 7.27% and 9.17%respectively. The yield on the 182-day paper grew by a higher margin of 50 basis points tostand at 8.19%.

T-Bonds

The bonds market registered reduced activity from the previous week with the bonds turnoverdeclining from Kshs 11.81 billion to Kshs 10.73 billion. The total bond deals decreased from 556to 464.In the international market, yields on Kenya’s Eurobonds increased by an average of 82.5 basispoints. The yields on the 10-year Eurobonds for Angola and Ghana also increased towards theend of the week.

Equities

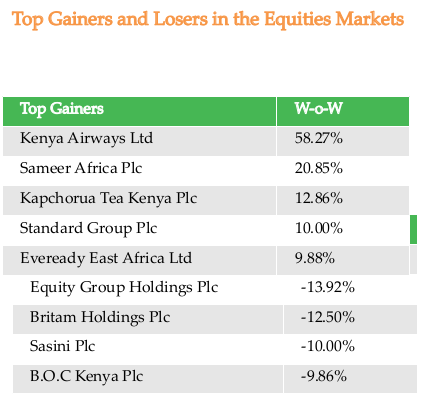

The equities market recorded reduced activity with the market capitalization declining by 3.94% to settle at Kshs 2,063.30 billion. However, the equities turnover and total shares traded grew by 1.53% and 22.97%, respectively to Kshs 4.93 billion and 145 million shares.NASI, NSE 20 and NSE 25 share indices plunged by 3.93%, 2.92% and 5.16% respectively. The performance of NASI was mainly driven by losses recorded by large cap stocks such as NCBA, Equity, Britam and KCB which depreciated by 14.20%, 13.92%, 12.50% and 8.71%, respectively.The Banking sector accounted for 38.65% of the week’s traded value, Manufacturing & Allied sector represented 25.87% and Safaricom was the week’ s main feature representing 34.21% after its shares worth Kshs 1.68 billion were transacted.

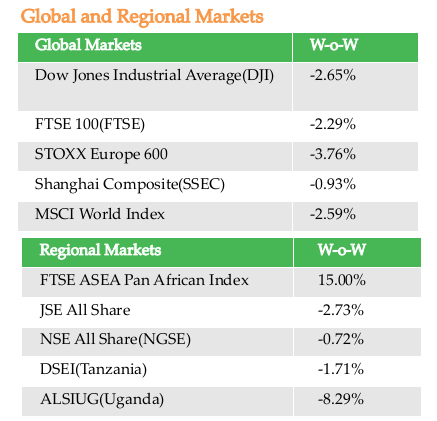

During the week, the global markets were on a downward trend partly due to rising USA – China tensions. The MSCI World Index shed 53 points to 41. In the USA, the Dow Jones Industrial Average and S&P 500 depreciated by 2.26% and 2.65% respectively to close the week at 2863.7 and 23685.42. In the European markets, STOXX Europe 600 fell by 3.76% while UK’s FTSE 100 shed 136 points to stand at 5799.77. Shanghai Composite lost 27 points to close at 2868.46. On the regional front, the Pan African share index, FTSE ASEA edged up by 15% to stand at 1333.80 up from 1159.81 in the previous week. South Africa’s JSE All Share lost value after decreasing to 49628.72 down from 51003.58. Within the East Africa Community, Tanzania’s DSEI dropped 32 points to close at 1822.84. Uganda’s ALSIUG dipped by 8.29% to settle at 1345.30. On global commodities market, oil prices went up on signs that demand from China is picking up. The Crude Oil WTI and ICE Brent Crude futures gained by 18.96% and 4.94% respectively to close at USD 29.43 and 32.50. The German economy contracted by 2.2% in Q1 2020, its steepest three-month slump since the 2009 financial crisis due to the effects of COVID-19 pandemic.

On the continental front, the FTSE ASEA Pan African index appreciated by 1.11% to 1159.81. The South African, JSE All Share and Nigerian, NSE All Share went up by 1.32% and 4.45% respectively. Within the East African Community, the DSEI(Tanzania) and ALSIUG(Uganda) outperformed Kenya’s NASI after the two indices surged by 4.00% and 7.69%,respectively. The National Bank of Rwanda slashed its policy rate to 4.5% down from 5.5%. The decision is aimed at supporting commercial banks to continue financing the economy. The Rwandese government projects its economy growth to fall to 3.5%.

Alternative Investments

The Derivative Market closed the week with a total of 33 contracts worth Kshs 1.1 million. KCB contract expiring in 17th September 2020 had 22 contracts traded valued at Kshs 827, 000. The I-REIT market registered a turnover of Kshs 915,420 from 56 unit deals.

Week’s Highlights

- The Central Bank of Kenya (CBK) sought to switch T-Bill investors to bonds with a view to provide relief to exchequer upcoming redemption’s on local debt. The desired switch has been pinned on its June infrastructure bond issue whose eligibility has been specified to holders of a one-year T-bill maturing on 1st June. The bond aims to raise Kshs 25.6 billion and has a value date equivalent to the maturity of the one-year paper tagged 2236/364 which raised Kshs 23.5 billion in proceeds. The government is presently facing debt-refinancing pressures as the COVID-19 has impacted revenue generation.

- Scangroup is set to receive an additional Kshs 480 million from the disposal of its 60% stake in its subsidiary firm,Kantar Africa. The extra compensation is in the form of profit-sharing in the unit for the period leading up to the conclusion of the transaction and payouts tied to the unit’s indebtedness. The firm expects minimum proceeds of Sh 5.2 billion in the deal, with the potential extra payouts taking the total consideration to Sh 5.7 billion. Scan group says net proceeds from the transaction will be Sh 5 billion and that it will use at least 40% of the amount (Sh 2 billion) to pay a special dividend.

- Stanbic Bank Kenya posted its financial results for Q1, 2020. The lender’s net profits declined to Kshs 1.5 billion down from Kshs 2.3 billion in Q1, 2019. The decline is attributable to decreased interest income brought about by the restructuring of loans amid the ongoing global pandemic. The lender’s portfolio of non-performing loans grew from Kshs 13.5 billion to Kshs 16.3 billion. However, the bank’s balance sheet expanded from Kshs 284.9 million to Kshs 309.7 million.

- CBK data has showed that the amount of cash in circulation is on a downward trend from the beginning of the year. The cash in circulation decreased by 10% to Kshs 241.96 billion in February, 2020 when compared to the same month last year. The amount has further declined by 7% from Kshs 265.87 billion recorded at the end of last year.In January, 2020, the cash in circulation stood at Sh 242.06 billion down from Sh 262.38 billion at the same time last year. This phenomenon is an indication that the CBK projects lower economic activity.

- The International Monetary Fund (IMF) excluded Kenya from the list of countries granted loan interest payment waivers because Kenya’s per capita income stands at USD 1,710. The IMF was granting reprieve to countries with per capita income below USD 1,215. IMF loan to Kenya stood at Kshs 50.9 billion in June 2019, representing 5.27%of the Kshs 947.5 billion Kenya owes multilateral lenders.

- Global rating agency Moody’s changed the outlook of local hostel developer Acorn Group’s Kshs 5 billion greenbond to negative from stable. Moody’s stated the negative outlook reflects the challenges posed to the construction and marketing of its assets because of COVID-19 lockdown measures and potential longer term impact on demand.The bond sale in October 2019 achieved an 85% subscription of the targeted Kshs 5 billion.