Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,621 million (4.39 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover, and the EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at Ksh 119.57, Ksh 121.58 and Ksh 144.15 respectively. The observed overall depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 5.68% | 0.22% |

| Euro | -5.08% | -1.07% |

| Sterling Pound | -5.37% | -0.87% |

Liquidity

Liquidity in the money markets eased, partly reflecting tax remittances which offset government payments. Open market operations remained active. Diaspora remittances for the month of July stood at $319.4M representing a -5.14% and -2.04% change year on year and month on month respectively.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 5.60% | 5.53% |

| Interbank volume (billion) | 30.3 | 21.4 |

| Commercial banks’ excess reserves (billion) | 27.2 | 30.3 |

Fixed Income

T-Bills

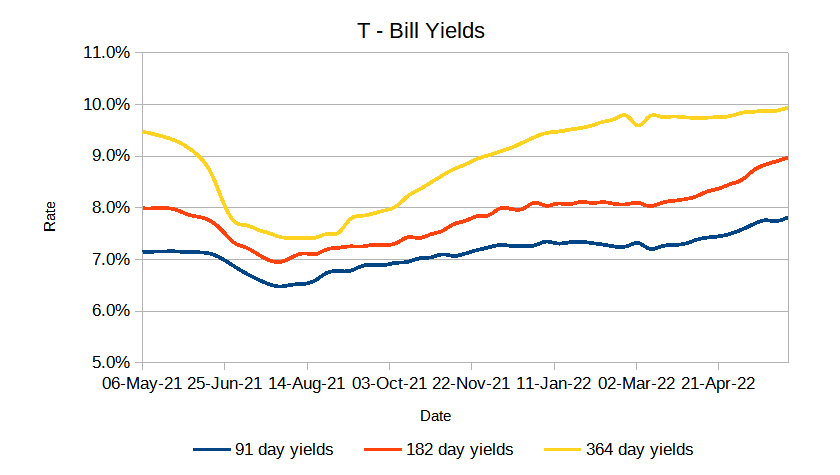

T-Bills were over-subscribed during the week with an increase in the overall subscription rate from 72.36% recorded in the previous week to 197.15%. The 91-day T-Bill got the highest subscription rate at 294.3% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 68.0% and 16.80% respectively. The acceptance rate increased by 0.25% to close the week at 99.94%.

T-Bonds

The bonds market had a higher demand for the week’s bond offers. Bonds turnover increased by 31.99% from 1.99B in the previous week to 2.62B. Total bond deals decreased by 70.56% from 87 in the previous week to 58.

Eurobonds

In the international market, the yields on the 10-year Eurobonds for Angola and Ghana increased. Yields on Kenya’s Eurobonds generally increased by 0.91% compared to the previous week, -1.537% and 6.535% month to date and year to date respectively. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 10.30% | -0.05% | 2.51% |

| 2018 10-Year Issue | 6.96% | -1.88% | 0.53% |

| 2018 30-Year Issue | 3.77% | -1.55% | 0.37% |

| 2019 7-Year Issue | 8.50% | -1.97% | 1.09% |

| 2019 12-Year Issue | 5.86% | -1.34% | 0.41% |

| 2021 12-Year Issue | 4.19% | -2.06% | 0.54% |

Equities

NASI, NSE 20 and NSE 25 decreased by 0.38%, 1.13% and 1.02% compared to last week bringing the year to date performance to -12.44%, -7.06% and -9.95% respectively. The market capitalization decreased by 0.38% from the previous week to close at 2.280 trillion recording a year to date decline of 12.38%. The performance was driven by gains recorded by large-cap stocks. Top gains were recorded in ABSA Bank, KCB Group and Safaricom which increased by 2.92%, 0.46% and 0.32% respectively.

The Banking sector had shares worth Ksh 211M transacted which accounted for 19.59% of the week’s traded value, Manufacturing & Allied sector had shares worth Ksh 94.5M transacted which represented 8.80% and Safaricom, with shares worth Kshs 723M transacted represented 67.23% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Liberty Holdings | 1.98% | 20.00% |

| Sameer Africa | 41.75% | 13.80% |

| Longhorn publishers | 0.25% | 9.83% |

| Sasini plc | 18.98% | 9.74% |

| EA cables | 1.63% | 8.33% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| Olympia | 10.53% | -12.13% |

| Transcentury | -0.83% | -8.46% |

| Scangroup plc | -9.76% | -5.37% |

| Equity Group | -9.00% | -4.95% |

| Nation Media | -3.54% | -4.75% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.39 | 0.13 | -99.55% |

| Derivatives Contracts | 9 | 5 | -86.84% |

| I-REIT Turnover | 0.56 | 0.016 | -98.80% |

| I-REIT Deals | 11 | 8 | -95.77% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -11.84% | -1.21% |

| Dow Jones Industrial Average (DJI) | -7.87% | -0.16% |

| FTSE 100 (FTSE) | 0.60% | 0.66% |

| STOXX Europe 600 | -10.74% | -0.80% |

| Shanghai Composite (SSEC) | -10.30% | -0.57% |

| MSCI Emerging Markets | -18.15% | -0.71% |

| MSCI World Index | -12.80% | -0.29% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -21.39% | -1.53% |

| JSE All Share | -6.04% | 1.60% |

| NSE All Share (NGSE) | 14.75% | -0.59% |

| DSEI (Tanzania) | 1.49% | 0.07% |

| ALSIUG (Uganda) | -5.65% | -0.86% |

US stocks closed the week lower as investors paused their bullish bets on stocks as they waited for more direction from the Federal Reserve. Growth sectors such as Technology were hurt by a fresh climb in Treasury yields with the benchmark 10-year note nearly hitting 3% after Germany reported record-high increases in monthly producer prices.

European stocks closed the week lower as investors fretted about soaring inflation, tightening monetary policy and slowing growth. With recession fears starting to rise in Europe, natural gas prices were on the rise adding to inflationary pressures just as Eurozone consumer prices were confirmed at an annual 8.9 percent in July which is way above the European Central Bank’s 2 percent target. This suggests that the regions central bank would have to add another half-point rate hike in September, to July’s increase, which will aggravate the risk of recession.

Asia Pacific stocks closed the week lower as hawkish comments from the Federal Reserve suggesting that the bank intended to keep raising rates at a sharp clip weighed on risk appetite. Chinese stocks fell slightly with concerns over slowing economic growth in the country and potentially worsening ties with the United States Over Taiwan dented local markets.

On the global commodities markets, Crude Oil WTI closed the week lower by 1.23% and the ICE Brent Crude decreased by 1.23%. Gold futures prices decreased by 0.01% to settle at $1,762.9.

Week’s Highlights

- Kenya’s debt hit Ksh 8.6 trillion in June 2022, an 11.5% yearly rise in public debt from Ksh 7.7 trillion recorded in June 2021. Data from the National Treasury indicated that gross public debt was up by Ksh 822.5 billion being split in half between domestic and external loans. Domestic debt rose the fastest at 16% to reach Ksh 4.288 trillion from 3.697 trillion in 2021 while external debt was up by 7.3% to Ksh 4.29 trillion from 4 trillion in 2021.

- Kenyans will experience higher fuel prices over the next 3 years should the Kenya Pipeline Company (KPC) increase the transportation and storage tariffs. The Energy and Petroleum Authority (EPRA) said KPC had applied for a review of the tariffs for the period 2021/22 to 2024/25 and that KPC aimed to use revenue from the proposed tariffs to partly fund the enhancement of the firms pipeline between Mombasa and Nairobi.

- Digital lenders moved to court seeking to revoke the 20% exercise tax on loans advanced to online borrowers. According to the Digital Finance Services Association of Kenya, the lenders want the court to bar the taxman from collecting or demanding payment of exercise duty on fees charged on loans.

- Commercial banks raised their lending rates to 16% for individuals and businesses in the second quarter of the year, indicating the early impact of accelerated approvals of risk-based lending plans by the Central Bank of Kenya indicating that more than half of commercial banks had had their lending plans approved allowing them to factor in the credit worthiness of a borrower when determining the rate to charge on their loan while those banks still waiting for approval had seen most of them lending at a maximum of 13%.

- The African Continental Free Trade Area (AfCFTA) unveiled a digital trading platform dubbed the AfCFTA Hub aimed at interconnecting national, regional and private digital applications to boost the ability of African SMEs to expand that will see them entitled to a free AfCFTA number that will aid in the export of products across Africa through improved logistics, networking of retail outlets, integration of fintech and brand development support.

- Ghana’s Central Bank increased its benchmark interest rate to 22% bringing the annual inflation to 31.7%, the highest rise since 2002, in an aim to curb inflation and stabilize the nations tumbling exchange rate. The monetary policy committee also decided to hike the primary reserve requirement of banks to 15% from 12%. Namibia’s Central Bank hiked lending rates to 5.5% to safeguard its currency peg with South Africa’s Rand and tame inflation. Egypt’s Monetary policy Committee maintained its lending rate at 12.25% and the deposit rate at 11.25%

Get future reports

Please provide your details below to get future reports: