Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves stood at USD 7,103 million (3.98 months of import cover). This falls below CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at KES 122.79, KES 129.11 and KES 149.71 respectively. The observed depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 8.53% | 0.21% |

| Euro | 0.80% | 0.61% |

| Sterling Pound | -1.73% | 0.23% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate rising from 5.11% to 5.25%, as tax remittances more than offset government payments. Remittance inflows totaled USD 345.45 million in November 2022, a 3.85% increase from USD 332.63 million in October and a 7.93% increase from USD 320.07 million in November 2021. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 5.11% | 5.25% |

| Interbank volume (billion) | 24.64 | 19.35 |

| Commercial banks’ excess reserves (billion) | 13.00 | 14.50 |

Fixed Income

T-Bills

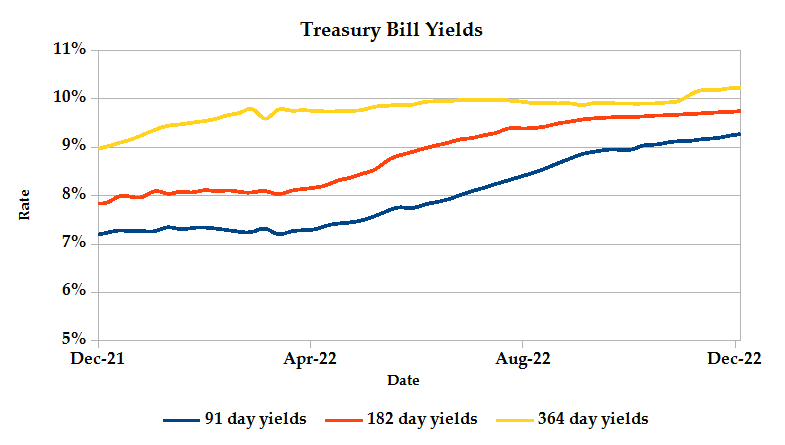

T-Bills remained under-subscribed during the week, with the overall subscription rate recorded as 97.05%, up from 82.42% in the previous week. The 91-day T-Bill received the highest subscription rate at 416.34% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 44.91% and 21.48% respectively. The acceptance rate declined by 17.65% to close the week at 81.85%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover declined by 15.86% from KES 14.41B in the previous week to KES 12.13B. Total bond deals decline by 29.13% from 793 in the previous week to 562.

In the primary bond market, CBK released auction results for the reopened bonds; FXD1/2008/20 and FXD1/2022/25 that sought KES 40.0 billion. The issues were under-subscribed, with the 20-year bond receiving bids worth KES 17.32 billion, while the 25-year bond received bids worth KES 13.24 billion, bringing the total performance to 76.43%. Of these, KES 24.33 billion worth of bids were accepted at an average rate of 13.83% and 14.44%, and a coupon rate of 13.75% and 14.19% for the 20-year and 25-year issues respectively.

Eurobonds

In the international market, yields on Kenya’s Eurobonds rose by an average 0.13% compared to the previous week and increased 4.24% year to date. The yields on the 10-year Eurobond for Ghana and Angola also increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 7.89% | 0.73% | 0.73% |

| 2018 10-Year Issue | 4.07% | 0.01% | 0.01% |

| 2018 30-Year Issue | 2.51% | -0.03% | -0.03% |

| 2019 7-Year Issue | 4.68% | 0.01% | 0.01% |

| 2019 12-Year Issue | 3.48% | 0.00% | 0.00% |

| 2021 12-Year Issue | 2.79% | 0.05% | 0.05% |

Equities

NASI and NSE 25 gained 0.03% and 0.17% respectively while NSE 20 dropped 0.22% compared to the previous week bringing the year to date performance to -24.32%, -17.81% and -13.99% respectively. Market capitalization picked up 0.03% from the previous week to close at KES 1.97 trillion recording a year to date decline of 24.30%. The performance was driven by gains recorded by large-cap stocks such as ABSA and EABL of 1.69% and 1.67% respectively. These were weighed down by losses recorded by KCB, Safaricom and Standard Chartered of 2.25%, 0.21% and 0.17%.

The Banking sector had shares worth KES 374M transacted which accounted for 27.45% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 289M transacted which represented 21.25% and Safaricom, with shares worth KES 429M transacted represented 31.50% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Total | 2.45% | 9.13% |

| Crown Paints | 24.59% | 8.57% |

| Williamson Tea | 23.08% | 6.67% |

| Unga | 15.73% | 6.67% |

| CIC Insurance | -10.60% | 6.59% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| Trans-Century | -34.17% | -11.24% |

| Home Afrika | -17.50% | -10.81% |

| NBV | -39.08% | -8.71% |

| EA Cables | -34.96% | -8.05% |

| HF Group | -17.37% | -6.82% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.16 | 1.32 | 748.84% |

| Derivatives Contracts | 2 | 29 | 1350.00% |

| I-REIT Turnover | 0.41 | 0.41 | 0.99% |

| I-REIT Deals | 55 | 36 | -34.55% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -17.97% | -3.37% |

| Dow Jones Industrial Average (DJI) | -8.50% | -2.77% |

| FTSE 100 (FTSE) | -0.38% | -1.05% |

| STOXX Europe 600 | -10.38% | -0.94% |

| Shanghai Composite (SSEC) | -11.71% | 1.61% |

| MSCI Emerging Markets | -20.69% | 0.45% |

| MSCI World Index | -17.85% | -2.57% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -22.62% | 3.21% |

| JSE All Share | 1.98% | 0.17% |

| NSE All Share (NGSE) | 13.61% | 1.51% |

| DSEI (Tanzania) | -1.52% | -0.19% |

| ALSIUG (Uganda) | -14.66% | -0.61% |

US indices settled lower with 10 of the 11 S&P 500 sector components declining led by energy stocks which recorded their longest losing streak since December 2018, weighed down by oil prices, followed by losses in health care stocks. Investors’ sentiments were dampened by fears of a potential recession in 2023 as they await November CPI report on Tuesday and the Fed’s interest rate decision on Wednesday.

European stocks dipped reflecting investors’ uncertainty on the direction of interest rate hikes, with European Central Bank and Bank of England set to announce their decision in the coming week. Energy stocks led declines in the STOXX 600 index weighed down by decline in share prices of heavyweights such as Shell and BP, while industrial stocks buoyed the index.

Asia Pacific indices closed the week higher, with Hong Kong’s tech-heavy Hang Seng outperforming its peers, posting a 6.56% gain, supported by growing optimism that the city will follow Beijing’s lead in scaling back anti-Covid measures. The market also recognized gains posted by Financials and Consumer discretionary sectors of 4.4% and 9.5% respectively and tech stocks that are set to be the largest gainers from the region’s reopening.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 10.96% and 11.07% lower at $71.50 and $76.10 respectively. Gold futures prices settled 0.06% higher at $1,810.70.

Week’s Highlights

- Stanbic Bank Kenya’s PMI headline figure rose to 50.9 in November from 50.2 in October, as private sector firms reported renewed expansion in business activity. This, they attributed to new order inflows picking up from local and international customers and favorable weather conditions. With new orders came rising purchases and expansion in inventory, which suffered increasing input and import costs as a result of a bullish dollar, higher taxation and transport costs.

- The World Bank has recommended policy adjustments to the NSSF Act in the 26th edition of Kenya’s Economic Update, which highlights that the mandated contribution rate is notably low, at less than 1% of the average private sector wage. Apart from backing the government’s bid to raise contribution rate, the World Bank has called for enforcing stern regulation of administrative costs, addressing operational inefficiencies to improve business processes and an integration of informal sector pension plan; Haba Haba into a centralized administrative platform.

- CBK has reinstated charges on bank-to-mobile transactions effective 1st January 2023 that were waived in March 2020 in an effort to facilitate use of mobile money during the pandemic. However, the fees have been slashed by an average 45% to 61% for the various transfers. During this period, CBK noted a monthly increase in the volume and value of peer-to-peer (P2P) transactions by 171% and 71% respectively while those of payment service providers (PSPs) and banks rose by 527% and 410%. The move positions banks to capitalize on the growth and plough back into the digital technology investments in place to contend with the transactions.

- Shelter Afrique has opened negotiations with CMA on the possibility of issuing a $500 million bond to finance its affordable housing projects in East Africa. The developer intends on venturing into capital markets and pension funds in Kenya, Rwanda, Uganda and Tanzania with the promise of decent returns following the successful debut of a $110.7 million Series 1 fixed rate senior unsecured bond issuance in Nigeria.

- Ghana’s Central Bank has proposed a plan to exchange the country’s local bonds worth an estimated 137.3 billion cedis ($10.5 billion) maturing between 2023 and 2029 in a bid to restructure its debt. The plan stipulates that the bonds will be exchanged for new ones maturing in 2027, 2029, 2032 and 2037 with annual coupon rates set at 0% in 2023, 5% in 2024 and 10% from 2025 to maturity. Concurrently, a $1.2 billion stability fund is being set up to cushion the financial sector from the impact of restructuring.

- China’s November inflation dropped to 1.6% year on year from 2.1% in October, matching market expectations and marking the lowest figure since March. The mild CPI drop and 1.3% Producer Price Index (PPI) decline are indicative of weak activity and lower demand as a result of Covid restrictions that have disrupted production.

- The World Gold Council, in its Gold Outlook 2023, reports that a mixed set of influences ranging from high uncertainty surrounding the global economy, recession concerns; falling yet elevated inflation and a possible end to hawkish rate hikes, suggest a stable but positive performance for gold. The key take-aways from the report include optimism around China’s economic growth which should boost consumer gold demand, further anticipated weakening of the dollar as US inflation recedes could provide support for gold and geopolitical tensions which continue to make gold a valuable risk hedge.

Get future reports

Please provide your details below to get future reports: