Foreign Exchange Reserves

The usable foreign exchange reserves remained adequate at USD 7,415 million (4.15 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover. However, it does not meet EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Sterling Pound and the Euro to exchange at KES 123.84, KES 150.60 and KES 133.32 respectively. The observed depreciation against the Dollar is attributable to increased demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 0.33% | 0.23% |

| Euro | 1.26% | 1.38% |

| Sterling Pound | 1.26% | 1.70% |

Liquidity

Liquidity in the money markets increased with the average interbank rate dipping to 5.21% from 6.24%, as government payments offset tax remittances. Remittance inflows totaled $357.30 million in December 2022, a 3.43% increase from $345.45 million in November and 1.92% increase from $350.56 million in December 2021. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.24% | 5.21% |

| Interbank volume (billion) | 0.87 | 26.29 |

| Commercial banks’ excess reserves (billion) | 12.70 | 12.20 |

Fixed Income

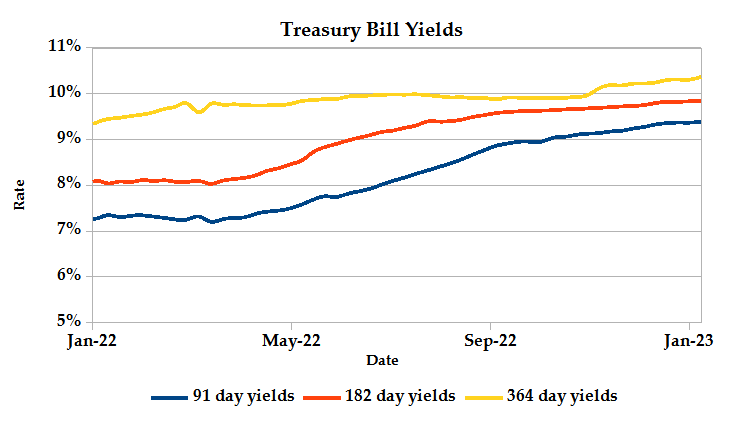

T-Bills

T-Bills were over-subscribed during the week, with the overall subscription rate coming in at 108.88% from 131.65% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 392.34% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 57.70% and 46.68% respectively. The acceptance rate picked up 0.58% to close the week at 99.94%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover rose 507.80% from KES 1.94B in the previous week to KES 11.81B. Total bond deals increased by 146.77% from 186 in the previous week to 459.

In the primary bond market, CBK released auction results for FXD1/2020/005 and FXD1/2022/015 which sought KES 50.0 billion. The issues had a performance rate of 83.26%, receiving bids worth KES 41.63 billion, out of which KES 31.51 billion was accepted at an average rate of 12.88% and 14.19% respectively.

Eurobonds

In the international market, yields on Kenya’s Eurobonds declined by an average 0.30% compared to the previous week and 0.43% year to date. The yields on the 10-year Eurobond for Ghana increased while that of Angola declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | -0.79% | -0.79% | -0.64% |

| 2018 10-Year Issue | -0.36% | -0.36% | -0.27% |

| 2018 30-Year Issue | -0.23% | -0.23% | -0.14% |

| 2019 7-Year Issue | -0.50% | -0.50% | -0.22% |

| 2019 12-Year Issue | -0.45% | -0.45% | -0.35% |

| 2021 13-Year Issue | -0.26% | -0.26% | -0.18% |

Equities

NASI, NSE 20 and NSE 25 settled 2.83%, 0.59% and 1.22% lower compared to the previous week bringing the year to date performance to -3.20%, 1.18% and -0.71% respectively. Market capitalization lost 2.84% from the previous week to close at KES 1.92 trillion recording a year to date decline of 3.21%. The performance was driven by losses recorded by large-cap stocks such as Safaricom, KCB and EABL of 6.38%, 1.28% and 0.72% respectively. These were however mitigated by gains recorded by Standard Chartered, Equity and ABSA of 3.32%, 2.20% and 1.66% respectively.

The Banking sector had shares worth KES 554M transacted which accounted for 47.74% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 233M transacted which represented 20.14% and Safaricom, with shares worth KES 350M transacted represented 30.18% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Standard Group | 0.48% | 20.14% |

| Liberty | 9.52% | 18.45% |

| Sanlam | -5.64% | 13.85% |

| Express | 10.15% | 13.33% |

| EA Cables | 18.82% | 12.22% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| TP Serena | -7.69% | -13.67% |

| Bamburi | -7.63% | -7.63% |

| EA Portland | 2.06% | -6.97% |

| Total | -6.08% | -6.67% |

| Safaricom | -8.52% | -6.38% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.00 | 1.74 | 100.00% |

| Derivatives Contracts | 0.00 | 29.00 | 100.00% |

| I-REIT Turnover | 0.22 | 0.56 | 152.59% |

| I-REIT Deals | 23.00 | 49.00 | 113.04% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 4.57% | 2.67% |

| Dow Jones Industrial Average (DJI) | 3.53% | 2.00% |

| FTSE 100 (FTSE) | 3.84% | 1.88% |

| STOXX Europe 600 | 4.23% | 1.83% |

| Shanghai Composite (SSEC) | 2.53% | 1.19% |

| MSCI Emerging Markets | 6.99% | 4.16% |

| MSCI World Index | 5.18% | 3.24% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -1.89% | 0.03% |

| JSE All Share | 7.07% | 3.37% |

| NSE All Share (NGSE) | 1.78% | 2.52% |

| DSEI (Tanzania) | 0.26% | -0.49% |

| ALSIUG (Uganda) | 0.65% | 0.65% |

US major indices posted strong weekly gains, with financial sector stocks giving S&P 500 the most support, as banks such as JPMorgan Chase & Co and Bank of America Corp beat their quarterly earnings estimates. Markets also reflected the University of Michigan’s survey findings that showed an improvement in consumer sentiment as the one-year inflation outlook for January fell.

European stocks ended the week higher, closing at a near nine-month high, supported by healthcare and banking stocks as well as Britain’s economic outlook which was boosted by a 0.1% growth in November.

Asia Pacific indices edged higher, with technology-heavy bourses in Taiwan, South Korea and Hong Kong recording the highest gains as treasury yields and the dollar retreated on soft inflation numbers. China markets rose on general optimism of economic rebound as the country reopens its borders.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 8.67% and 8.54% higher at $80.08 and $85.28 respectively. Gold futures prices settled 2.78% higher at $1,921.70.

Week’s Highlights

- Energy and Petroleum Regulatory Authority (EPRA) released the monthly statement on maximum retail prices of petroleum products which will be in force from 15th January 2023 to 14th February 2023. Pump prices remained unchanged at KES 177.30 per litre for Super Petrol, KES 162.00 per litre for Diesel and KES 145.94 per litre for Kerosene. The subsidy on Kerosene has been maintained at KES 25.13 per litre while the price of Diesel has been cross-subsidized with that of Super Petrol.

- Commercial banks in Kenya reduced their lending to the State through investment in government securities to KES 64.87 billion for the period ending 30th December 2022, down from KES 169.74 billion in 2021. This was partly attributed to paper losses amid rising yields as the MPC raised the benchmark rate as well as capital reallocation to the private sector as demand rose. World Bank has raised an alarm on the banking sector’s exposure to sovereign debt risk as a result of rising government debt vulnerability.

- Nairobi City County Government (NCCG) has engaged CMA on actualizing one of the Authority’s visions that 30% of counties financing be raised from capital markets. As a result, CMA has pledged support for NCCG’s intention to issue a green bond and the potential listing of County agencies such as Nairobi Water and Sewerage Company to acquire long-term financing to meet development needs.

- Insurance Regulatory Authority’s Q3 2022 Industry Release Report indicated that the total industry exposure to capital market investments (quoted shares) dropped from 4.3% in Q3 2021 to 3.0% in Q3 2022, while slightly picking up from 2.8% in Q2 2022. The quarter was characterized by the first positive performance in the equities market since Q3 2021, showing signs of a rebound.

- The High Court has temporarily suspended the recently reintroduced bank to mobile money transaction charges after a petition was filed claiming that the charges should not be borne by customers. The petition case which is set to be mentioned on 23rd January 2023, argues that Safaricom’s engagement is with its M-Pesa Paybill clients who are mainly banks and other financial institutions, essentially being the service recipients should shoulder the costs.

- The US Labor Department announced December CPI report, showing a 9.4% monthly drop in gas prices, while food prices maintained a moderate 0.3% increase. Rent and utility prices remained elevated during the month. Core inflation slowed to 5.7% year-on-year, from 6% in November, while the headline CPI figure dipped to 6.5% from 7.1%.

- World Bank has revised 2023 global growth down to 1.7% in 2023 from 3% reported in June 2022 and 2.7% in 2024. This follows a slowdown in projected growth in advanced economies from 2.5% in 2022 to 0.5% in 2023 while growth in emerging markets and developing economies is expected at 2.7% in 2023 from 3.8% in 2022. Emerging markets growth has been driven down by heavy debt burdens and weak business investments, piling on existing ailing education, healthcare, poverty and infrastructure.

Get future reports

Please provide your details below to get future reports: