MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) held a meeting on April 29 to assess the economic impact and the outcomes of policy measures deployed in March to mitigate the adverse economic and financial impact of COVID-19. The Committee noted that the policy measures were having the intended effect on the economy, and were still being transmitted. Given the continuing adverse economic outlook, the MPC decided to augment its accommodative monetary policy stance by lowering the Central Bank Rate (CBR) to 7.00% from 7.25%. The Committee decided to reconvene within a month.

- The Kenya National Bureau of Statistics (KNBS) released the Economic Survey 2020, indicating that the economy had grown by 5.4% in 2019, from 6.3% recorded in 2018. The slower growth can be attributed to; a slower growth of 3.6% in agriculture, forestry and fishing sector and a slower of growth of 3.2% in the manufacturing sector. The financial and insurance sector, and tourism sector grew by 6.6% and 3.9% respectively.

- Additionally, the World Bank released the Kenya Economic Update, April 2020. According to the report, Kenya’s GDP growth for 2020 is expected to come in at 1.5%, with a potential downside scenario of a contraction to 1.0 percent, if COVID-19 related disruptions in economic activity last longer.

- The Retirement Benefits Authority(RBA) allowed companies adversely affected by COVID-19 pandemic to apply for suspension of retirement benefits contribution. However, companies that have filed winding up notice will bear full costs of employee and employer pension obligations.

- The president assented the Tax Amendments Bill 2020, which will allow salaried persons to use part of their retirement savings to secure home loans. The amendment will remove the restriction which prohibits schemes from using their funds to offer direct or indirect loans to any person.

- Vodacom and Safaricom announced that they had completed the acquisition of the M-PESA brand, product development and support services from Vodafone through a newly-created joint venture. The transaction, which was first announced in 2019, will accelerate M-PESA’s growth in Africa by giving both Vodacom and Safaricom full control of the M-PESA brand, product development and support services as well as the opportunity to expand M-PESA into new African markets.

- The NSE derivatives market(NEXT) released its Q1 2020 trading performance results. The market offered positive returns for investors who held short positions as markets experienced a decline. Net returns on Exposure of Kshs 25million generated returns of 203.01%, 249.26%,293.32%,126.18%,116.14%,118.15%, and 360.70% for investors with short positions in Safaricom, KCB, Equity, ABSA, BAT Kenya, EABL and NSE 25 futures respectively. NEXT offered low margin requirements and lower trading fees for investors allowing them to break even quickly on their positions.

- The Energy & Petroleum Regulatory Authority (EPRA) announced new prices of petroleum products that will be in force from 15th April to 14th May 2020. Super Petrol, Diesel and Kerosene decreased by 16.2%, 4.0% and 19.0% respectively to prices of Kshs 92.9, Kshs 97.6 and Kshs 77.3. The changes follows a drop in the average landed cost of imported Super Petrol, Diesel and Kerosene by 30%, 9.89% and 37.70% respectively. This is expected to depress the transport index and prices of other commodities.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 1.65% to stand at USD 7.74 billion(4.66 months of import cover).

However, this meets the CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

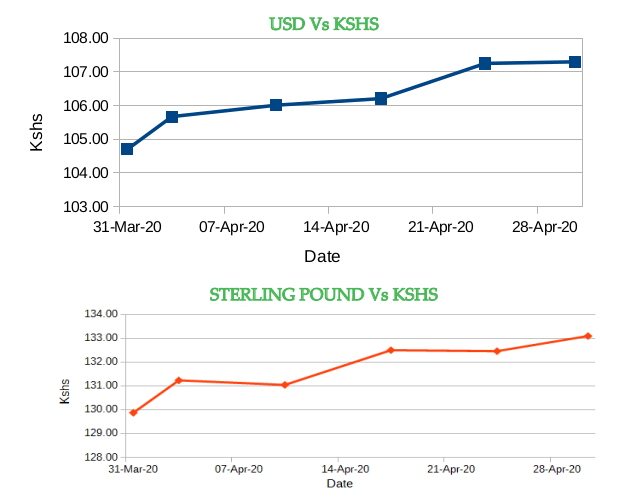

The Kenyan Shilling depreciated against the USD by 2.48%, exchanging at Kshs 107.29 at the end of the month up from Kshs 104.69 in the previous month. The depreciation is due to increased dollar demand and reduced foreign exchange inflows amid economic uncertainty engendered by the COVID-19 pandemic disrupting global supply chains and reduced diaspora remittances.

Inflation

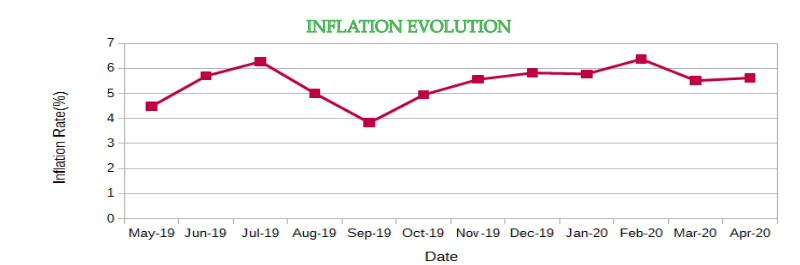

The overall year on year inflation increased to 5.62% in the month of April up from a revised figure of 5.51% in March. The increase is attributable to increase in Food and Non-Alcoholic Drinks’ Index by 1.77% and Housing, Water, Electricity, Gas and Other Fuels’ Index by 0.41%. During the same period, the Transport Index increased by 1.32% mainly due to increase in prices of matatu and taxi fares.

Liquidity

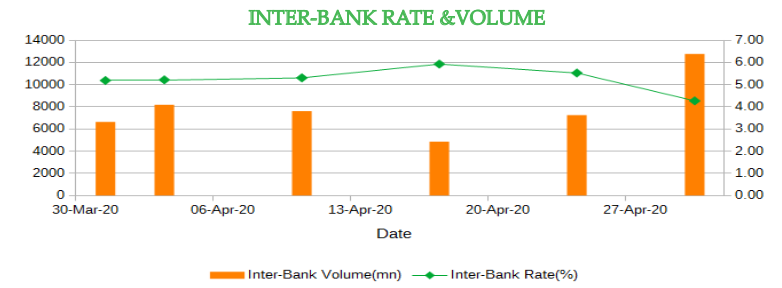

During the month, liquidity increased as a result of government payments which partly offset tax receipts and auction of government securities. The inter-bank rate decreased to 4.27% down from 5.19%. The volume of inter-bank transactions increased from Kshs 6.64billion to Kshs 12.78billion.Commercial banks excess reserves increased to Kshs 42.70 billion.

FIXED INCOME

T-Bills

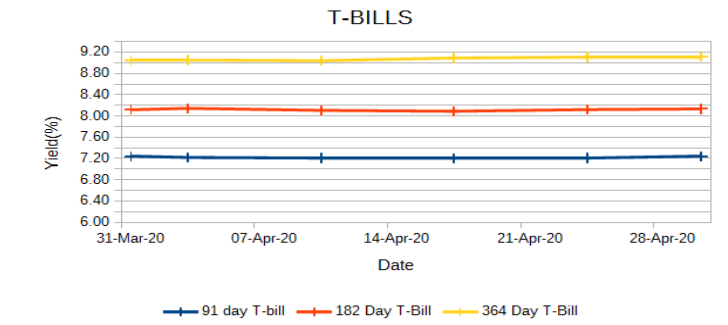

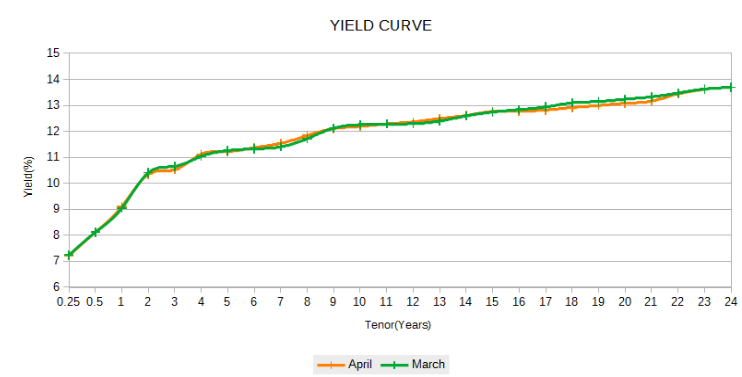

The T-bills recorded an overrall subscription rate of 72.8% at the end of month of April, compared to 151.0% recorded in the previous month. The undersubscription is partly attributable to investors’ low confidence in the market. The performance of the 91-day, 182-day and 364-day papers stood at 86.8%, 28.4% and 111.7% respectively. On a monthly basis, the yields on the 182-day and 364-day papers increased by 0.20% and 0.8% respectively to 8.13% and 9.12%.

On the other hand, the yield on the 91-day paper remained relatively unchanged at 7.24%.

T-Bonds

At the end of the month, the T-Bonds registered a turnover of Kshs 6.67billion from 420 bond deals. This represents a weekly decrease of 21.4% and 1.4% respectively. The yields on government securities in the secondary market remained relatively stable during the month of April.In the international market, yields on Kenya’s Eurobonds declined by an average of 39.42 basis points.

EQUITIES

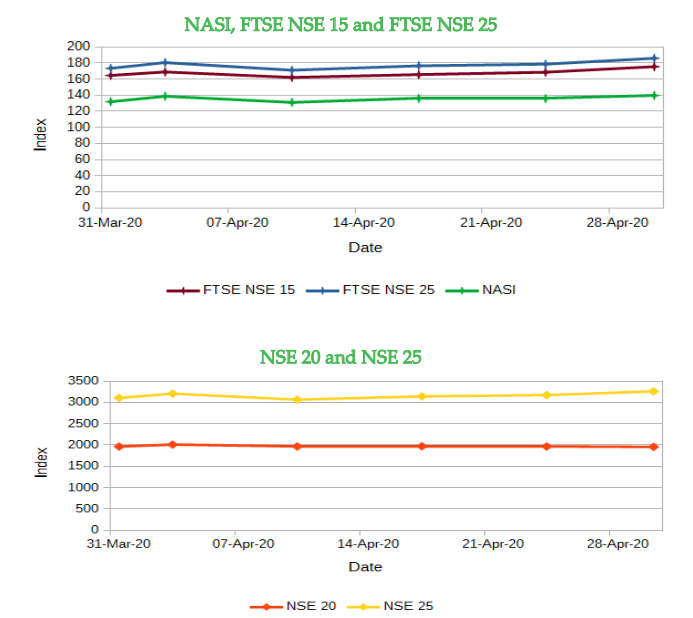

During the month of April, the market capitalization rose by 5.90% to Kshs 2.14 trillion. However, total shares traded and equity turonver plunged by 48.7% and 62.4% respectively to 68 million shares and Kshs 1.6billion. NASI and NSE 25 gained by 5.9% and 4.9%in that order, while NSE 20 dropped by 0.41% on a monthly basis. On a weekly basis, the NASI and NSE 25 gianed by 2.9% and 2.8% respectively while NSE 20 declined by 0.5%. The gain in NASI is as a result of appreciation of large-cap stocks such as EABL, Equity Group, Safaricom and Co-operative Bank.

ALTERNATIVE INVESTMENTS

- During the last week of the month, the I-REITs market recorded a turnover of Kshs 1.2million with 36 contracts. The Derivatives market registered a turnover of Kshs 14000 with 1 contract.

- Health technology e-commerce company focused on women’s health, Kasha, received $1million investment from Finnish financier, Finnfund. The funding is set to increase the company’s presence in Rwanda and Kenya, and to support its expansion into other African countries.

- The World Bank through it private lending arm, the International Finance Corporation (IFC), is set to acquire $15million minority stake in Naivas. The capital injection is meant for expansion of Naivas’ growth strategy in the short term period, increasing the number of its branches strategically countrywide and scaling up the more capital-intensive food market.

- Swiss impact asset manager responsAbility Investments and EDFI ElectriFI announced their cooperation in the field of climate finance in emerging economies. Under the agreement, EDFI ElectriFI is providing additional first-loss capital for a responsAbility-managed energy debt fund targeting universal access to clean power.

- During the month, major global markets gained as investors look forward to easing up of measures put across to deal with the COVID-19 pandemic. In the USA, the S&P 500 and Dow Jones indices gained by 12.68% and 11.08% respectively from the previous month.

In Europe, the continental index of STOXX Europe 600 and UK’s FTSE 100 appreciated by 6.24% and 4.04% respectively, however, at a lower rate than the USA as most European countries are still under strict lockdown measures. - On a regional front, most markets were on an upward tend and outperformed the Kenyan stock market apart from Uganda All Share Index. The FTSE ASEA Pan African index, representing the overall African markets, gained by 6.28% from the month of March. South Africa’s JSE All Share went up by 13.14%, Nigeria’s All share index rose by 8.08% and Tanzania’s DSEI increased by 36.62%. However, the Uganda’s All Share Index declined by 21.78%.

- On the global commodities markets, the oil futures indices continued to experience volatility even after talks by OPEC countries and Russia to cut oil production. The Crude Oil WTI futures plunged by 8.01% from the previous month of March, while recording historical negative prices within the month. However, the ICE Brent Crude Oil increased in value by 11.13%.

- During the month, major global economies declined in production with some entering recession such as the French economy which entered a recession having recorded a 6% drop in the first quarter of 2020, its worst since 1945, and having shrank by 0.1% in the last three months of 2019 . China’s GDP also shrunk by 6.8% from Q1 2019 and 9.8% in the first three months of 2020 while Italy’s GDP declined by 4.7% in Q1 2020.

Get future reports

Please provide your details below to get future reports: