MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) held a meeting on September 29 and decided to raise the Central Bank Rate (CBR) from 7.50% to 8.25%.

- Inflation increased in September 2022 due to increases in food and fuel prices. Food inflation remained elevated largely due to the impact of supply chain disruptions. Overall inflation is expected to remain elevated in the near term, due in part to the scaling down of the government price support measures, resulting in increases in fuel and electricity prices, the impact of tax measures in the government budget and global inflationary pressures.

- Volatility in global financial markets surged due to the significant strengthening of the dollar, and monetary and fiscal policy stance in advanced economies to curb inflationary pressures. Inflation in developed economies remains elevated due to high oil and gas prices and lingering supply chain challenges, despite recent moderation in commodity prices.

- Global economic outlook has weakened, due to the impact of a rapid tightening of monetary policy in advanced economies particularly the U.S, the ongoing war in Ukraine, and the lingering pandemic-related disruptions particularly in China.

- Private capital investment in Africa, in the first half of 2022 had one of the strongest half-years of private capital activity ever recorded. According to a report by the African Private Equity and Venture Capital Association (AVCA), this was attributable to the substantial amount of fresh capital raised by fund managers in 2021, an increasing interest in Africa’s venture ecosystem by international investors and domestic venture capital firms.

- Nigeria’s central bank raised its benchmark interest rate as it seeks to curb rising inflation. The recent hike means the country has now raised borrowing costs significantly, making it one of four central banks on the continent that have hiked by 300 basis points or more this year.

- The Sterling pound fell below Sh130 against the shilling for the first time since the peak of Covid restrictions. This signals a lower cost of imports from the UK while hurting export earnings for farm produce. The pound is among the major international currencies that have been falling against the US dollar amid continued increases in interest rates by the Federal Reserve to curb inflation.

- The UK entered into recession as the Bank of England voted to raise its base rate in order to curb inflation. The bank noted volatility in wholesale gas prices but said announcements of government caps on energy bills would limit further increases in consumer price index inflation.

- Foreign investors looking for merger and acquisition deals in East Africa are facing challenges when valuing potential targets due to low-quality financial data. This is potentially costing the region valuable foreign direct investment inflows. Private equity, venture capital funds and development finance institutions (DFIs) have over the years expressed concerns about asset quality and valuation of local businesses, pointing out the possibility of overpaying for low-quality investments.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves increased by 0.66% to stand at USD 7.42 billion (4.19 months of import cover). This meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover but below the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

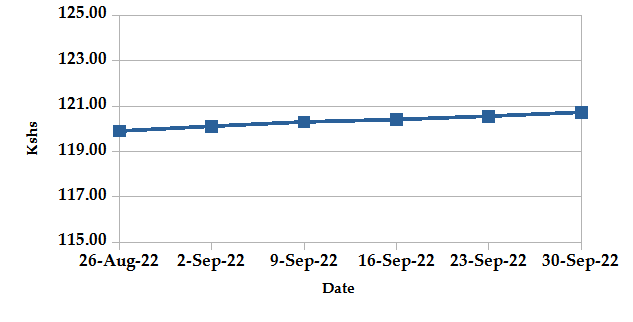

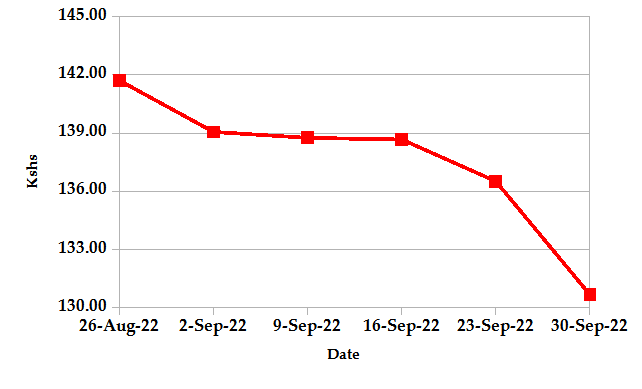

The Kenyan Shilling depreciated against the USD by 0.60%, exchanging at Kshs 120.73 at the end of the month up from Kshs 120.01 in the previous month. The depreciation is due to increased dollar demand in the energy, oil and manufacturing sectors. The Shilling gained against the Sterling Pound by 7.00%, exchanging at Kshs 130.66 at the end of the month down from Kshs 140.50 in the previous month. The gain is due to investor concerns of the government tax cut plan despite financial stability concerns.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

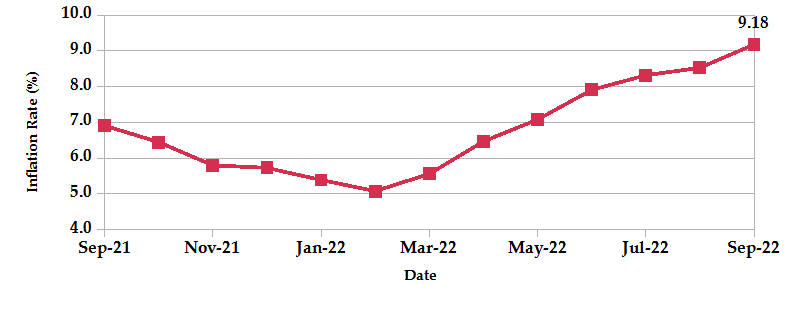

The overall year-on-year inflation increased to 9.18% in the month of September up from a revised figure of 8.53% in August. The increase is attributable to a rise in food and fuel prices due to persistent supply chain disruptions and rising global energy prices.

INFLATION EVOLUTION

Liquidity

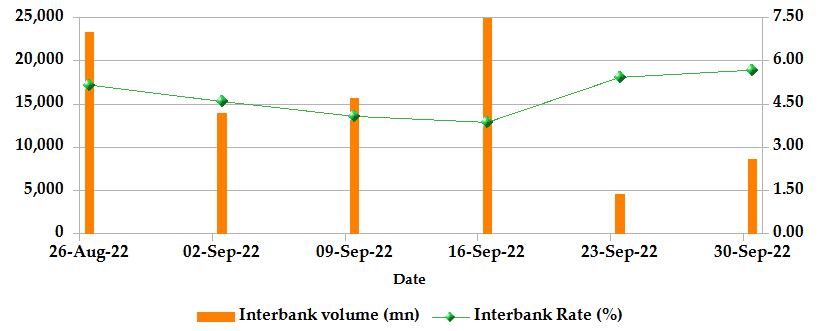

During the month, liquidity decreased as a result of tax receipts which partly offset government payments. The inter-bank rate increased to 5.68% up from 5.00%. The volume of inter-bank transactions decreased from Kshs 12.57 billion to Kshs 8.69 billion. Commercial banks excess reserves decreased from Kshs 42.40 billion to Kshs 13.40 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

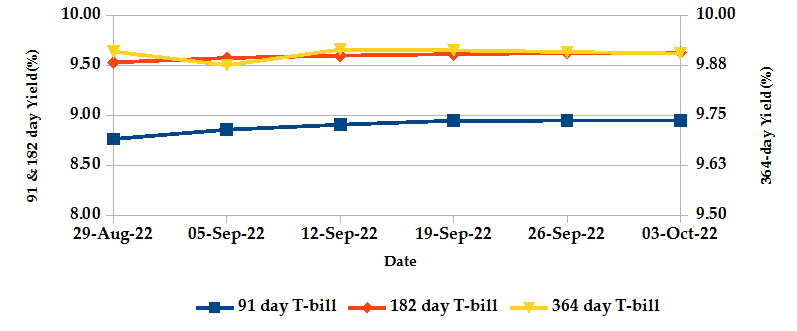

The T-bills recorded an overall subscription rate of 83.9% at the end of the month of September, compared to 70.9% recorded in the previous month. The undersubscription is partly attributable to tightened liquidity. The performance of the 91-day, 182-day and 364-day papers stand at 292.5%, 65.2% and 19.0% respectively. On a monthly basis, the yields on the 91-day and 182-day papers increased by 2.11% and 1.04% respectively to 8.95% and 9.63%. On the other hand, the yield on the 364-day paper remained relatively unchanged at 9.91%.

T-BILLS

T-Bonds

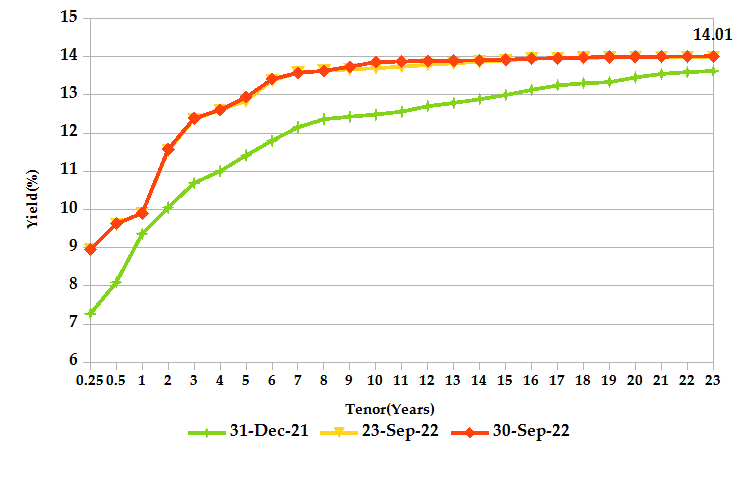

At the end of the month, the T-Bonds registered a turnover of Kshs 3.25 billion from 112 bond deals. This represents a weekly increase of 6.8% and 8.7% respectively. The yields on government securities in the secondary market slightly increased during the month of September.

In the international market, yields on Kenya’s Eurobonds increased by an average of 248.9 basis points.

YIELD CURVE

EQUITIES

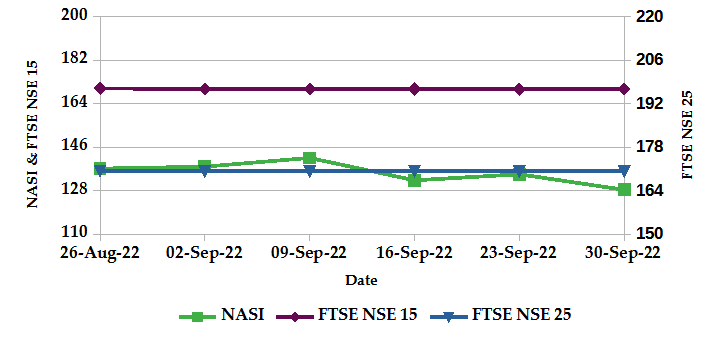

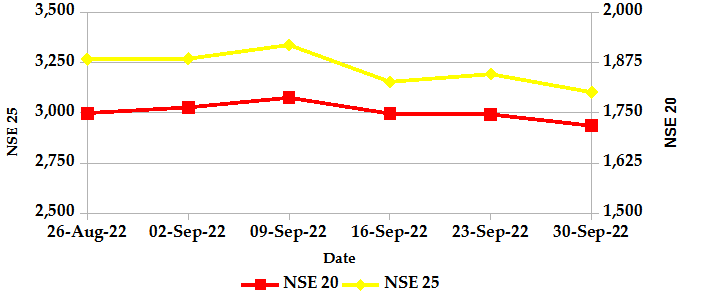

During the month of September, the market capitalization declined by 6.60% to Kshs 2.00 trillion. Also, total shares traded and equity turnover plunged by 34.0% and 39.1% respectively to 57 million shares and Kshs 1.5 billion. NASI, NSE 20 and NSE 25 declined by 6.6%, 1.9% and 4.7% respectively on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 declined by 4.8%, 1.6% and 2.8% respectively. The decline in NASI is a result of the depreciation of large-cap stocks such as EABL, Equity Group, Safaricom and Co-operative Bank.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 153 contracts having a turnover of Kshs 18.3 million which was an increase from 163 contracts having a turnover of Kshs 7.0 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.3 million with 152 deals which was a decrease from Kshs 8.5 million with 153 deals recorded over the last month.

- The ETF market over the month recorded a turnover of Kshs 44.4 million with 2 deals which was an increase from no deals recorded over the last month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -2.91% | -9.34% |

| STOXX Europe 600 | -0.65% | -6.57% |

| Shanghai Composite (SSEC) | -2.07% | -5.55% |

| MSCI Emerging Market Index | -3.32% | -11.90% |

| MSCI World Index | -2.45% | -9.46% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -1.16% | -4.24% |

| JSE All Share | 0.49% | -5.51% |

| NSE All Share (NGSE) | -0.01% | -1.63% |

| DSEI (Tanzania) | 0.10% | -1.93% |

| ALSIUG (Uganda) | 0.51% | -1.32% |

- During the month, major global markets declined as major central banks tightened their monetary policy stance to tame inflation. In the USA, the S&P 500 and Dow Jones indices declined by 9.34% and 8.83% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 declined by 6.57% and 5.36% respectively as European shares saw sharp losses due to rising interest rates and high inflation increasing investor uncertainty. Markets have been turbulent since the Russia-Ukraine war sent gas prices soaring, leading to rampant inflation, which sparked aggressive rate hikes from central banks and worries about a subsequent growth slowdown.

- On a regional front, most markets declined due to persistent inflation driven by rising energy prices. The FTSE ASEA Pan African index, representing the overall African markets declined by 4.24% from the month of August. South Africa’s JSE All Share declined by 5.51%, Nigeria’s All Share Index declined by 1.63%, Tanzania’s DSEI declined by 1.93% and Uganda’s All Share Index declined by 1.32%.

- On the global commodities markets, the oil futures indices declined over concerns of interest rate hikes as most major central banks took measures to curb inflation. The Crude Oil WTI futures plunged by 11.23% from the previous month of August and the ICE Brent Crude Oil declined by 8.84%.

Get future reports

Please provide your details below to get future reports: