The Monetary Policy Committee (MPC) of the Central Bank of Kenya raised the Central Bank Rate (CBR) from 10.50% to 12.50% during its meeting on 5th December 2023. This decision comes amidst persistent domestic inflationary pressures and a depreciating Shilling, which are driving a rising cost of living and eroding purchasing power for households. The MPC also emphasized its ongoing commitment to monitoring the impact of its policies and the evolving global and domestic economic environment. It stands ready to take further steps to tighten monetary policy as circumstances warrant.

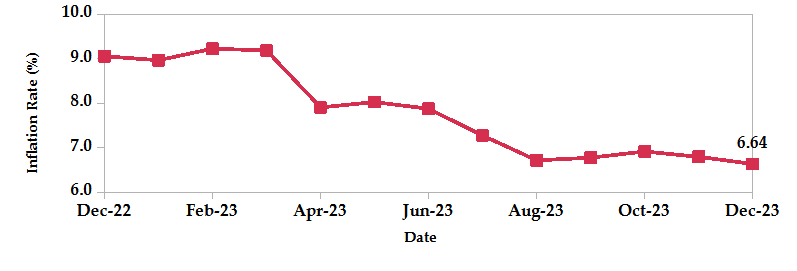

Inflation decreased to 6.64% in December, down from 6.8% in November, marking the lowest rate recorded since April 2022. The food and non-alcoholic beverages index rose slightly by 0.3%, a lower pace compared to the previous month’s 0.4%, attributed to higher food prices. The housing, water, electricity, gas and other fuels index edged up 0.4% due to higher electricity costs. Notably, despite a drop in petrol and diesel prices, the transport index rose 0.5%, owing to a hike in fare prices on some routes.

Kenya’s GDP rose by 5.9% year-on-year in Q3 2023, surpassing the 5.5% rise in the previous quarter. This marks the strongest economic expansion since Q1 2022, spearheaded by a resilient agricultural sector that grew by 6.7%. Other sectors also thrived, with manufacturing up 2.6%, finance and insurance up 14.7%, information and communication up 7.3%, and accommodation and food services up 26%. On a quarterly basis, GDP rose to 1.3%, up from 1.1% in Q2.

Kenya and the EU signed an Economic Partnership Agreement (EPA), promising a 27% surge in bilateral trade. This unlocks duty-free access for Kenyan businesses to the vast EU market, paving the way for job growth in key sectors like manufacturing and agriculture. The EPA ensures responsible growth for both parties by setting a new standard with its ambitious provisions on gender equality, labor rights and climate change.

The World Bank approved a $150 million project, the Kenya Jobs and Economic Transformation Project (KJET), designed to empower 6,800 women-led businesses and create 45,000 new or improved jobs across the country. KJET will fuel the growth of micro, small and medium enterprises (MSMEs) by strengthening their value chains, opening doors to new markets and upgrading their skills and capacity.

Ethiopia has officially defaulted on its international debt, failing to make a key $33 million interest payment that was due on 11th December 2023. This marks the country’s formal entry into sovereign default, following similar recent struggles by Zambia, Sri Lanka and Ghana.

The US Q3 GDP revised higher to 5.2%, exceeding forecasts of 5% and marking the strongest pace since Q4 2021. Non-residential investment jumped from -0.1% to 1.3%, due to upward revisions and a 6.9% increase in structures. Residential investment recorded its first gain in nearly two years, rising 6.2%. Consumer spending, though slightly slowing from its initial 4% estimate to 3.6%, remained robust, particularly in goods purchases. Trade also contributed positively, with exports rising 6% and imports moderating to 5.2%.

China’s Caixin PMI rose to 50.8 in December, exceeding forecasts and marking a seven-month high. Output roared back, new orders surged at their fastest pace since February, and new export orders eased at their slowest in six months. However, the positive momentum was tempered by ongoing job losses, the first decline in backlogs since May, and stagnating purchasing activity. Supply chain disruptions eased, but cost pressures remained subdued despite modest increases in input and output costs.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves declined by 1.90% to settle at USD 6.61 billion (3.50 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

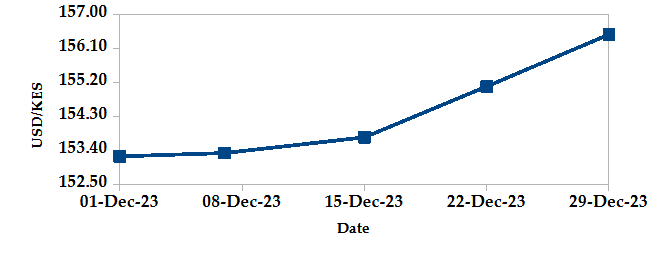

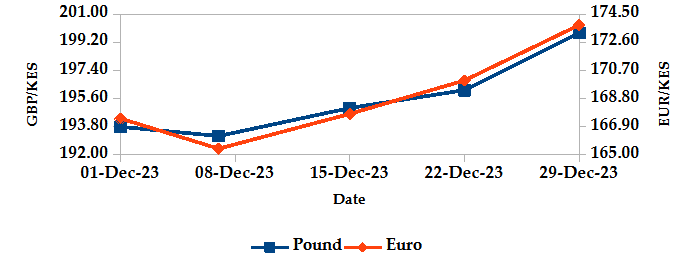

The Kenyan Shilling depreciated against the USD, the Sterling Pound and the Euro by 2.16%, 2.75% and 3.31%, exchanging at Kshs 156.46, Kshs 199.80 and Kshs 173.78 respectively at the end of the month, from Kshs 153.15, Kshs 194.46 and Kshs 168.22 in the previous month. The depreciation against the Dollar is attributed to rising demand from importers, which has caused a shortage in the market.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year on year inflation decreased to 6.64% in December from 6.80% in November. This is primarily driven by lower fuel prices.

INFLATION EVOLUTION

Liquidity

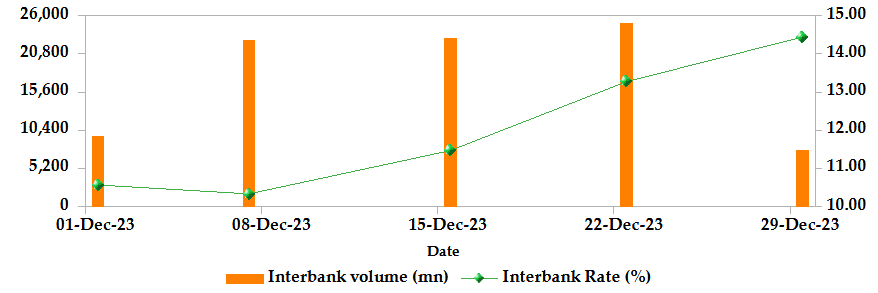

During the month, liquidity tightened as a result of tax remittances which more than offset government payments. The inter-bank rate increased from 10.80% to 14.44%. The volume of inter-bank transactions decreased from Kshs 9.67 billion to Kshs 7.76 billion. Commercial banks excess reserves decreased from Kshs 23.10 billion to Kshs 10.10 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

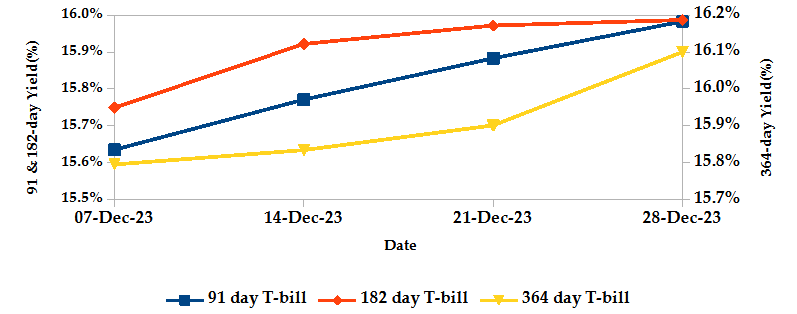

T-bills recorded an overall subscription rate of 89.94% during the month of December, compared to 156.43% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 439.91%, 27.36% and 12.53% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 2.92%, 2.81% and 2.37% to 15.98%, 15.99% and 16.10% respectively as investors aggressively bid to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

T-Bonds

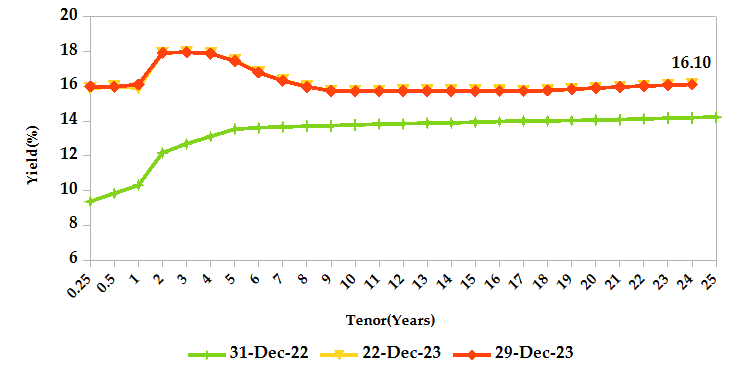

During the month, T-Bonds registered a total turnover of Kshs 52.14 billion from 1,817 bond deals. This represents a monthly decrease of 6.89% and 36.09% respectively. The yields on government securities in the secondary market increased during the month of December.

In the primary bond market, CBK issued a new 3-year bond FXD1/2024/03 and re-opened FXD1/2023/05 through a tap sale, targeting to raise Kshs 35.0 billion. The coupon rate for the reopened bond is 16.84%, while that of the new issue will be market-determined.

In the international market, yields on Kenya’s Eurobonds decreased by an average of 123 basis points.

YIELD CURVE

EQUITIES

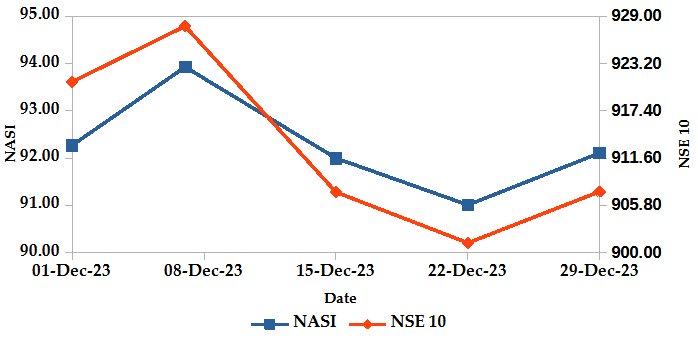

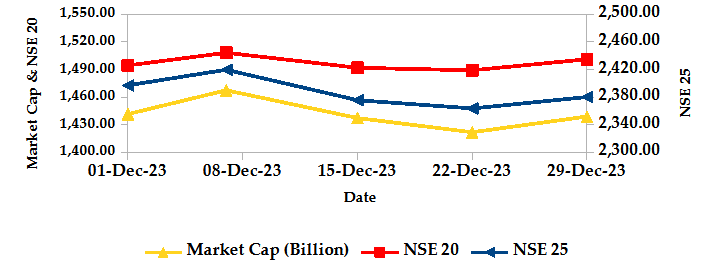

During the month, market capitalization gained 0.19% to settle at Kshs 1.44 trillion. Total shares traded decreased by 35.50% to 199.96 million shares and equity turnover went down 30.16% to close at Kshs 3.01 billion. On a monthly basis, NASI, NSE 20 and NSE 25 settled 0.20%, 0.37% and 0.10% higher, while NSE 10 settled 0.54% lower. The performance was as a result of gains recorded by large cap stocks such as KCB, Stanbic and ABSA of 16.18%, 6.62% and 3.15%. These were however weighed down by the losses recorded by other large cap stocks such as Equity and Safaricom of 7.81% and 1.07%.

NASI and NSE 10

Market Capitalization, NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

The derivatives market, over the month, recorded a turnover of Kshs 3.23 million with 33 contracts, which was a decrease from Kshs 4.70 million with 109 contracts recorded in the previous month.

I-REIT market, over the month, recorded a turnover of Kshs 0.36 million with 34 deals which was a decrease from Kshs 10.46 million with 143 deals recorded in the previous month.

The EFT market recorded no transactions over the month, which was a decrease from Kshs 1.46 million with 1 deal recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

Global Markets

Weekly Change

Monthly Change

S&P 500

4.42%

24.73%

STOXX Europe 600

3.77%

10.33%

Shanghai Composite (SSEC)

-1.81%

-4.54%

MSCI Emerging Market Index

3.71%

6.35%

MSCI World

4.81%

21.85%

Regional Markets

Weekly Change

Monthly Change

FTSE ASEA Pan African Index

-1.11%

2.12%

JSE All Share

1.22%

3.12%

NSE All Share (NGSE)

4.78%

44.92%

DSEI (Tanzania)

0.79%

-7.34%

ALSIUG (Uganda)

-3.22

-28.20%

Global markets were volatile during the month. In the US, the S&P 500 gained 4.42% and the Dow Jones index gained 4.84%, buoyed by stronger-than-expected jobs data, which reinforced confidence in the economic recovery. In Europe, the STOXX Europe 600 and the UK’s FTSE 100 indices edged 3.77% and 3.75% higher, fueled by easing German inflation and anticipated potential rate cuts from the European Central Bank. In Asia Pacific, the Shanghai Composite (SSEC) index lost 1.81%, as investors weighed mixed regional inflation data and dovish hints from the Chinese central bank regarding future rate cuts.

On a regional front, markets recorded mixed performance. The FTSE ASEA Pan African index, representing the overall African markets lost 1.11% from November. South Africa’s JSE All Share Index, Nigeria’s All Share Index and Tanzania’s DSEI gained 1.22%, 4.78% and 0.79% respectively, while Uganda’s All Share index dropped by 3.22%.

On the global commodities markets, oil future indices edged lower, fueled by optimism over interest rate cuts and easing concerns over the Red Sea supply disruptions. Crude Oil WTI futures and ICE Brent Crude Oil settled 5.67% and 4.72% lower to close at $71.65 and $77.04 respectively.

Get future reports

Please provide your details below to get future reports: