Month’s Highlights

Top digital lenders cut lending by more than 50% to Ksh 2 billion a month after CBK kicked them out of credit reference bureaus, a move that denied members borrower profiles necessary for making quick lending decisions. They are therefore not able to verify customers’ credit details and fear of risk of default.

Kenya will start to gradually cut duty on goods from the UK seven years after the post-Brexit trade agreement with the UK is enforced, giving time for domestic firms to enhance their competitive advantage. Kenya offers to open 82.6% value of total trade to the UK, thus flooding the local market with finished and unfinished goods excluding agricultural and industrial products. British firms will ship in goods duty-free for 25 years thereafter.

BOC Kenya has opted not to recommend the company’s takeover by Carbacid Investments to its shareholders after an independent advisor hired to review the transaction declared Carbacid’s offer of sh.63.5 per BOC share as an undervaluation. Carbacid’s six months revenue increased to KSh449.7 million, a 27% improvement from the KSh352.9 million revenue earned in the same period in 2019.

Interest rates on fixed deposits dropped to an eight-year low of 6.3% from 7.1% in 2019, on bankers reduced appetite for savings as a result of increased fixed deposits from wealthy investors due to reduced investment opportunities and subdued demand for loans.

Kenya intends to create a special fund for settling fast-maturing loans in the next financial year as a way of mitigating future cash-flow crisis arising from heavy debt repayments. The treasury will come up with and gazette rules for the establishment of the fund to specifically pay off maturing debts, buy back bonds when interest rates are low and retire some of the debts early to avoid higher costs in the future. The current debt maturities are projected to jump by 65.17% to 493.12 billion in the next two fiscal years.

Acorn Holdings has quoted its two development and income REITs products worth 7.5 billion at NSE’s recently opened unquoted securities platform, whose main objective is to offer a more transparent over-the-counter marketplace for shares of unlisted companies. The company seeks to grow its capacity in student hostels.

Uganda Manufacturers Association have signed an agreement to encourage manufacturers to list on the Uganda Securities Exchange (USE). While players in the manufacturing sector are optimistic about huge capital fundraising opportunities, it is not clear how much cash the capital markets sector is willing to provide in an environment where many investors are reluctant to pump a lot of money into one sector at the expense of other rewarding sectors.

Gold was down in Asia, with higher U.S. Treasury yields and the U.S. Federal Reserve Chairman’s commitment to current ultra-easy monetary policy all putting a dent in Gold’s appeal for investment.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 0.76% to stand at USD 7.61 billion (4.67 months of import cover). However, this meets the CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

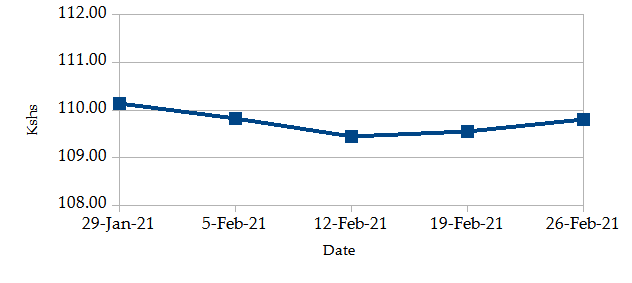

The Kenyan Shilling gained against the USD by 0.31% exchanging at Kshs 109.80 at the end of the month down from Kshs 110.14 in the previous month. The appreciation is due to decreased dollar demand from general importers due to the closing of major Asian markets due to the Lunar New Year holiday.

USD Vs KSHS

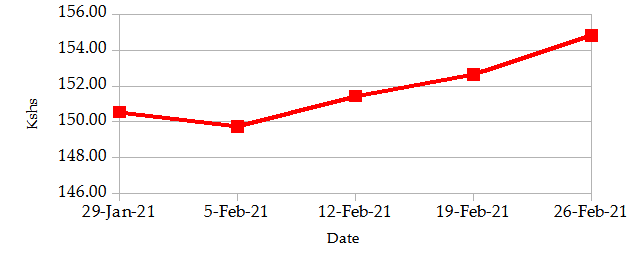

STERLING POUND Vs KSHS

Inflation

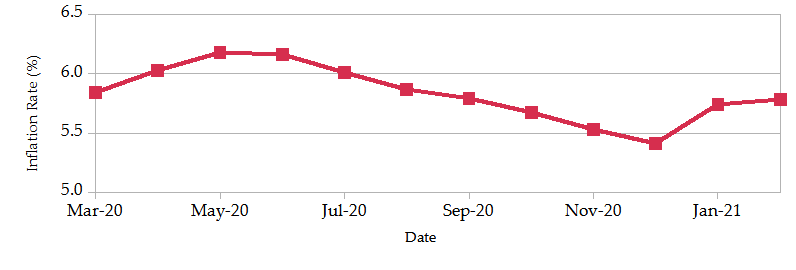

The overall year-on-year inflation increased to 5.78% in the month of February up from a revised figure of 5.74% in January. The increase is attributable to the 0.1% increase in the Food and Non-Alcoholic Drink’s Index due to increases in prices of cabbages, spinach and cooking oil, 0.4% increase in the Housing, Water, Electricity, Gas and Other Fuels’ Index due to increase in the price of kerosene and a 2.3% increase in the Transport Index driven by increase in the prices of diesel and petrol.

INFLATION EVOLUTION

Liquidity

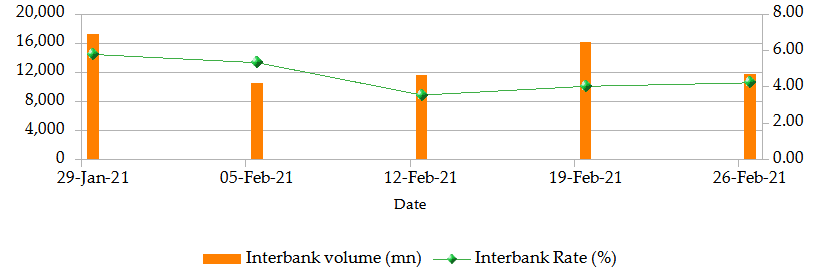

Liquidity increased during the month of February as a result of government payments. The interbank rate decreased to 4.23% from 5.79%. The volume of inter-bank transactions decreased from Kshs 17.25 billion to Kshs 11.73 billion. Commercial banks excess reserves decreased to Kshs 12.5 billion from 13.7 billion in January.

INTER-BANK RATE and VOLUME

FIXED INCOME

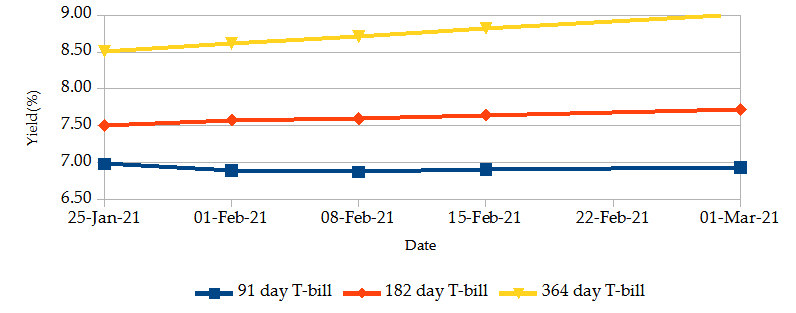

T-Bills

The T-bills recorded an overall subscription rate of 94.70% at the end of the month of February, compared to 66.84% recorded in the previous month. The increase in subscriptions is due to an increase in market liquidity from a decline in inter-bank rate to 4.2% from 5.8%. The performance of the 91-day, 182-day and 364-day papers stand at 62.82%, 52.17% and 149.99% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 0.49%, 1.90% and 4.53% respectively to 6.93%, 7.72% and 9.01%.

T-BILLS

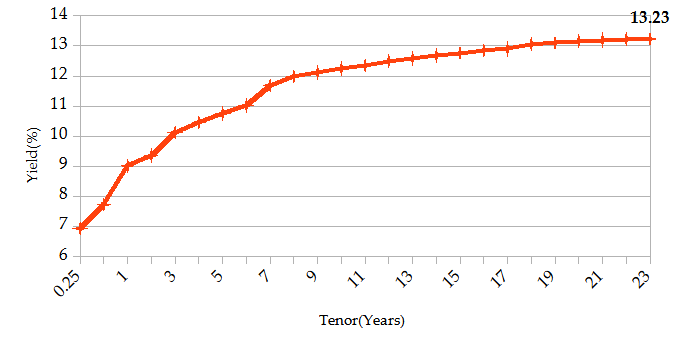

T-Bonds

Over the month of February, the T-Bonds registered a total turnover of Kshs 15.08 billion from 365 bond deals. This represents a monthly decrease of 71.39% and 64.73% respectively. The yields on government securities in the secondary market remained relatively stable during the month of February.

In the international market, yields on Kenya’s Eurobonds remained stable, increasing marginally by an average of 0.6 basis points.

YIELD CURVE

EQUITIES

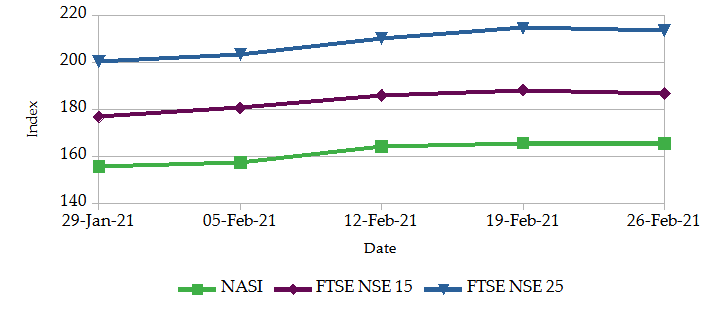

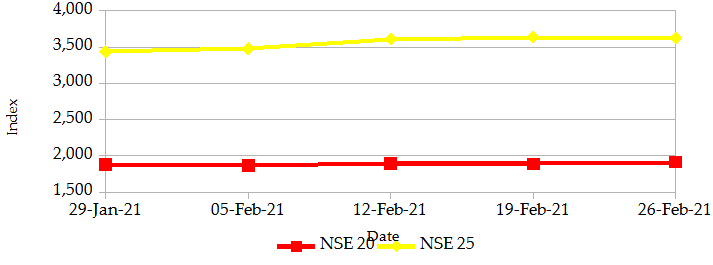

During the month of February, NASI, NSE 20 and NSE 25 increased by 6.3%, 1.8% and 5.5% respectively on a monthly basis. On a weekly basis, the NASI and NSE 25 decreased by 0.1% and 0.4% while NSE 20 increased by 1.4%. The increase in NASI is a result of gains of large-cap stocks such as BAT Kenya, East Africa Breweries Ltd, KCB Group and Safaricom Plc.. At the close of the month, market capitalization increased by 6.31% to Kshs 2.54 trillion. Also, total shares traded and equity turnover decreased by 55.3% and 42.6% respectively to 10 million shares and Kshs 353 million.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25TS

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -2.45% | 2.61% |

| STOXX Europe 600 | -2.58% | 2.31% |

| Shanghai Composite (SSEC) | -5.06% | 0.75% |

| MSCI Emerging Market Index | -6.35% | 0.73% |

| MSCI World Index | -2.83% | 2.45% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 0.21% | -1.42% |

| JSE All Share | -2.18% | 6.01% |

| NSE All Share (NGSE) | -0.95% | -6.16% |

| DSEI (Tanzania) | -0.52% | 3.01% |

| ALSIUG (Uganda) | -2.66% | 4.01% |

- During the month, major global markets gained on hopes the rollout of vaccines will reinvigorate the global economy. In the USA, the S&P 500 and Dow Jones indices gained by 2.61% and 3.17% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and UK’s FTSE 100 gained by 2.31% and 1.19% respectively.

- On a regional front, most markets had mixed returns. The FTSE ASEA Pan African index, representing the overall African markets, declined by 1.42% from the month of January. South Africa’s JSE All Share increased by 6.01%, Uganda’s All Share Index gained by 4.01% and Tanzania’s DSEI increased by 3.01%. However, Nigeria’s All-share index declined by 6.16%.

- On the global commodities markets, the crude prices gained supported by a sharp drop in US crude output due to the storms in Texas and an assurance that U.S. interest rates will stay low for a while. Extra voluntary cuts by Saudi Arabia have tightened global supplies and supported prices. The Crude Oil WTI futures increased by 17.82% from the previous month of January. Also, the ICE Brent Crude Oil increased in value by 18.34%.

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 64 contracts having a turnover of Kshs 9.60 million which was a decrease from 83 contracts having a turnover of Kshs 11.89 million recorded over the last month.

- The I-REIT market over the month recorded 142 contracts having a turnover of Kshs 3.01 million which was an increase from 211 contracts having a turnover of Kshs 1.84 million recorded over the last month.

- The ETF market recorded 1 deal having a turnover of Kshs 54.17 million from the previous month which registered no activity.

Get future reports

Please provide your details below to get future reports: