MONTH’S HIGHLIGHTS

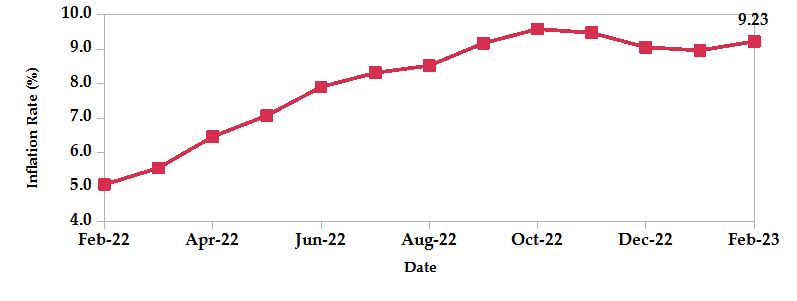

- Inflation edged higher to 9.2% in February from 9.0% in January, reversing the three-month downward trend. This was attributed to higher food prices evidenced by the food and non-alcoholic beverages inflation which rose from 12.8% to 13.3%, as production took a hit from the prolonged drought. The transport index remained unchanged, seeing as the prices of diesel and petrol were kept the same. The housing, water, electricity, gas and other fuels category increased by 0.4% mainly due to the 4.7% rise in prices of gas/LPG.

- The Cabinet gave approval for the legislative proposal to replace the nominal debt ceiling currently at Kshs 10 trillion with a debt anchor set at 55% of GDP in present value terms. The move comes after a previous attempt to peg debt to a percentage measure was met with an increment from Kshs 9 trillion. The Cabinet stated that this is in tandem with global best practices and the Administration’s efforts towards sustainable debt management.

- S&P Global revised Kenya’s outlook from Stable to Negative while affirming the ‘B/B’ long and short-term foreign and local currency sovereign credit ratings. This, they attributed to the troubled Eurobond issuance situation resulting from financing challenges within the external debt market, as well as the country’s 2023 debt service obligations. In addition, the ongoing US dollar shortage and the Shilling depreciation have fanned the external debt flame. The negative outlook also reflects the country’s tightened liquidity following a recent subdued performance of the domestic debt issuances.

- The National Treasury gazetted the actual revenues and net expenditure as of 31st January 2023. Total revenue collected during the month amounted to Kshs 1.14 trillion, accounting for 53.28% of the original estimates of Kshs 2.14 trillion for the 2022/23 financial year. While this reflects the ongoing tax policies and revenue administration reforms by the taxman, the total revenue still falls short of the 91.33% prorated amount expected for the first seven months of the year.

- The Central Bank of Kenya announced the automation of the process of onboarding investors of government securities creating portfolio accounts. Starting March 2023, new CDS forms will be in effect, eliminating the need to physically present them at CBK. The initiative is set to increase accessibility and investor participation in these securities.

- CMA facilitated an engagement with NSE, the Association of Pension Trustees and Administrators of Kenya and the Sanduku Investment Initiative towards the creation of a Kenya National REIT (KNR). KNR is expected to be an accreditation body for REITs and service providers within the value chain as well as ensuring that the investment grade REITs are structured for immediate investor uptake. KNR is aligned with the Government’s Economic Transformation Agenda towards delivering affordable housing units and is expected to unlock access to capital through capital markets.

- Kenya held the first Business Forum event with the European Union, as part of the EU Global Gateway strategy, in partnership with the Kenya Private Sector Alliance (KEPSA) and the European Business Council (EBC). The Forum witnessed the launch of the ‘Investing in Young Businesses in Africa’ initiative, aimed at supporting early-stage sustainable and inclusive businesses. In addition, a five-year Business Environment and Export Enhancement Programme (BEEEP) was established to boost Kenyan agricultural exports by an average of 25% annually and raise earnings by 9 billion Euros. The European Investment Bank will also mobilise 1.8 million Euros towards supporting green agriculture projects.

- OPEC raised the world oil demand growth forecast for 2023 by 0.1 million barrels per day (mb/d) to 2.3 mb/d to accommodate China’s increasing energy consumption as it reopens. This comes at a time when Russia announced plans to voluntarily scale down production by 500,000 barrels per day starting March 2023, in response to price caps imposed by major economies. The cut is estimated at 5% of Russian oil output and is expected to contribute to the restoration of market relations. This is set to further tighten oil markets over the near future.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves declined by 2.07% to settle at USD 6.86 billion (3.92 months of import cover). This lies below CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

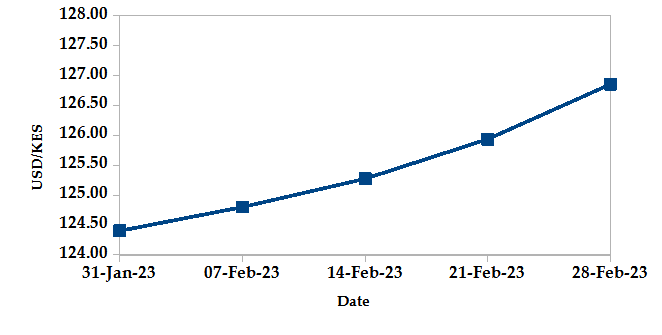

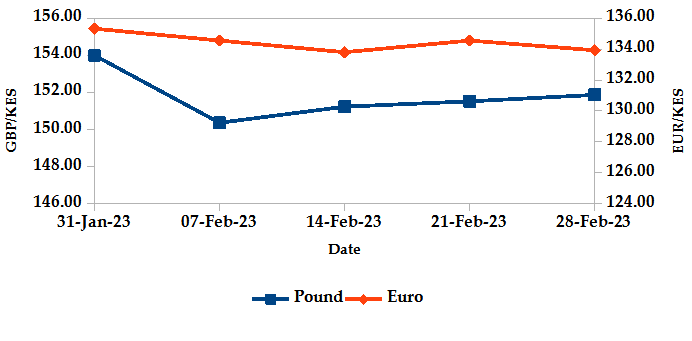

The Kenyan Shilling depreciated against the USD by 1.97%, exchanging at Kshs 126.85 at the end of the month, up from Kshs 124.40 in the previous month. The Shilling strengthened against the Sterling Pound by 1.38% and the Euro by 1.03%, exchanging at Kshs 151.87 and Kshs 133.93 at the end of the month, up from Kshs 154.00 and Kshs 135.33 respectively in the previous month. The depreciation is due to increased Dollar demand by importers as well as investors hedging their exposure by holding foreign currency deposits.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

The overall year-on-year inflation accelerated to 9.23% in February from a revised figure of 8.97% in January. This is largely due to higher food prices as a result of the prolonged drought.

INFLATION EVOLUTION

Liquidity

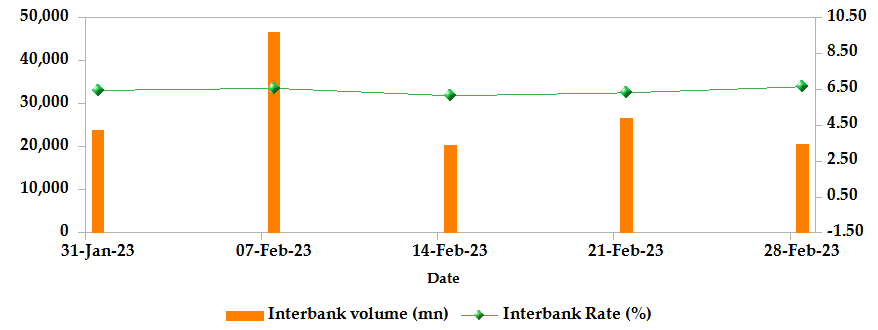

During the month, liquidity decreased as a result of tax remittances which offset government payments. The interbank rate rose to 6.64% from 6.44%. The volume of inter-bank transactions dropped from Kshs 23.78 billion to Kshs 20.58 billion. Commercial banks’ excess reserves peaked at Kshs 15.40 billion from Kshs 2.90 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

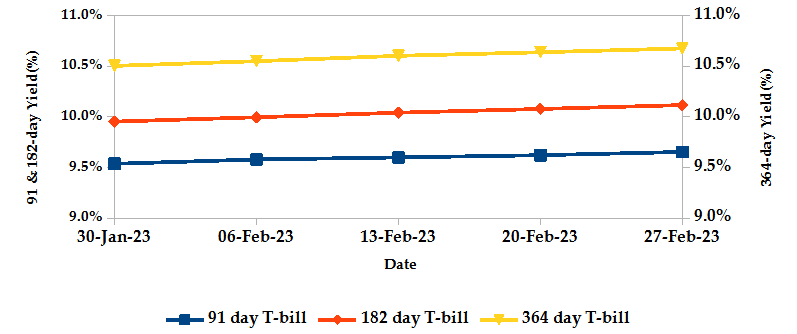

T-Bills

T-bills recorded an overall subscription rate of 167.06% for the month of February, compared to 126.55% recorded in the previous month. The rise in subscriptions was driven by intermittent periods of eased flow of funds during the month as well as improved yields on all issues. The performance of the 91-day, 182-day and 364-day papers stood at 583.70%, 105.27% and 62.19% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 1.23%, 1.64% and 1.64% to 9.66%, 10.12% and 10.68% respectively as investors pushed for higher returns to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

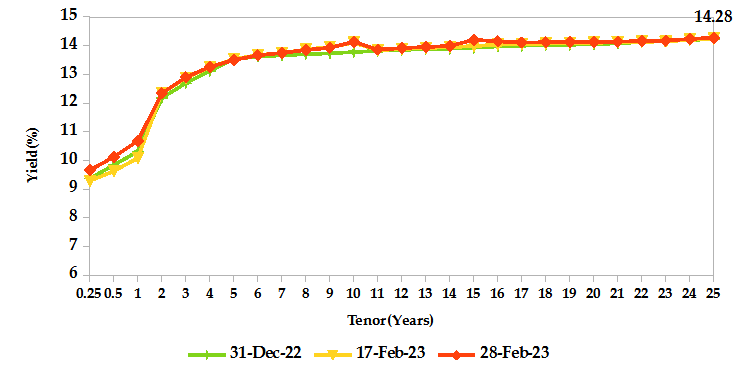

T-Bonds

During the month, T-Bonds registered a total turnover of Kshs 46.69 billion from 2,241 bond deals. This represents a monthly increase of 18.21% and 20.81% respectively. The yields on government securities in the secondary market increased during the month of February.

In the primary market, CBK issued a new 17-year amortized infrastructure bond; IFB1/2023/017 targeting Kshs 50.0 billion. Additionally, the Central Bank reopened FXD1/2017/010 and issued a new FXD1/2023/010 bond seeking Kshs 50.0 billion from both papers in the initial auction and Kshs 10.0 billion through a tap sale.

In the international market, yields on Kenya’s Eurobonds increased by an average of 42 basis points.

YIELD CURVE

EQUITIES

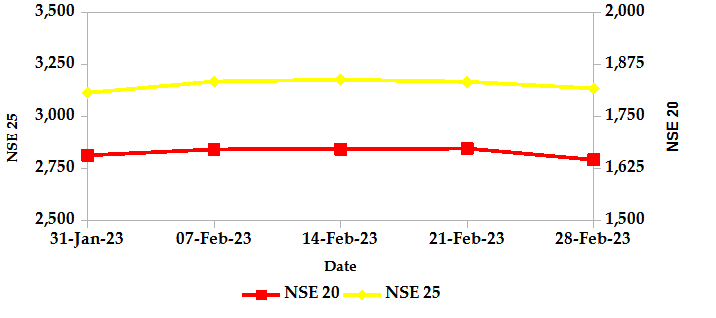

During the month, market capitalization gained 0.06% to settle at Kshs 1.96 trillion. Total shares traded declined by 49.63% to 161.46 million shares while equity turnover dropped 42.28% to close at Kshs 4.36 billion. On a monthly basis, NASI and NSE 25 settled 0.06% and 0.67% higher while NSE 20 lost 0.65%. The performance was a result of gains recorded by large-cap stocks such as Standard Chartered, Equity and NCBA of 3.97%, 3.41% and 2.23%. These were however weighed down by losses recorded by other large-cap stocks such as Stanbic, EABL and Safaricom of 4.55%, 0.85% and 0.43% respectively.

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market, over the month, recorded 50 contracts with a turnover of Kshs 3.50 million which was a decrease from 85 contracts with a turnover of Kshs 5.76 million recorded in the previous month.

- I-REIT market, over the month, recorded a turnover of Kshs 2.93 million with 289 deals which was an increase from Kshs 1.88 million with 154 deals recorded in the previous month.

- The ETF market, over the month, recorded a turnover of Kshs 0.23 million with 1 deal which was a decline from Kshs 12.20 million with 2 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -2.61% | 3.82% |

| STOXX Europe 600 | 1.74% | 6.20% |

| Shanghai Composite (SSEC) | 0.75% | 5.25% |

| MSCI Emerging Market Index | -6.54% | 0.15% |

| MSCI World Index | -2.53% | 4.37% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 2.12% | 0.48% |

| JSE All Share | -2.37% | 4.88% |

| NSE All Share (NGSE) | 4.82% | 8.16% |

| DSEI (Tanzania) | 0.96% | 1.85% |

| ALSIUG (Uganda) | -0.81% | -0.60% |

- During the month, global markets posted mixed performance. In the USA, the S&P 500 and Dow Jones indices edged 2.61% and 4.20% lower respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 were up by 1.74% and 1.35%, on the back of easing inflation and a resilient economy.

- On a regional front, markets also recorded mixed performance. The FTSE ASEA Pan African index, representing the overall African markets gained 2.12% from January. South Africa’s JSE All Share lost 2.37%, Nigeria’s All Share Index gained 4.82%, Tanzania’s DSEI picked up 0.96% while Uganda’s All Share index declined by 0.81%.

- On the global commodities markets, oil futures indices remained volatile reflecting China’s demand rebound, Russia’s plan to cut production and major economies’ efforts to curb inflation by raising interest rates. Crude Oil WTI futures and ICE Brent Crude Oil settled 3.13% and 2.74% lower to close at $76.67 and $83.12 respectively.

Get future reports

Please provide your details below to get future reports: