Month’s Highlights

The MPC met during the month and retained the CBR at 7.0% for the sixth time in a row since the rate cuts in the first half of 2020. The economic outlook still remains positive and inflation is well anchored. All other sectors have rebounded stable and resilient.

EPRA reviewed fuel prices upwards for the month of January, citing increased landing costs of imported fuel in December 2020 and an increase in crude oil prices globally. Petrol increased by Kshs 0.17 to retail at 106.99. Diesel and kerosene increased by Kshs 4.57 and Kshs 3.56 respectively.

IMF put pressure on Kenya to include 3.47 trillion on parastatal and county loans in the country’s national debt, raising the public debt to 10 trillion and crashing through the 9 trillion limit set by the parliament. This puts Kenya at risk of losing access to cheap Eurobonds. However, the current account deficit narrowed to 4.7% of GDP from 4.9% in the twelve months to November 2020, attributable to savings from oil imports and resilient earnings from exports and remittances.

IMF has increased its projections for the global economy with a GDP of 5.5% compared to its previous projection of 5.2%. The projection is driven by hopes of global recovery as vaccinations kick off and expectations of more stimulus in large economies. Emerging markets and developing countries are expected to grow by 6.3% in 2021, mainly led by India and China whose GDPs are expected to grow by 11.5% and 8.1% respectively.

KRA surpassed its target revenue collections by 2 billion to raise 166 billion in December 2020 – a 3.5% increase from December 2019. Customs and Border control recorded the highest growth of 40.9% to raise 60.8 billion. Improved revenue collections is attributed to improved economic conditions since the ease of COVID-19 containment measures as well as the agency’s efforts to increase tax compliance.

Assets in Kenya mutual funds grew by 37% year-on-year to 98 billion in the third quarter of 2020, compared to a similar period in 2019. Kenyans opted for mutual funds due to uncertainties in the economy. CIC Unit Trust, Britam Unit Trust and ICEA Unit Trust remained the top fund managers in terms of wealth with 40.5 billion, 11.3 billion and 10.6 billion respectively.

The Nairobi Securities Exchange announced that the bourse will continue experiencing recovery, following the recent upgrade by MSCI Emerging Markets to 9.49% from 8.2%. The upgrade was attributed to return of foreign investors, improved business environment, and attractive prices of many stocks.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 1.12% to stand at USD 7.66 billion(4.71 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

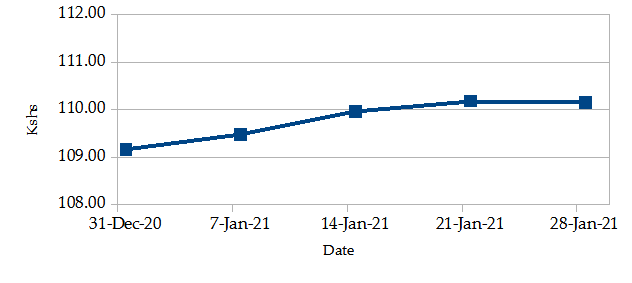

Currency

The Kenyan Shilling depreciated against the USD by 0.89% exchanging at Kshs 110.14 at the end of the month up from Kshs 109.17 in the previous month. The depreciation is due to high dollar demand from general importers as businesses resumed following the festive season. We expect continued pressure on the shilling due to reduced dollar inflows from the tourism and horticulture sectors.

USD Vs KSHS

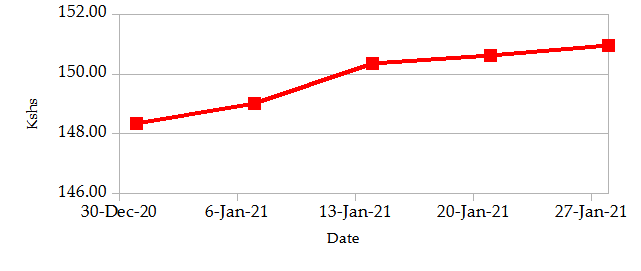

STERLING POUND Vs KSHS

Inflation

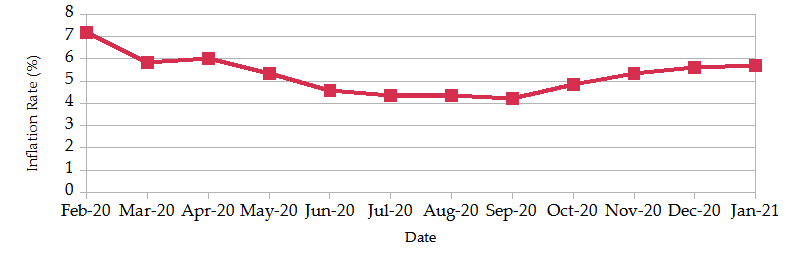

The overall year-on-year inflation increased to 5.69% in the month of January up from 5.63% in December. The increase is attributable to an increase in food and non-alcoholic index and the transport index by 1.26% and 1.07% respectively. This was due to the reintroduction of the 16% VAT and increased fuel prices by EPRA. The price of Kerosene rose by 4.66% from the previous month.

INFLATION EVOLUTION

Liquidity

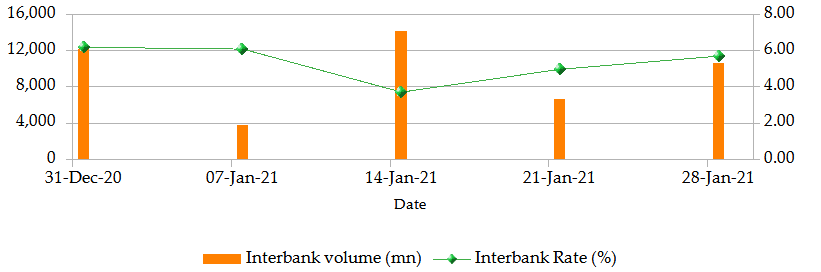

During the month of January, liquidity eased as a result of government payments which partly offset tax receipts. The inter-bank rate decreased to 5.79% from 6.19% the previous month. The volume of inter-bank transactions increased to Kshs 17.25 billion from Kshs 12.10 billion. Commercial banks excess reserves decreased to Kshs 13.7 billion from Kshs 16.8 billion the previous month.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

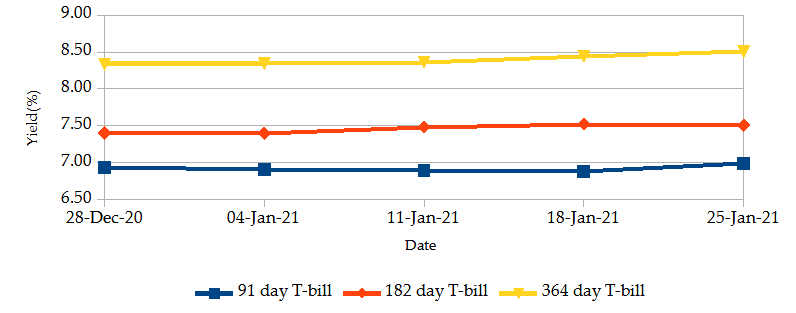

The T-bills recorded an overall subscription rate of 66.84% at the end of the month of January, compared to 52.60% recorded in the previous month. The increase in subscription is due to an increase in yields for the 182 and 364-day papers. The performance of the 91-day, 182-day and 364-day papers stand at 61.84%, 31.79% and 103.88% respectively. On a monthly basis, the yields on the 91-day papers decreased by 0.13% to 6.90% and yields on 182-day and 364-day papers increased by 2.41% and 3.29% respectively to 7.58% and 8.62%.

T-BILLS

T-Bonds

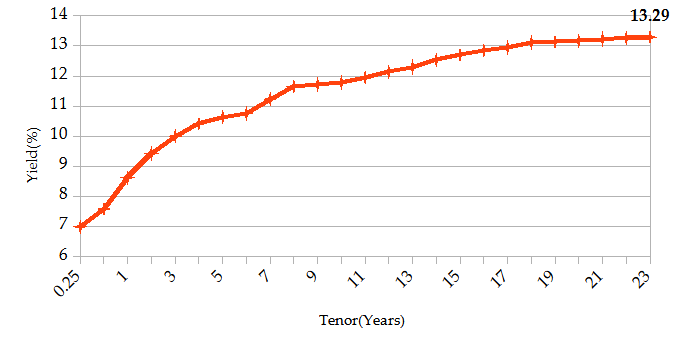

Over the month of January, the T-Bonds registered a total turnover of Kshs. 52.72 billion from 1,035 bond deals. This represents a monthly decrease of 6.61% and 31.50% respectively. The yields on government securities in the secondary market remained relatively stable during the month of January.

In the international market, yields on Kenya’s Eurobonds remained stable, increasing by an average of 1.02 basis points.

YIELD CURVE

EQUITIES

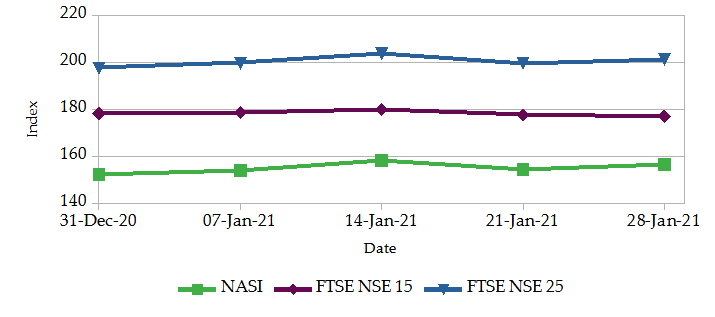

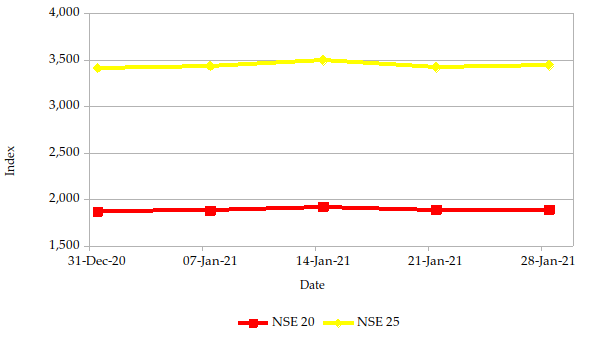

During the month of December, the market capitalization rose by 6.21% to Kshs 2.34 trillion. However, total shares traded and equity turnover declined by 75.10% and 84.68% respectively to 4 million shares and Kshs 86 million. NASI, NSE 20 and NSE 25 gained by 6.2%, 6.3% and 5.3% respectively on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 gained by 1.3%, 1.6% and 2.1% respectively. The gain in NASI is a result of an appreciation of large-cap stocks such as Safaricom, Co-operative Bank, East Africa Breweries Ltd and ABSA Bank.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25TS

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 83 contracts having a turnover of Kshs 11.89 million which was an increase from 93 contracts having a turnover of Kshs 7.87 million recorded over the last month.

- The I-REIT market over the month recorded 211 contracts having a turnover of Kshs 1.84 million which was a decrease from 195 contracts having a turnover of Kshs 2.17 million recorded over the last month.

- The ETF market recorded no activity over the month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | -3.31% | -1.11% |

| STOXX Europe 600 | -3.11% | -0.80% |

| Shanghai Composite (SSEC) | -3.43% | 0.29% |

| MSCI Emerging Market Index | -4.54% | 2.93% |

| MSCI World Index | -3.41% | -1.05% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 1.38% | 4.76% |

| JSE All Share | -2.67% | 5.39% |

| NSE All Share (NGSE) | 3.44% | 5.32% |

| DSEI (Tanzania) | -0.27% | -1.47% |

| ALSIUG (Uganda) | -0.65% | -0.76% |

- During the month, major global markets declined due to vulnerabilities arising from the new variant of Covid-19 and new lockdowns in major economies, especially in the UK. In the USA, the S&P 500 and Dow Jones indices declined by 1.11% and 2.04% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and UK’s FTSE 100 declined by 0.80% and 0.82% respectively.

- On a regional front, most markets had mixed returns. The FTSE ASEA Pan African index, representing the overall African markets, increased by 4.76% from the month of December. South Africa’s JSE All Share gained by 5.39%, Uganda’s All Share Index declined by 0.76%, and Tanzania’s DSEI decreased by 1.47%. However, Nigeria’s All-share index rose by 5.32%.

- On the global commodities markets, the oil prices increased due to broader market strength and optimism. Saudi Aramco predicts oil demand will be returning to pre-Covid levels later this year. The Crude Oil WTI futures increased by 7.58% from the previous month of December. Also, the ICE Brent Crude Oil increased in value by 7.88%. Gold futures declined by 2.7% as gold prices declined due to subdued demand under the threat of new variants of the Covid-19 virus which unsettled investors.

Get future reports

Please provide your details below to get future reports: