MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) met on 30th January 2023 and decided to maintain the Central Bank Rate (CBR) at 8.75%, noting that the impact of the previous rate adjustment was still working its way through the economy. In addition, measures taken by the Government to allow limited duty-free imports of certain food items were expected to relieve pressure on food prices and further ease inflation.

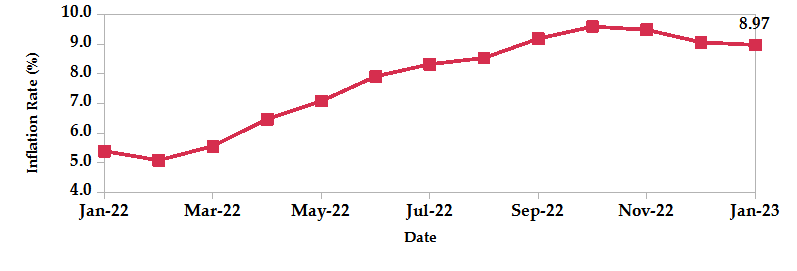

- Inflation declined further to 9.0% in January from 9.1% in December attributed to lower food prices amid improved supply following the short rains and lower global commodity prices. This was evidenced by the food and non-alcoholic beverages inflation which dropped from 13.8% to 12.8%. The transport index remained unchanged, tracking the constant prices of diesel and fuel. The housing, water, electricity, gas and other fuels category rose by 0.3% mainly due to an increase in the prices of electricity units.

- Kenya’s Balance of Payment data indicated that the current account deficit was estimated at 4.9% of GDP in 2022, from 5.2% in 2021. The contraction reflects the strong performance of export goods and services and resilience in remittance inflows.

- The National Treasury released the 2023 Draft Budget Policy Statement which projected an increase in revenue collected in the 2023/24 financial year to Kshs 2.9 trillion, scaled up from Kshs 2.5 trillion in FY2022/23. This will be supported by ongoing reforms in tax policy and revenue administration measures aimed at expanding the tax base. These measures, among others, include the integration of KRA tax system with the telecommunication companies, the reduction of Value Added Tax (VAT) gap from 38.9% to 19.8% by fully rolling out the electronic Tax Invoice Management System (eTIMS), reduction of Corporate Income Tax (CIT) gap from 32.2% to 30.0% and expansion of tax base in the informal sector.

- KPLC has submitted a proposal to EPRA for electricity tariff adjustment to ensure competitive prices, efficiency and sustainability in the provision of electricity generation, transmission, distribution and retail supply services to sub-sectors. An additional proposal includes revising the consumption band for small commercial and domestic customers from the current 100kWh/month to 30kWh/month to align the objectives of the social tariff customer category with the correct social class normally defined by income level. With these adjustments, the revenue unlocked is expected to flow into meeting obligations for power generation plants for KenGen and Independent Power Producers as well as expand the electricity network owned by Kenya Power, KETRACO and Rural Electrification Schemes.

- Nairobi City County Government (NCCG) began talks with CMA on the possibility of actualizing one of the Authority’s visions that 30% of counties financing be raised from capital markets. CMA pledged support for NCCG’s plan to issue a green bond and the potential listing of County agencies such as Nairobi Water and Sewerage Company to acquire long-term financing to meet development needs.

- IMF projected that global inflation is set to fall to 6.6% in 2023 from 8.8% in 2022 and drop further to 4.3% in 2024, still above pre-pandemic levels of 3.5%. The headline figure reflects declining international fuel and non-fuel commodity prices due to weaker global demand as well as the cooling effects of monetary policy restrictions.

- World Bank revised 2023 global growth down to 1.7% from 3% reported in June 2022 and 2.7% in 2024. This follows a slowdown in projected growth in advanced economies from 2.5% in 2022 to 0.5% in 2023, while growth in emerging markets and developing economies is expected at 2.7% in 2023 from 3.8% in 2022. Emerging markets growth has been driven down by heavy debt burdens and weak business investments, piling on existing ailing education, healthcare, poverty and infrastructure.

- The Federal Reserve raised the target range for Fed funds rate by 25 bps to 4.5% – 4.75%, in line with market expectations. The Chair reiterated that interest rates are not yet at a sufficiently restrictive level despite disinflation, noting that it is still at an early stage. The European Central Bank and Bank of England took the 50bps route, pledging to stay the course in raising rates.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves declined by 5.83% to settle at USD 7.01 billion (3.92 months of import cover). This lies below CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

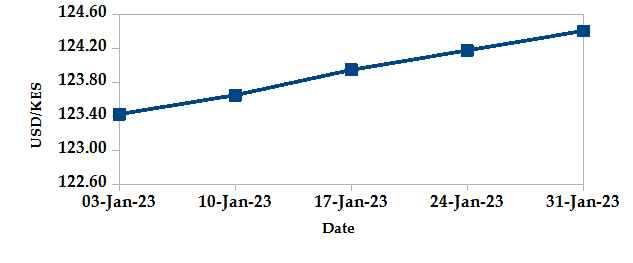

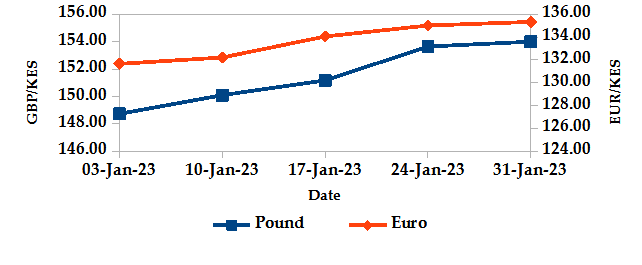

The Kenyan Shilling depreciated against the USD by 0.83%, exchanging at Kshs 124.40 at the end of the month, up from Kshs 123.37 in the previous month. The Shilling also depreciated against the Sterling Pound by 3.72% and the Euro by 3.10%, exchanging at Kshs 154.00 and Kshs 135.33 at the end of the month up from Kshs 148.47 and Kshs 131.27 respectively in the previous month. The depreciation is due to increased Dollar demand by importers as well as investors hedging their exposure by holding foreign currency deposits.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

The overall year-on-year inflation slowed to 8.97% in January from a revised figure of 9.06% in December This is mainly attributed to lower food prices as supply improved and easing global commodity prices.

INFLATION EVOLUTION

Liquidity

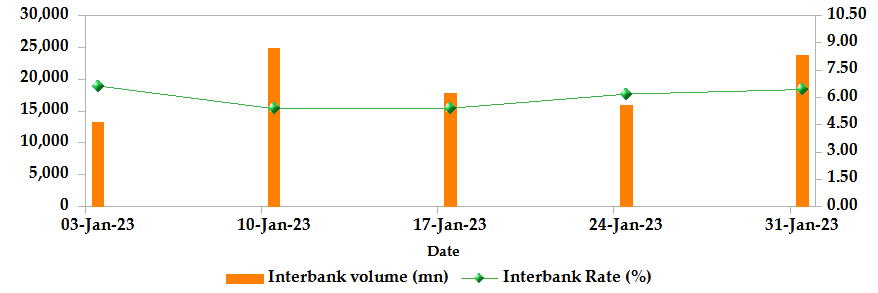

During the month, liquidity slightly increased as a result of government payments which offset tax remittances. The interbank rate declined to 6.44% from 6.49%. The volume of inter-bank transactions dropped from Kshs 25.49 billion to Kshs 23.78 billion. Commercial banks’ excess reserves declined from Kshs 10.60 billion to Kshs 2.90 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

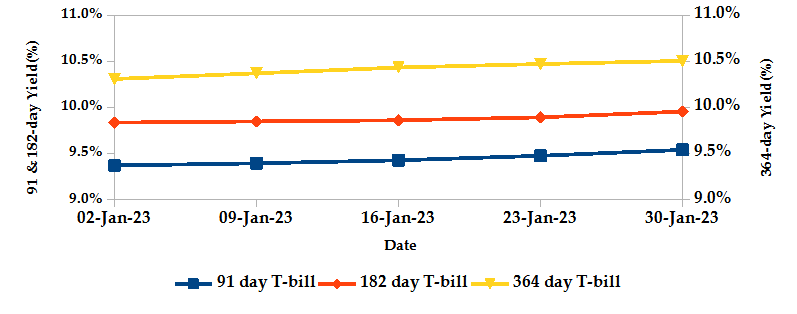

T-bills recorded an overall subscription rate of 126.55% for the month of January, compared to 77.81% recorded in the previous month. The rise in subscriptions was driven by a slight uptick in market liquidity as well as improved yields on all issues during the month. The performance of the 91-day, 182-day and 364-day papers stood at 422.13%, 92.32% and 42.54% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 1.80%, 1.22% and 1.90% to 9.54%, 9.95% and 10.50% respectively as investors pushed for higher returns to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

T-Bonds

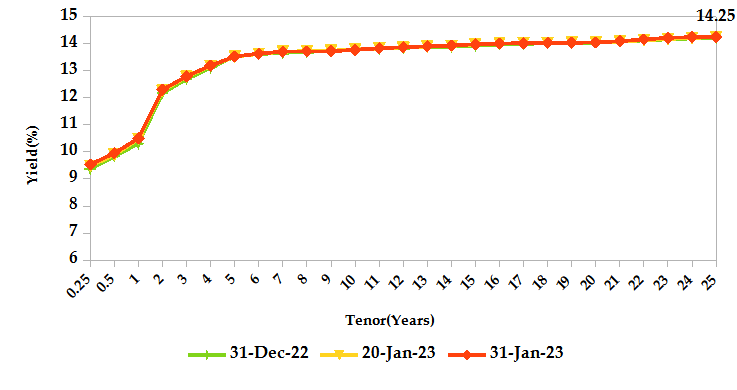

During the month, T-Bonds registered a total turnover of Kshs 39.50 billion from 1,855 bond deals. This represents a monthly decline of 4.22% and 4.13% respectively. The yields on government securities in the secondary market slightly increased during the month of January.

In the primary market, CBK reopened FXD1/2020/005 and FXD1/2022/015 through a tap sale seeking to raise Kshs 10.00 billion. Additionally, the Central Bank reopened FXD1/2017/010 with an effective tenor of 4.5 years and a coupon of 12.97% and issued a new FXD1/2023/010 bond seeking Kshs 50.0 billion from both papers.

In the international market, yields on Kenya’s Eurobonds dropped by an average of 54 basis points.

YIELD CURVE

EQUITIES

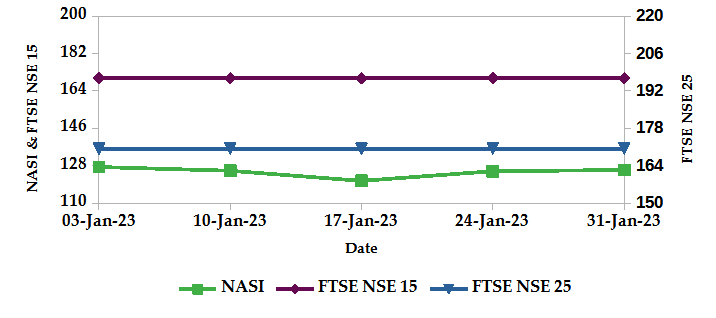

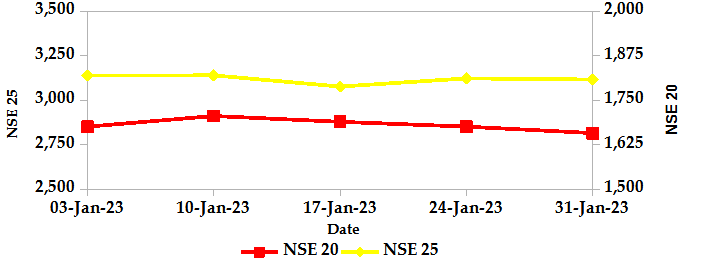

During the month, market capitalization dropped 1.23% to settle at Kshs 1.96 trillion. Total shares traded rose by 117.05% to 320.53 million shares while equity turnover picked up 86.49% to close at Kshs 7.56 billion. On a monthly basis, NASI, NSE 20 and NSE 25 settled 1.22%, 1.12% and 0.59% lower respectively. The performance was a result of losses recorded by large-cap stocks such as Safaricom and Equity of 3.11% and 1.12%. These were however bolstered by gains recorded by other large-cap stocks such as Standard Chartered, EABL and Co-operative of 10.16%, 5.22% and 1.22% respectively.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market, over the month, recorded 85 contracts with a turnover of Kshs 5.76 million which was a decrease from 61 contracts with a turnover of Kshs 8.90 million recorded in the previous month.

- I-REIT market, over the month, recorded a turnover of Kshs 1.88 million with 154 deals which was a decrease from Kshs 5.79 million with 188 deals recorded in the previous month.

- The ETF market, over the month, recorded a turnover of Kshs 12.20 million with 2 deals which was a decline from Kshs 251.14 million with 1 deal recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 1.48% | 6.18% |

| STOXX Europe 600 | -0.04% | 6.67% |

| Shanghai Composite (SSEC) | -0.28% | 5.39% |

| MSCI Emerging Market Index | -0.74% | 7.85% |

| MSCI World Index | 1.05% | 7.00% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 0.19% | -1.16% |

| JSE All Share | -0.70% | 9.67% |

| NSE All Share (NGSE) | 1.19% | 3.88% |

| DSEI (Tanzania) | 1.41% | 1.28% |

| ALSIUG (Uganda) | 0.62% | 0.43% |

- During the month, global markets posted gains as major economies realized softer inflation numbers and the gradual economic rebound in China. In the USA, the S&P 500 and Dow Jones indices picked up 6.18% and 2.83% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 were also up by 6.67% and 4.29%, supported by Britain’s improved economic outlook.

- On a regional front, markets recorded mixed performance. The FTSE ASEA Pan African index, representing the overall African markets declined by 1.16% from December. South Africa’s JSE All Share increased by 9.67%, Nigeria’s All Share Index gained 3.88%, Tanzania’s DSEI picked up 1.28% while Uganda’s All Share index increased by 0.43%.

- On the global commodities markets, oil futures indices were volatile, partly reflecting rising optimism about China’s reopening and demand rebound. Crude Oil WTI futures and ICE Brent Crude Oil settled 1.64% and 0.52% lower to close at $79.15 and $85.46 respectively.

Get future reports

Please provide your details below to get future reports: