MONTH’S HIGHLIGHTS

- The Central Bank of Kenya (CBK’s) Monetary Policy Committee (MPC) retained the Central Bank Rate at 7.5% during its 27th July meeting. The MPC noted that international commodity prices, particularly oil, wheat and edible oils, had begun to moderate and hence this may likely ease inflationary pressure. The government subsidy program is likely to tame further increases in commodity prices.

- The Energy and Petroleum Regulatory Authority (EPRA) retained the pump prices for fuel products at Ksh. 159.12, Ksh. 140 and Ksh. 127.94 for super, diesel and kerosene respectively. This follows after the government authorized an additional Ksh. 16.68 billion in the fuel subsidy kitty cushioning the prices from inflating further. The landing cost of imported super increased by 19.04% to $1,042.85 from last month while that of diesel rose 2.2% to $1,019. The shilling devaluation against the Dollar to Ksh 118.8 per dollar has since increased the cost of imports.

- Capital Markets Authority (CMA) released the Q2’2022 statistical bulletin and during the quarter. Unit Trust Assets Under Management grew by 4.45% to Ksh 140.7 billion as at the end of Q2’2022 from Ksh 134.7 billion recorded in FY’2021. Equity turnover for Q2 stood at Ksh 26.24 billion, a 30.94 % decrease compared to Ksh 37.99 billion registered in Q2’2021.

- The National Treasury gazetted the revenue expenditures for the FY’2021/2022 highlighting that the total revenue collected ending June 2022 amounted to Ksh 1,939.2 billion equivalent to 104.7% of the revised estimates of kshs 1,851.5 billion.

- The Kenya Revenue Authority (KRA) recorded a revenue collection of KShs. 2.031 trillion for the Financial Year 2021/2022 compared to KShs. 1.669 trillion collected in the last financial year exceeding its revised target of Kshs. 1.976 trillion. The revenue collection signifies a performance rate of 102.8% against the revised target and a revenue growth of 21.7% compared to the last financial year. The significant growth is attributed to improved tax collection and compliance.

- The government authorized subsidies for maize flour and oil prices in an attempt to curb the high cost of living for Kenyans. An additional Ksh 16.68 billion was added to the fuel subsidy kitty cushioning the prices from inflating further. Additionally, the government subsidized the price of maize flour on a four-week program to sh 100 for a two-kilogram packet down from sh 210. This comes as the price of commodities under food and non-alcoholic beverages register a 15.3% twelve-month increase.

- In global markets, various central banks have continued making adjustments to their monetary policies in an attempt to curb further currency devaluation and rising inflation rates. Uganda’s Central Bank raised its benchmark rates to 8.5% and The Central Bank of Sri Lanka raised its rate to 15.5%. South Africa’s Reserve Bank raised its rate by 5.5%, The Central Bank of Nigeria up to 14% and The Bank of Canada raised its policy rate to 2.5%. However, Ghana’s central bank retained the rate at 19% on signs of a levelling inflation curve.

- Supply chain disruptions in the global markets have continued sending ripples as commodity scarcity keeps the prices on an upward trend. Inflation in the UK hit 9.4% while Ghana’s inflation increased to 38%. The United States and Turkey registered increases to 9.1% and 78.6% while Egypt and Ethiopia recorded a decline to 13.2% and 34% respectively. Negotiations are underway for a treaty to allow commodity export from both Russia and Ukraine amid the ongoing strife.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 2.38% to stand at USD 7.74 billion(4.46 months of import cover). However, this meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover, and the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

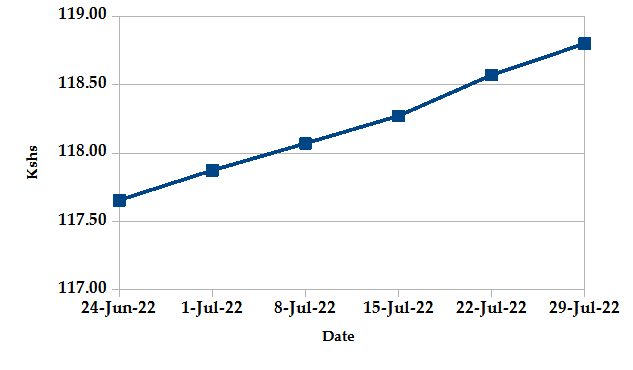

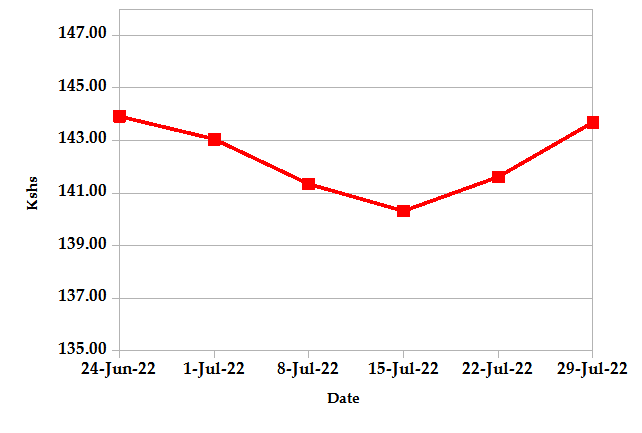

The Kenyan Shilling depreciated against the USD by 0.94%, exchanging at Kshs 118.80 up from Ksh 117.83 in the previous month. The depreciation is due to election-related uncertainty due to the closeness of presidential polls which decreases investor confidence. Despite this, the Kenya Shilling has strengthened against other major international currencies including the Sterling pound and the Euro.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

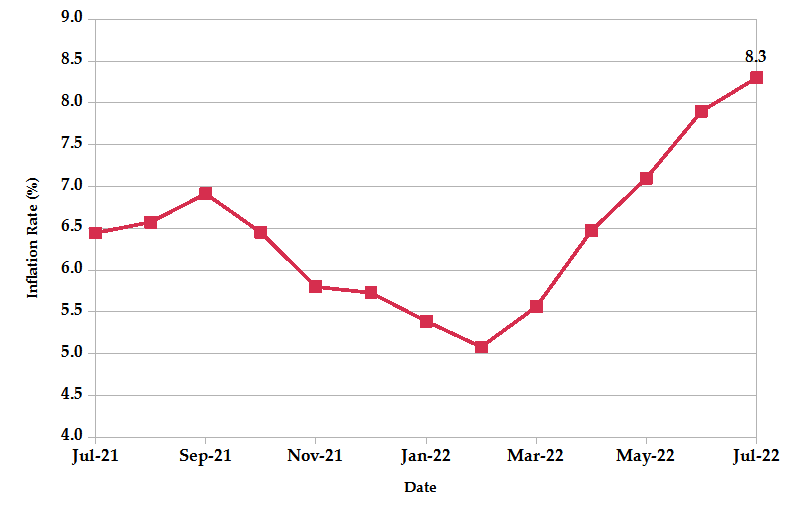

The overall year-on-year inflation increased to 8.3% in the month of June up from a revised figure of 7.9% in May. The increase is attributable to the increase in prices of commodities under; food and non-alcoholic beverages (15.3%), transport (7.0%) and housing, water, electricity, gas and other fuels (5.6%) between July 2021 and July 2022.

INFLATION EVOLUTION

Liquidity

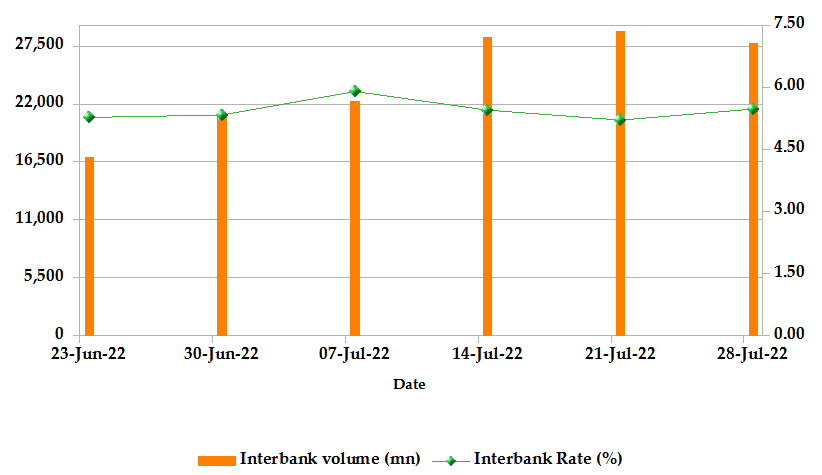

During the month, liquidity tightened as a result of government receipts from the issue of the two reopened fifteen-year infrastructure bonds which mopped up liquidity. The inter-bank rate increased to 5.36% up from 5.21%. The volume of inter-bank transactions increased from Kshs 14.34 billion to Kshs 19.25 billion. Commercial banks’ excess reserves decreased from Kshs 3.1.2 billion to Kshs 27.2 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

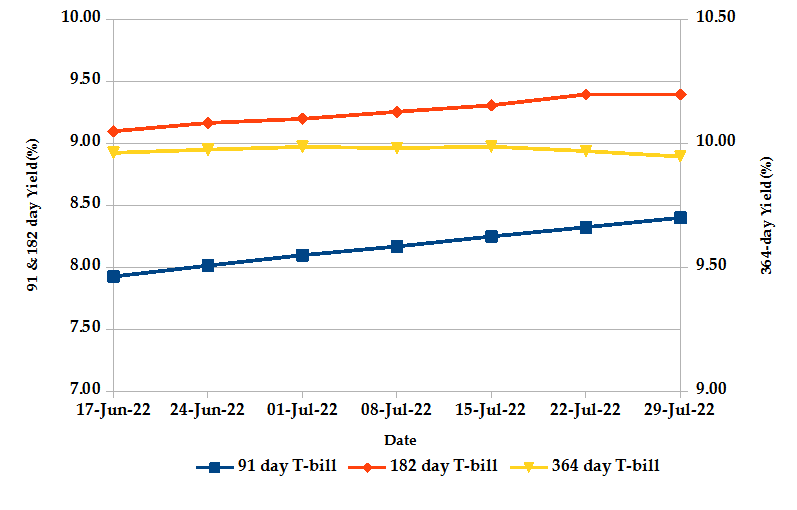

T-Bills

The T-bills recorded an average subscription rate of 108.6% for the month of July, compared to 70.76% recorded in the previous month. The general oversubscription is partly attributed to eased liquidity in the money market and relatively higher yields. The monthly average of the 91-day and 182-day T-bills increased by 199% and 28.16% to close at 336.5% and 78.6% respectively while that for the 364-day T-bill declined by 16.93% down to 47.5% compared to the previous month. Acceptance rate increased by 10.52% to 94.57% outlining increased government appetite for funds.

T-BILLS

T-Bonds

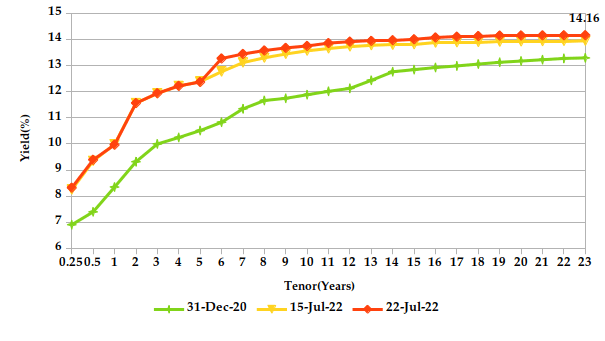

Over the month of July, the T-Bonds registered a turnover of Kshs 23.86 billion from 597 bond deals. This represents a monthly increase of 27.39% in turnover and a 10.63% decrease in bond deals. The yields on government securities in the secondary market increased during the month of July.

In the international market, yields on Kenya’s Eurobonds rose by an average of 48.5 basis points over the month on month and 8.96% year to date.

YIELD CURVE

EQUITIES

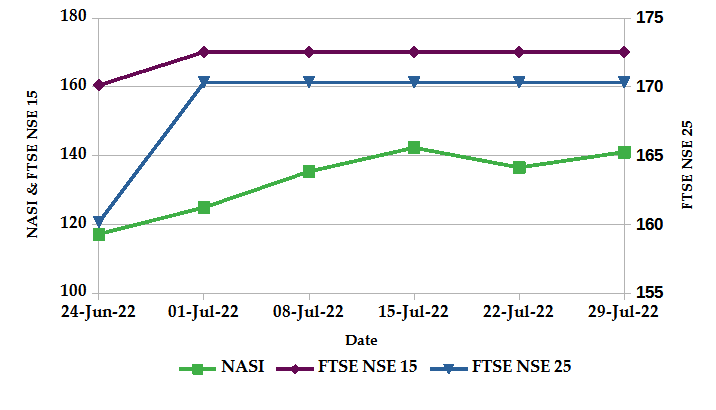

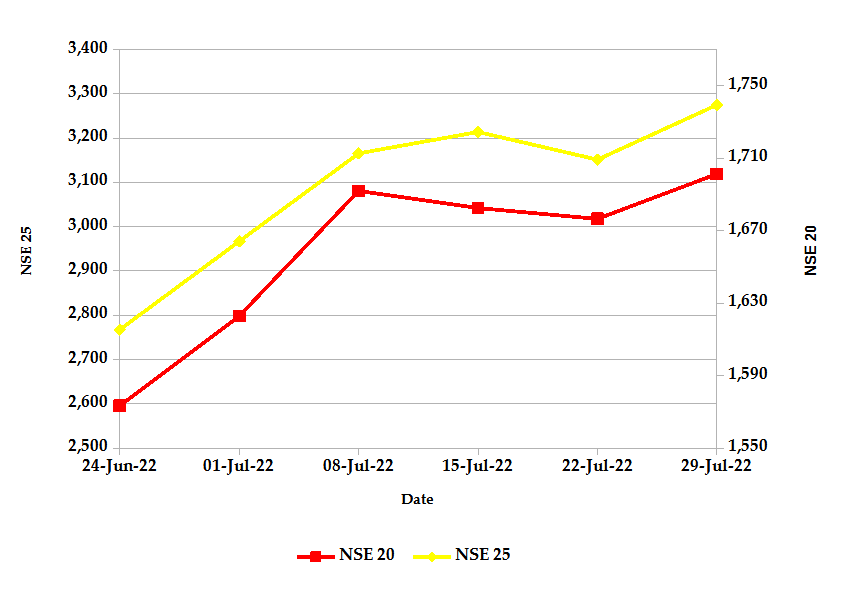

During the month of June, the market capitalization increased by 7.9% to Kshs 2.746 trillion. Total shares traded and equity turnover plunged by 32.76% and 41.07% respectively to 49 million shares and Kshs 1.3 billion. NASI, NSE 20 and NSE 25 increased by 13.3%, 5.5% and 10.9% respectively on a monthly basis. On a weekly basis, the NASI, NSE 20 and NSE 25 gained by 3.3%, 1.5% and 3.9% respectively. The increase in NASI is a result of gains of large-cap stocks such as Safaricom, EABL, Equity and COOP by 20.04%, 13.11%, 11.63% and 9.17% on a monthly basis.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 128 contracts having a turnover of Kshs 5.37 million which was a decrease from 266 contracts having a turnover of Kshs 17.89 million recorded over the last month.

- I-REIT market over the month recorded a turnover of Kshs 1.4 million with 176 deals which was a decrease from Kshs 1.5 million with 166 deals recorded over the last month.

- The ETF market over the month recorded no activity.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 4.26% | 9.11% |

| STOXX Europe 600 | 2.96% | 7.64% |

| Shanghai Composite (SSEC) | -0.51% | -4.28% |

| MSCI Emerging Market Index | 0.34% | -0.69% |

| MSCI World Index | -3.60% | 7.86% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -0.70% | -4.05% |

| JSE All Share | 1.14% | 3.93% |

| NSE All Share (NGSE) | -3.10% | -2.79% |

| DSEI (Tanzania) | 1.64% | 1.40% |

| ALSIUG (Uganda) | 4.25% | 12.91% |

- During the month, major global markets increased as investor sentiments improved due to positive indications from economic data. In the US, a stronger monthly jobs report reaffirmed bets for the Federal Reserve to front-load rate hikes to slow inflation.. In the USA, the S&P 500 and Dow Jones indices gained by 9.11% and 6.71% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 declined by 7.64% and 3.54% respectively.

- On a regional front, the markets closed the month mixed amid sharp interest rate hikes by major central banks pushing investors to ramp up bets of a global economic recession. This comes on the back of rising inflation and currency devaluation against the Dollar in most emerging markets. The FTSE ASEA Pan African index, representing the overall African markets, declined by 4.05% from the month of May. South Africa’s JSE All Share increased by 3.93%, Nigeria’s All Share Index declined by 2.79%, Tanzania’s DSEI declined by 1.40% and Uganda’s All Share Index increased by 12.91%.

- On the global commodities markets, the oil futures indices declined over concerns of a global slowdown. The Crude Oil WTI futures plunged by 7.05% from the previous month of May. The ICE Brent Crude Oil decreased in value by 4.61%.

Get future reports

Please provide your details below to get future reports: