MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC) convened on 29th March 2023 and decided to raise the Central Bank Rate (CBR) from 8.75% to 9.50% in response to the need for further tightening to anchor inflation expectations and the potential impact of elevated global risks on the domestic economy.

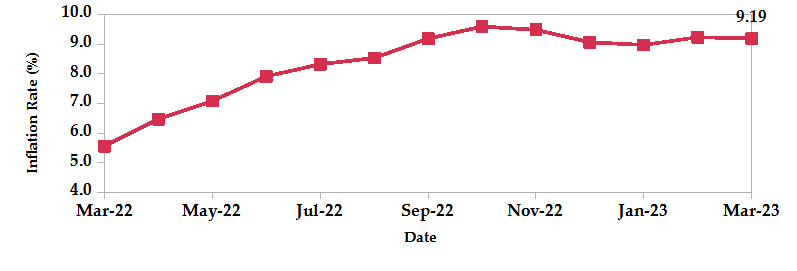

- Inflation slightly declined in March 2023, mainly driven by the marginal decline in fuel inflation from 13.8% in February to 13.4%. Food inflation remained elevated at 13.4% from 13.3% in February, driven by higher prices of fresh produce following the recent drier-than-expected weather conditions in the country. The housing, water, electricity, gas and other fuels category rose 0.6% due to the increased price of electricity and LPG. The transport index edged 0.3% higher, credited to a rise in petrol prices during the month.

- The Energy & Petroleum Regulatory Authority (EPRA) approved new electricity tariffs for the 2022/23-2023/26 4th Tariff Control Period effective from 1st April 2023. The new tariffs will increase the revenue requirement to meet energy purchase costs, allow for system expansion, ensure financial sustainability and improve service delivery. While Commercial and Industrial customers will benefit from reduced end-user bills, Domestic and Small Commercial customers will face an increase, except for those in the Domestic Lifeline and Small Commercial 1 categories who consume between 0-30 kWh.

- Kenya’s balance of payment and current account deficit for the 12 months ending January 2023, as per the provisional data, indicates an improvement in the current account deficit from 5.6% in a similar period in 2022 to 4.9% of GDP. The narrower deficit is indicative of sluggish growth of imports, boosted by strong exports of goods and services as well as resilient remittance inflows.

- Kenya’s Cabinet approved the Privatization Bill 2023 to encourage private sector participation, improve infrastructure and public service delivery, reduce government spending and generate revenue through compensation for privatizations. The bill seeks to improve regulation, broaden ownership of state-owned entities and enhance efficiency and responsiveness to stakeholders. The bill is part of a wider reform process targeting public enterprises and aims to revitalize Kenya’s capital markets by reviewing the framework for state divestiture in non-strategic sectors.

- The Central Bank of Kenya (CBK) issued the Kenya Foreign Exchange Code (FX Code) to commercial banks. The FX Code establishes standards for commercial banks to promote the integrity and effective functioning of the wholesale FX market in Kenya, reinforcing the country’s flexible exchange rate regime. Market participants will be required to submit quarterly reports to CBK on the level of compliance with the FX Code within 14 days after the end of the period.

- The US Federal Reserve, Bank of England and the European Central Bank (ECB) took action to combat rising inflation by increasing interest rates by 0.25%, 0.25% and 0.5% respectively in March 2023. Inflation remains elevated in all three regions and policymakers are monitoring the credit conditions’ impact on economic activity and inflation outlook. The UK banking system is considered robust, while the ECB warns of persistently high inflation in the region. The US Federal Reserve, on the other hand, is prioritizing maximum employment and long-term inflation targets.

- The US and UK experienced positive GDP growth rates in Q4 2022. The US economy expanded by 2.6%, driven by private inventories, fixed investments and intellectual property products. However, consumer spending on goods declined and spending on services advanced much less than initially estimated. The overall 2022 GDP expanded by 2.1%. The UK economy expanded by a slight 0.1%, driven by higher household consumption, investment spending and higher government consumption. However, there was a decline in the volume of net trade and businesses de-stocked their inventories, partially offsetting the growth. On a yearly basis, the UK’s economic growth slowed sharply to 0.6% in Q4 2022, the weakest pace of expansion since a contraction of 7.7% in Q1 2021.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves declined by 6.33% to settle at USD 6.43 billion (3.59 months of import cover). This lies below CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

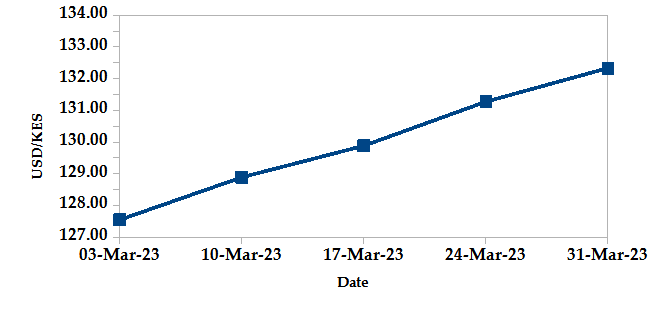

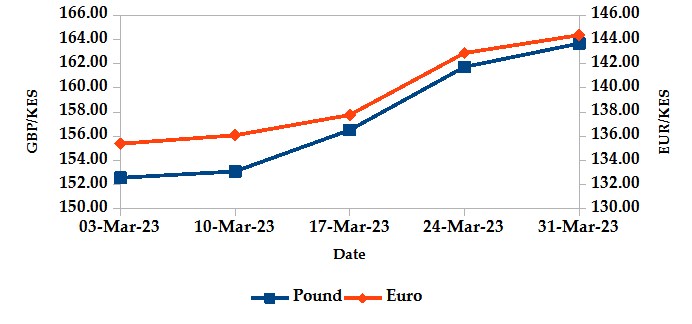

The Kenyan Shilling depreciated against the USD by 4.32%, exchanging at Kshs 132.33 at the end of the month, up from Kshs 126.85 in the previous month. The Shilling also depreciated against the Sterling Pound by 7.77% and the Euro by 7.79%, exchanging at Kshs 163.67 and Kshs 144.37 at the end of the month, up from Kshs 151.87 and Kshs 133.93 respectively in the previous month. The depreciation is due to increased Dollar demand by importers as well as investors hedging their exposure by holding foreign currency deposits.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

The overall year-on-year inflation slightly declined to 9.19% in March from a revised figure of 9.23% in February. This is mainly attributed to a marginal decline in fuel inflation.

INFLATION EVOLUTION

Liquidity

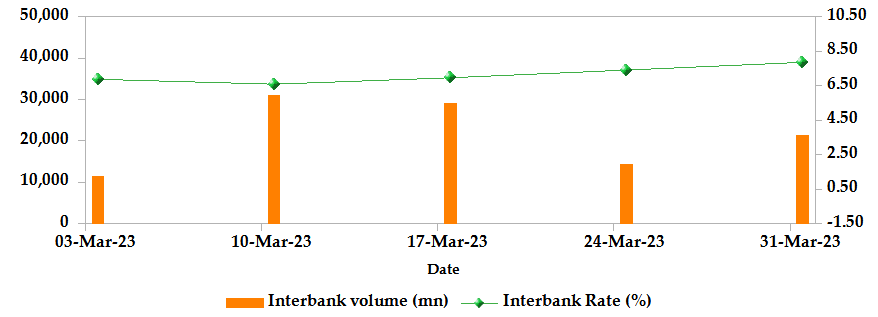

During the month, liquidity tightened as a result of tax remittances which offset government payments. The interbank rate rose to 7.86% from 6.64%. The volume of inter-bank transactions slightly increased to Kshs 21.35 billion from Kshs 20.58 billion. Commercial banks excess reserves decreased from Kshs 15.40 billion to Kshs 8.90 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

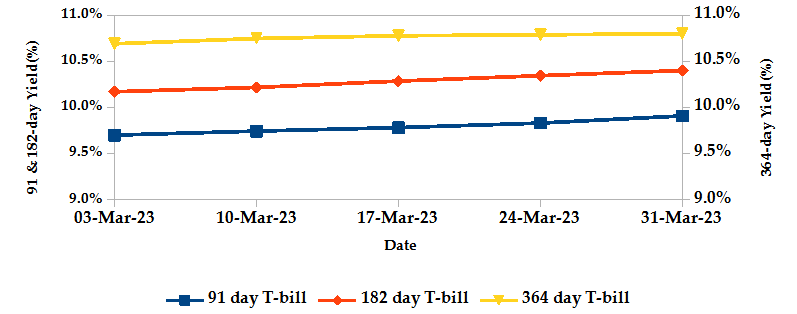

T-bills recorded an overall subscription rate of 97.99% during the month of March, compared to 167.06% recorded in the previous month. The decline in subscriptions was driven by tightened market liquidity. The performance of the 91-day, 182-day and 364-day papers stood at 298.22%, 77.26% and 38.62% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 2.61%, 2.79% and 1.16% to 9.91%, 10.40% and 10.80% respectively as investors pushed for higher returns to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

T-Bonds

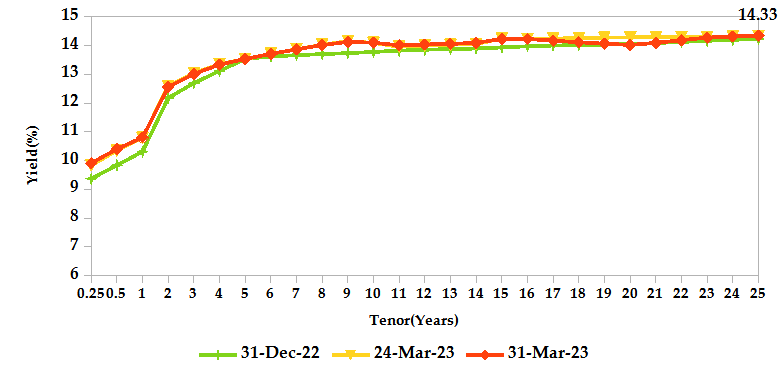

During the month, T-Bonds registered a total turnover of Kshs 74.96 billion from 3,806 bond deals. This represents a monthly increase of 60.55% and 69.83% respectively. The yields on government securities in the secondary market increased during the month of March.

In the primary market, CBK reopened the 17-year amortized infrastructure bond; IFB1/2023/017 through a tap sale seeking to raise 20.0 billion. Additionally, the Central Bank reopened three bonds. The first bond; FXD2/2018/10, seeks Kshs 20.0 billion and the other two bonds; FXD1/2022/03 & FXD1/2019/15 seek Kshs 30.0 billion.

In the international market, yields on Kenya’s Eurobonds increased by an average of 139 basis points.

YIELD CURVE

EQUITIES

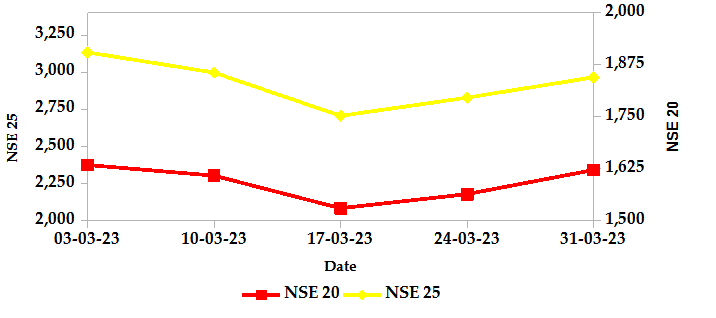

During the month, market capitalization lost 10.52% to settle at Kshs 1.76 trillion. Total shares traded rose by 273.48% to 603.02 million shares while equity turnover picked up 652.66% to close at Kshs 32.85 billion. On a monthly basis, NASI, NSE 20 and NSE 25 settled 10.49%, 1.49% and 5.43% lower. The performance was a result of losses recorded by large-cap stocks such as Safaricom, KCB and EABL of 22.32%, 7.19% and 2.72%. These were however bolstered by gains recorded by other large-cap stocks such as Stanbic, Standard Chartered, Co-operative and ABSA of 4.76%, 3.98%, 3.95% and 2.40% respectively.

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market, over the month, recorded 90 contracts with a turnover of Kshs 11.36 million which was an increase from 50 contracts with a turnover of Kshs 3.50 million recorded in the previous month.

- I-REIT market, over the month, recorded a turnover of Kshs 7.15 million with 247 deals which was an increase from Kshs 2.93 million with 289 deals recorded in the previous month.

- The ETF market, over the month, recorded a turnover of Kshs 0.00 million with 0 deals which was a decline from Kshs 0.23 million with 1 deal recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 3.51% | 7.46% |

| STOXX Europe 600 | -0.71% | 5.45% |

| Shanghai Composite (SSEC) | -0.22% | 5.02% |

| MSCI Emerging Market Index | 2.73% | 2.88% |

| MSCI World | 2.83% | 7.33% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -2.00% | -1.52% |

| JSE All Share | -1.67% | 3.13% |

| NSE All Share (NGSE) | -1.70% | 6.32% |

| DSEI (Tanzania) | -3.11% | -1.32% |

| ALSIUG (Uganda) | -4.94% | -5.51% |

- During the month, global markets posted mixed performance. In the USA, the S&P 500 and Dow Jones indices edged 3.51% and 1.89% higher respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 were down by 0.71% and 3.10%, amidst growing concerns over a banking crisis in the US.

- On a regional front, markets recorded a negative performance. The FTSE ASEA Pan African index, representing the overall African markets lost 2.00% from February. South Africa’s JSE All Share, Nigeria’s All Share Index, Tanzania’s DSEI and Uganda’s All Share Index all lost by 1.67%, 1.70%, 3.11% and 4.94% respectively.

- On the global commodities markets, oil futures indices remained volatile reflecting China’s demand rebound, Russia’s plan to cut production and major economies’ efforts to curb inflation by raising interest rates. Crude Oil WTI futures and ICE Brent Crude Oil settled 1.30% and 4.03% lower to close at $75.67 and $79.77 respectively.

Get future reports

Please provide your details below to get future reports: