MONTH’S HIGHLIGHTS

- The Monetary Policy Committee (MPC), in its November 23rd meeting, decided to raise the Central Bank Rate (CBR) by 50bps to 8.75%.

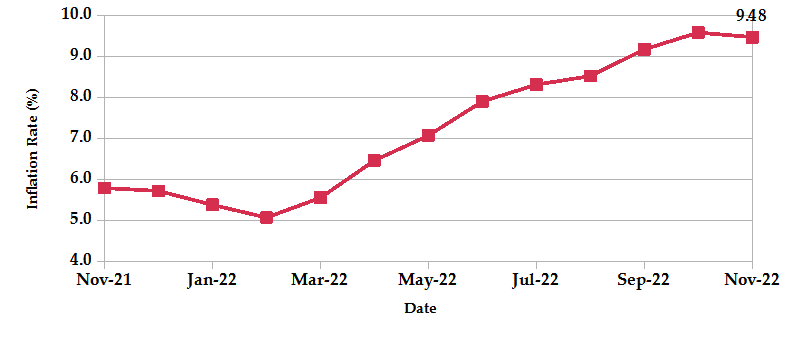

- Inflation declined to 9.5% in November from 9.6% in October due to eased food prices as food and non-alcoholic beverages inflation dropped from 15.8% to 15.4%. The housing, water, electricity, gas and other fuels category was notably lower at 0.4% on the back of lower electricity unit prices while transport dropped by 0.1% from a decline in diesel and petrol prices. Receding global energy prices and slowing demand in major importing countries largely contributed to the decline.

- The National Treasury released the Quarterly Economic and Budgetary Review Report for the period ending 30th September 2022, indicating that total revenue collected amounted to Kshs 596.6 billion, surpassing its Kshs 559.1 billion target. Government expenditure and net lending amounted to Kshs 759.5 billion, exceeding the Kshs 694.0 billion target by Kshs 65.5 billion, with domestic and foreign interest obligations accounting for 19.9% of the recurrent expenditure. The deficit should in essence be covered by borrowing, with net domestic borrowing settling below its Kshs 175.5 billion target at Kshs 101.6 billion while net foreign financing stood at Kshs 31.1 billion.

- Kenya’s daily foreign exchange reserves fell below their minimum statutory limit for the first time since 2015. CBK Governor assured that the reserves are expecting a boost from project loans, with IMF expected to release Kshs 52.83 billion in December under the current 38-month budgetary support programme. The IMF, during the month, reached a staff-level agreement with Kenyan authorities on the fourth review of the country’s economic program under the Extended Fund Facility (EFF) and Extended Credit Facility (ECF), with access to $433 million, bringing the total financial support under the arrangements to $1,548 million.

- The African Exchanges Linkage Project (AELP), poised to harmonize infrastructure in African capital markets to facilitate cross-border trading, went live. The platform integrates trading of exchange-listed securities across 7 bourses, including Nairobi Stock Exchange (NSE), Johannesburg Stock Exchange (JSE), Nigerian Stock Exchange (NGX), Stock Exchange of Mauritius (SEM), which represent about 85% of the region’s securities market capitalization.

- S&P Global reported a contraction in business activity across both the UK and US private sector. UK Composite PMI Output Index rose fractionally to 48.3 in November from 48.2 in October, while the US Index fell to 46.3 from 48.2. Companies attributed the downturn to rising cost of living, aggressive Fed rate hikes and weaker economic conditions that have weighed on demand in both domestic and export markets.

- The Organization of Petroleum Exporting Countries (OPEC) highlighted that the global oil demand growth forecast for 2022 stands at 2.5 million barrels per day (mb/d), while that of 2023 stands at 2.2 mb/d, a 0.1mb/d downward revision for both periods. Main supply drivers are expected to be the US, Norway, Brazil, Canada, Kazakhstan and Guyana while oil production is expected to decline in Russia following EU sanctions on imports, with countries moving to the Middle East to secure supply. OPEC has imposed a price cap of $60 per barrel on the region’s oil, to take effect from 5th December 2022, while the sanction prohibits maritime transport of Russian crude oil from 5th December 2022 and petroleum products from 5th February 2023.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 2.96% to settle at USD 7.07 billion (3.96 months of import cover). This falls below the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

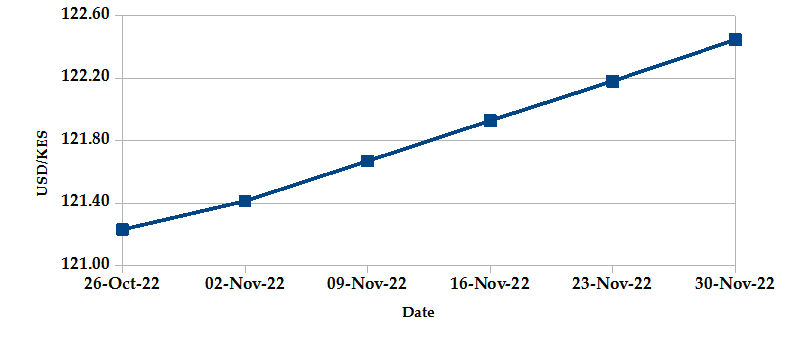

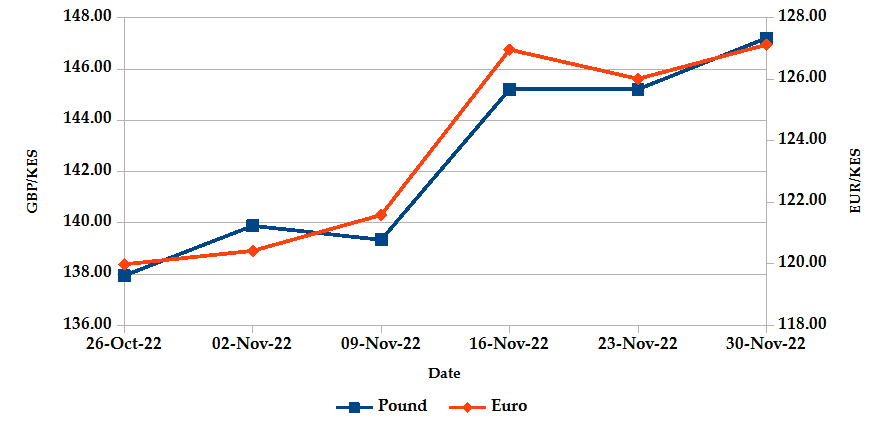

The Kenyan Shilling depreciated against the USD by 0.92%, exchanging at Kshs 122.45 at the end of the month up from Kshs 121.33 in the previous month. The depreciation is due to increased Dollar demand in the energy, oil and manufacturing sectors. The Shilling also depreciated against the Sterling Pound by 4.93% and the Euro by 4.98%, exchanging at Kshs 147.21 and Kshs 127.13 at the end of the month up from Kshs 140.30 and Kshs 121.09 respectively in the previous month.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

The overall year-on-year inflation marginally declined to 9.48% in the month of November from a revised figure of 9.59% in October. This is attributed to a decline in food, electricity and fuel prices as global energy prices receded amid slower demand.

INFLATION EVOLUTION

Liquidity

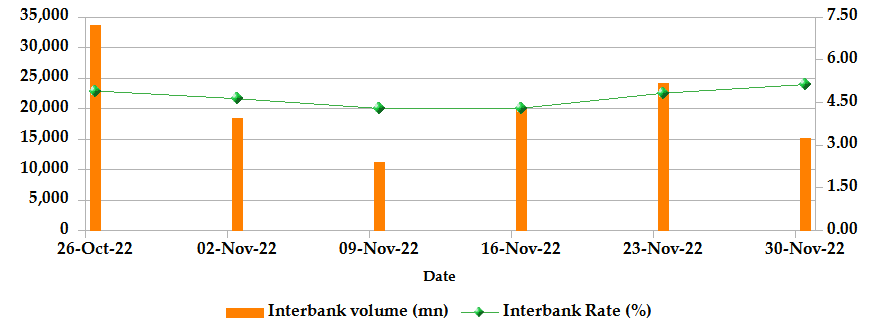

During the month, liquidity tightened as a result of tax remittances which offset government payments. The interbank rate rose to 5.14% from 4.80%. The volume of inter-bank transactions declined from Kshs 20.20 billion to Kshs 15.27 billion. Commercial banks excess reserves decreased from Kshs 26.0 billion to Kshs 13.0 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

T-Bills

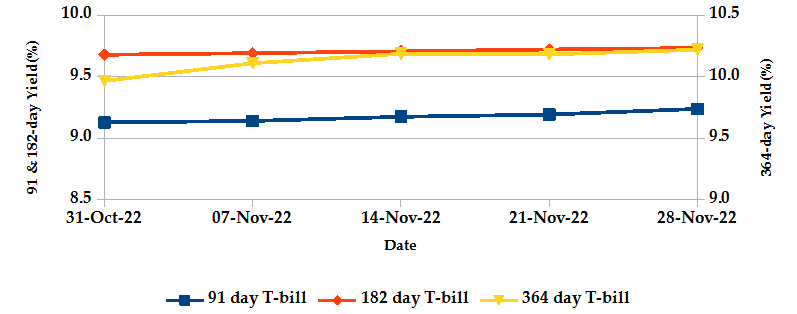

T-bills recorded an overall subscription rate of 167.66% at the end of November, compared to 105.11% recorded in the previous month. The increase in subscriptions was driven by ample market liquidity as well as improved yields on all issues during the month. The performance of the 91-day, 182-day and 364-day papers stood at 462.43%, 112.20% and 105.21% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 1.21%, 0.57% and 2.55% to 9.24%, 9.73% and 10.22% respectively.

T-BILLS

T-Bonds

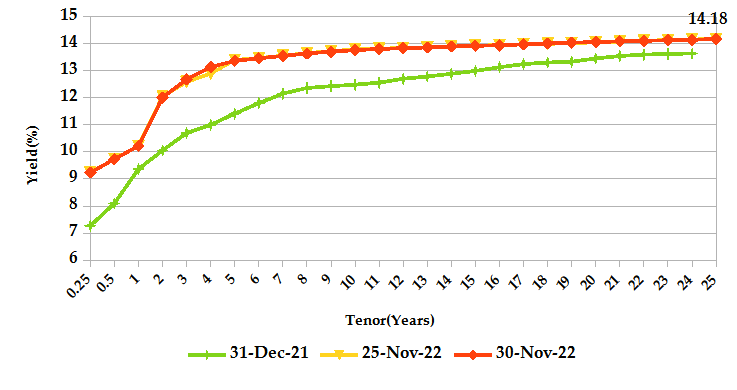

During the month, T-Bonds registered a turnover of Kshs 54.99 billion from 2,518 bond deals. This represents a monthly decline of 14.09% and an increase of 12.31% respectively. The yields on government securities in the secondary market slightly increased during the month of November.

In the primary market, CBK opened a tap sale for the infrastructure bond; IFB1/2022/14 seeking an additional Kshs 5.0 billion, reopened two bonds; FXD1/2008/20 and FXD1/2022/25 seeking to raise Kshs 40.0 billion and issued a new 6-year amortized infrastructure switch bond; IFB1/2022/6 seeking Kshs 87.8 billion.

In the international market, yields on Kenya’s Eurobonds declined by an average of 331.3 basis points.

YIELD CURVE

EQUITIES

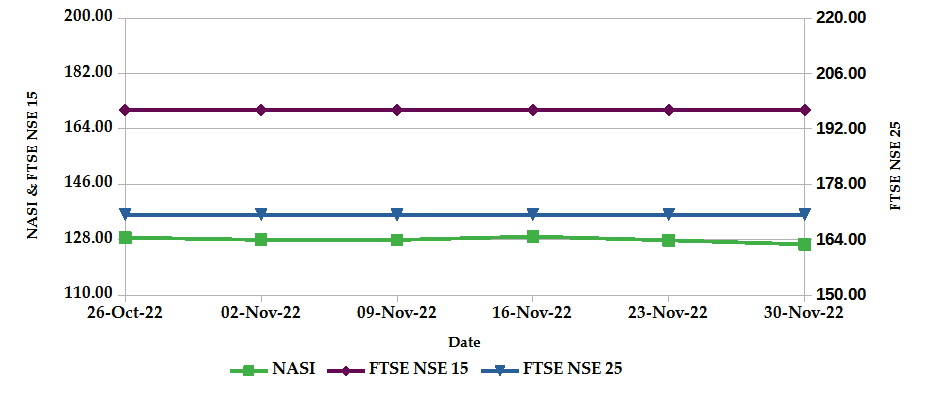

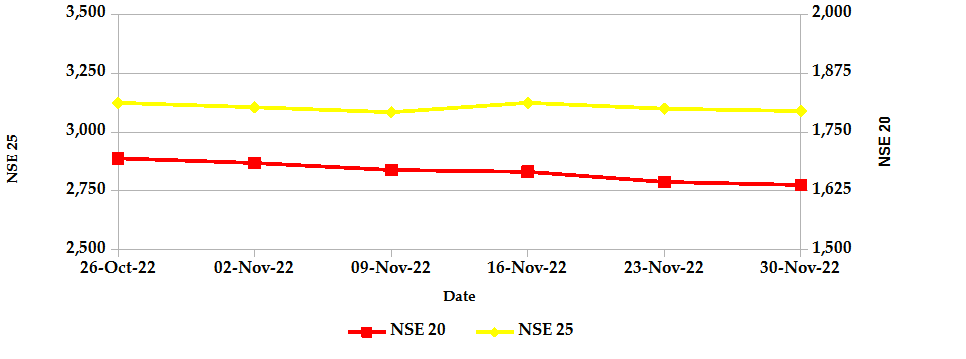

During the month of November, market capitalization declined by 1.80% to Kshs 1.97 trillion. Total shares traded slipped 14.31% to 39.55 million shares while equity turnover picked up 15.16% to Kshs 1.28 billion. On a monthly basis, NASI, NSE 20 and NSE 25 lost 1.80%, 2.40% and 1.06% respectively. The performance was a result of losses recorded by large-cap stocks such as Safaricom and Equity of 2.99% and 2.25% respectively, which were mitigated by gains posted by Standard Chartered and ABSA of 4.34% and 3.56% respectively.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 82 contracts with a turnover of Kshs 4.60 million which was a decrease from 141 contracts with a turnover of Kshs 8.33 million recorded in the previous month.

- I-REIT market over the month recorded a turnover of Kshs 0.99 million with 165 deals which was a decrease from Kshs 2.22 million with 166 deals recorded in the previous month.

- The ETF market over the month recorded a turnover of Kshs 289.77 million with 6 deals which was an increase from Kshs 120.49 million with 2 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 1.31% | 5.38% |

| STOXX Europe 600 | 0.28% | 6.75% |

| Shanghai Composite (SSEC) | 1.76% | 8.91% |

| MSCI Emerging Market Index | 4.29% | 14.64% |

| MSCI World Index | 0.87% | 6.80% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | 0.58% | 3.04% |

| JSE All Share | 3.07% | 14.22% |

| NSE All Share (NGSE) | 3.09% | 8.72% |

| DSEI (Tanzania) | 0.79% | 0.00% |

| ALSIUG (Uganda) | 0.93% | -2.35% |

- During the month, global markets edged higher after comments by several Fed officials confirmed that the pace of rate hikes could soon ease, backed by lower inflation. In the USA, the S&P 500 and Dow Jones indices gained 5.38% and 5.66% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 gained 6.75% and 6.74%, supported by improved consumer confidence and better-than-expected economic contraction.

- On a regional front, major indices posted monthly gains. The FTSE ASEA Pan African index, representing the overall African markets rose 3.04% from October. South Africa’s JSE All Share gained 14.22%, Nigeria’s All Share Index gained 8.72%, Tanzania’s DSEI remained relatively unchanged while Uganda’s All Share index declined by 2.35%.

- On the global commodities markets, oil futures indices declined following slowing global demand. China’s Covid-19 restrictions and related worker unrest as well as Russia-Ukraine tensions largely contributed to eased demand. Crude Oil WTI futures and ICE Brent Crude Oil settled 6.90% and 8.29% lower to close at $80.56 and $86.97 respectively.

Get future reports

Please provide your details below to get future reports: