Inflation declined to 6.80% in November from 6.92% in October, primarily driven by lower fuel prices. This led to a 0.1% marginal decline in the transport index. However, the food and non-alcoholic beverages index rose 0.4%, owing to higher food prices and despite a decrease in electricity and kerosene prices, the housing, water, electricity, gas and other fuels’ index rose 0.2%, mainly due to the rising cost of gas and cement.

Kenya has secured substantial financial support from the IMF and the World Bank Group to bolster its economic growth and development plans. The IMF agreed to expand access under the Extended Fund Facility (EFF) and Extended Credit Facility (ECF) by 130.3% of the quota, equivalent to $938 million, providing Kenya with immediate access to $682.3 million upon approval. This increases total IMF financial support for Kenya to $2.68 billion. In addition, the World Bank Group has committed a $12 billion loan package to Kenya over the next three years, starting July 2024.

The CMA approved the inclusion of First Future Holdings (FFH), an agent of Sterling Capital, into its regulatory sandbox. FFH aims to test a USSD-based platform that simplifies Central Depository System account opening and subsequent trading at the Nairobi Securities Exchange (NSE) in partnership with Sterling Capital. This platform will integrate with the Immigration Population Registration System (IPRS) and the Kenya Revenue Authority (KRA) to enable SMS-based trading of shares.

The National Treasury appointed Citi Bank and Standard Bank as joint lead managers to explore potential international US dollar capital markets funding and liability management options for Kenya. This move is expected to broaden Kenya’s access to more favourable financing terms, reduce its dependence on domestic borrowing and foster economic growth.

The IMF has revised its global growth forecast for 2024 downward to 2.9%, citing lingering pandemic effects, geopolitical tensions and supply chain disruptions. While 2023 is expected to hold steady at 3%, inflation is projected to remain high, rising to 6.9% this year and 5.8% next year. Despite these challenges, some economies, such as the US, Japan and the UK, are showing resilience. However, China and the Eurozone face headwinds and are expected to experience slower growth.

Euro area inflation eased to its lowest level in over two years in November 2023, dropping to 2.4% year-on-year. This decline was driven by a sharp drop in energy costs, which tumbled by 11.5% compared to -11.2% in October. Inflation rates for other categories also showed signs of moderation, including services prices which decreased to 4.0% from 4.6%, food, alcohol and tobacco prices decreased to 6.9% from 7.4%, and non-energy industrial goods inflation dropped to 2.9% from 3.5%. On a monthly basis, consumer prices fell by 0.5% in November, marking the largest monthly decline since January 2020.

The US Federal Reserve maintained its target range for the lending rate at a 22-year high of 5.25%-5.5% in November, for the second consecutive time, reflecting the Fed’s dual focus of bringing inflation back to its 2% target while avoiding a recession. The Fed Chair Jerome Powell signalled that the September dot plot, which showed most policymakers forecasting one more rate hike this year, may no longer be accurate. Powell also stated that the Fed has not discussed any rate cuts yet, as its primary focus remains on whether it will need to raise rates further.

The Bank of England kept its base interest rate at 5.25%, a 15-year high, at its November meeting, for the second consecutive time. Policymakers are closely monitoring the UK economy, which is showing signs of slowing down, while also trying to deal with the ongoing problem of high inflation. The Monetary Policy Committee (MPC) voted 6-3 to keep rates unchanged, with three members voting for a 0.25% increase. The central bank stressed that monetary policy will likely remain tight for some time in order to bring inflation back to its 2% target, and the MPC is ready to tighten policy further if needed.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the usable foreign reserves declined by 1.40% to settle at USD 6.74 billion (3.60 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

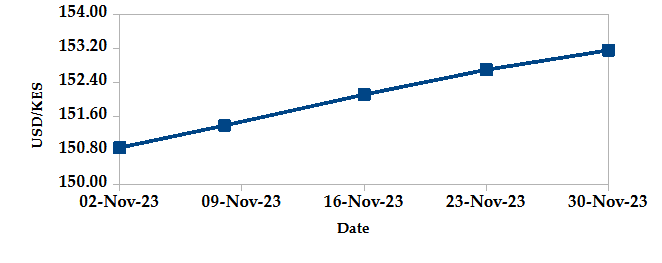

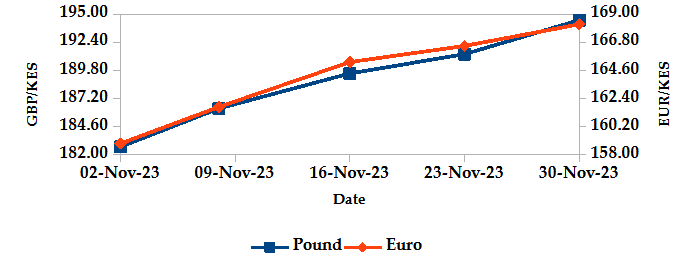

The Kenyan Shilling depreciated against the USD, the Sterling Pound and the Euro by 1.72%, 6.42% and 5.42%, exchanging at Kshs 153.15, Kshs 194.46 and Kshs 168.22 respectively at the end of the month, from Kshs 150.56, Kshs 182.72 and Kshs 159.56 in the previous month. The depreciation against the Dollar is attributed to rising demand from importers, which has caused a shortage in the market.

USD Vs KSHS

STERLING POUND & EURO Vs KSHS

Inflation

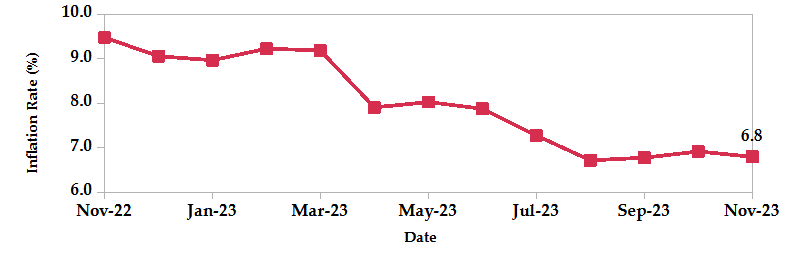

The overall year on year inflation decreased to 6.80% in November from 6.92% in October. This is primarily driven by lower fuel prices.

INFLATION EVOLUTION

Liquidity

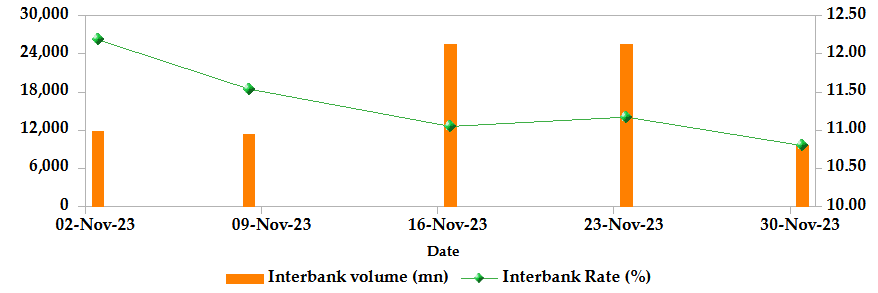

During the month, liquidity increased as a result of government payments which more than offset tax remittances. The inter-bank rate decreased from 12.52% to 10.80%. The volume of inter-bank transactions decreased from Kshs 10.38 billion to Kshs 9.67 billion. Commercial banks excess reserves increased from Kshs 19.80 billion to Kshs 23.10 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

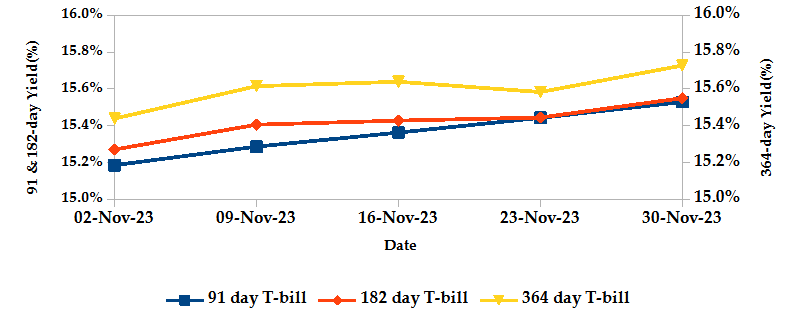

T-Bills

T-bills recorded an overall subscription rate of 156.43% during the month of November, compared to 129.32% recorded in the previous month. The performance of the 91-day, 182-day and 364-day papers stood at 701.20%, 68.69% and 26.26% respectively. On a monthly basis, yields on the 91-day, 182-day and 364-day papers increased by 2.77%, 2.78% and 2.21% to 15.53%, 15.55% and 15.73% respectively as investors aggressively bid to compensate for a weaker Shilling and inflationary pressures.

T-BILLS

T-Bonds

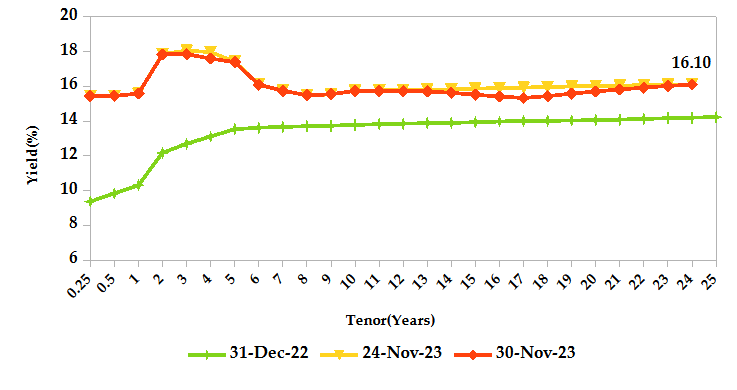

During the month, T-Bonds registered a total turnover of Kshs 55.99 billion from 2,843 bond deals. This represents a monthly increase of 61.89% and 85.09% respectively. The yields on government securities in the secondary market decreased during the month of November.

In the primary bond market, CBK reopened the 6.5-year infrastructure bond, IFB1/2023/6.5, through a tap sale in an effort to raise Kshs 25.0 billion. The coupon rate is 17.93% and the sale runs from 21/11/2023 to 06/12/2023.

In the international market, yields on Kenya’s Eurobonds decreased by an average of 119 basis points.

YIELD CURVE

EQUITIES

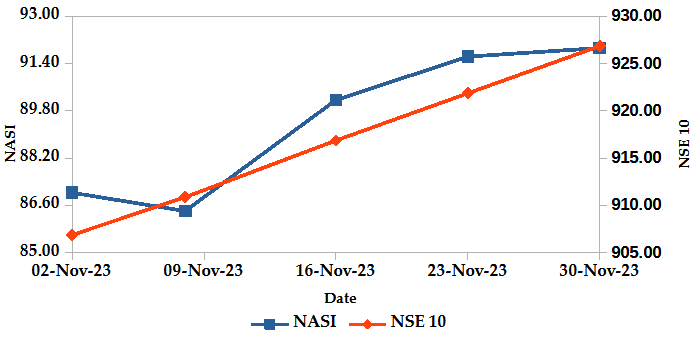

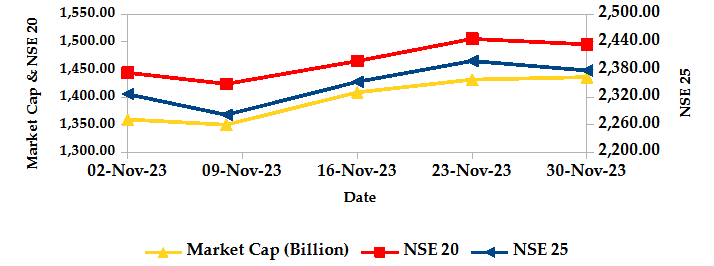

During the month, market capitalization gained 3.81% to settle at Kshs 1.44 trillion. Total shares traded increased by 15.23% to 310.01 million shares and equity turnover went up 11.29% to close at Kshs 4.31 billion. On a monthly basis, NASI, NSE 20, NSE 25 and NSE 10 settled 3.81%, 2.36%, 0.35% and 0.21% higher. The performance was as a result of gains recorded by large-cap stocks such as Safaricom, KCB and Standard Chartered of 12.85%, 7.71% and 0.96%. These were however weighed down by the losses recorded by other large cap stocks such as EABL, Stanbic and ABSA of 10.65%, 5.77% and 3.90%.

NASI and NSE 10

Market Capitalization, NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

The derivatives market, over the month, recorded a turnover of Kshs 4.70 million with 109 contracts, which was an increase from Kshs 4.02 million with 127 contracts recorded in the previous month.

I-REIT market, over the month, recorded a turnover of Kshs 10.46 million with 143 deals which was a decrease from Kshs 600.26 million with 40 deals recorded in the previous month.

The EFT market, over the month, recorded a turnover of Kshs 1.46 million with 1 deal, which was a decrease from Kshs 10.23 with 2 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

Global Markets

Weekly Change

Monthly Change

S&P 500

8.92%

19.45%

STOXX Europe 600

6.45%

6.32%

Shanghai Composite (SSEC)

0.36%

-2.79%

MSCI Emerging Market Index

7.86%

2.55%

MSCI World

9.21%

16.25%

Regional Markets

Weekly Change

Monthly Change

FTSE ASEA Pan African Index

6.62%

3.27%

JSE All Share

9.04%

1.88%

NSE All Share (NGSE)

3.08%

38.32%

DSEI (Tanzania)

-1.45%

-8.07%

ALSIUG (Uganda)

-2.75

-25.82%

Global markets registered gains during in the month. In the US, the S&P 500 gained 8.92% and the Dow Jones index gained 8.77%, buoyed by investors’ optimism following Federal Reserve Chair Jerome Powell’s remarks suggesting that interest rate hikes may be nearing their peak. In Europe, the STOXX Europe 600 and the UK’s FTSE 100 indices edged 6.45% and 1.80% higher, as data indicating a decline in inflation across the US and Europe fueled expectations of a potential shift towards lower interest rates by central banks. In Asia Pacific, the Shanghai Composite (SSEC) index gained 0.36%, fueled by reduced concerns over U.S. interest rate hikes, the Bank of Japan’s dovish signals and strategic bargain buying.

On a regional front, markets recorded mixed performance. The FTSE ASEA Pan African index, representing the overall African markets gained 6.62% from October. South Africa’s JSE All Share Index and Nigeria’s All Share Index also gained 9.04% and 3.08%, while Tanzania’s DSEI and Uganda’s All Share Index dropped by 1.45%, 2.75% respectively.

On the global commodities markets, oil future indices edged lower, fueled by investor uncertainty regarding the depth of OPEC+ supply reductions and concerns over sluggish global manufacturing activity. Crude Oil WTI futures and ICE Brent Crude Oil settled 6.25% and 7.49% lower to close at $75.96 and $80.86 respectively.

Get future reports

Please provide your details below to get future reports: