MONTH’S HIGHLIGHTS

- Inflation accelerated to 9.6% in October 2022 from 9.2% in September 2022 driven by an increase in food, fuel and electricity prices. Annual food inflation remained elevated at 15.8% largely due to the impact of drought that affected supply chains. Overall inflation is expected to remain elevated as fuel prices are expected to continue rising due to the Organization of the Petroleum Exporting Countries (OPEC)’s decision to make supply cuts as well as the partial lift on subsidies.

- Kenya National Bureau of Statistics Q2 2022 GDP report indicated that the country’s economy grew by 5.2%, slower than 11.0% in Q2 2021. A strong performance was recorded in sectors like Transportation and storage (7.1%), Financial and insurance (11.6%), Accommodation and food Services (22.6%), and Mining and quarrying (22.6%) among others. Agriculture, forestry and fishing reflected the effects of unfavourable weather conditions in their subdued performance.

- Stanbic Bank Kenya’s PMI dropped to 50.2 in October, after reaching a seven-month high of 51.7 in September, signalling a softer improvement in business conditions. High fuel costs, weaker shilling and supply shortages continue to weigh on input and production costs, reducing production capacity.

- Capital Markets Authority (CMA) approved the listing of Lap Trust Imara I-REIT by introduction on the NSE. Laptrust holds 100% of the I-REIT, therefore the security will not be offered to the public initially. It is set to be listed as a close-ended fund at Kshs 20 per unit, with a total of 346,231,413 units based on the net asset value of the scheme at the time of listing. The properties under the I-REIT include CPF Metro Park, CPF House, Pension Towers, Freedom Heights Mall and Service Plot, Man Apartment and Nova Eldoret.

- The Insurance Regulatory Authority released its Q2 2022 Quarterly report, indicating that the total industry exposure to capital market investments stood at Kshs 25.26 billion, representing a 2.8% allocation, compared to Kshs 33.16 billion (4.0%) a year earlier. This was attributed to the sustained sale of underperforming assets whose value dwindled with the bear market experienced at the bourse.

- The International Monetary Fund (IMF) downgraded its 2023 World Economic Outlook, projecting that global growth will slow to 2.7%. The cost of living crisis, tightening financial conditions, Russia-Ukraine tensions and the lingering COVID-19 pandemic continue to weigh heavily on the outlook.

- The US economy recorded a strong rebound in Q3 2022, posting a 2.6% GDP growth from a dismal 0.6% contrast in the second quarter. This reflected an increase in exports, consumer spending, non-residential fixed investment, and government spending which were offset by decreases in residential fixed investment and private inventory investment.

- European Central Bank announced its decision to raise interest rates by 75 basis points to 1.5%, the third major consecutive hike. The Governing Council maintained their stance that they would adjust all the instruments within their mandate to ensure that inflation returns to its 2% medium-term target.

ECONOMIC INDICATORS

Foreign Exchange Reserves

During the month, the CBK’s usable foreign reserves declined by 1.86% to stand at USD 7.29 billion(4.11 months of import cover). This meets the CBK’s statutory requirement to endeavour to maintain at least 4 months of import cover. However, it is below the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

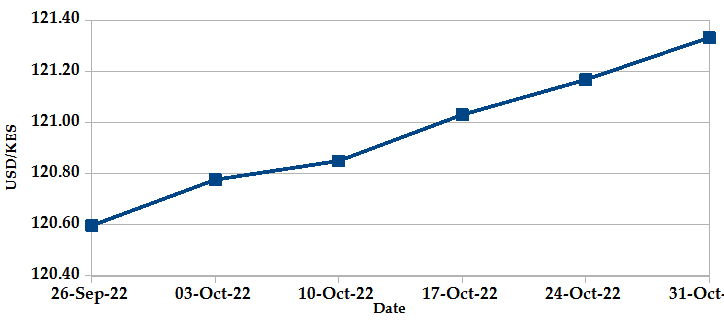

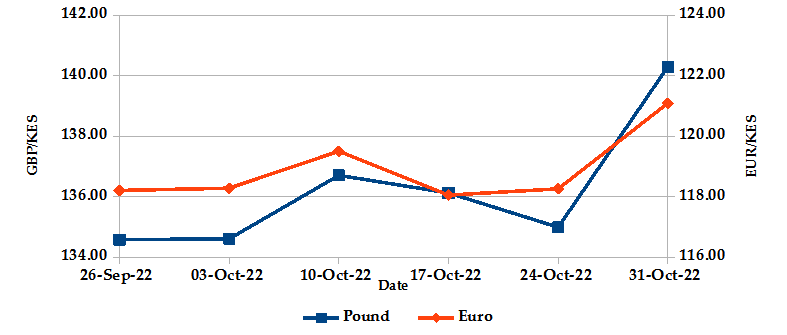

The Kenyan Shilling depreciated against the USD by 0.50%, exchanging at Kshs 121.33 at the end of the month up from Kshs 120.73 in the previous month. The depreciation is due to increased Dollar demand in the energy, oil and manufacturing sectors. The Shilling also depreciated against the Sterling Pound by 7.37% and the Euro by 3.38%, exchanging at Kshs 140.30 and Kshs 121.09 at the end of the month up from Kshs 130.66 and Kshs 117.13 respectively at the previous month.

USD Vs KSHS

STERLING POUND Vs KSHS

Inflation

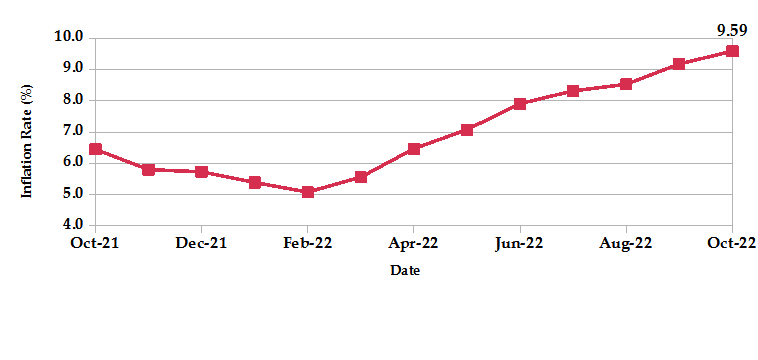

The overall year-on-year inflation increased to 9.59% in the month of October up from a revised figure of 9.18% in September. The increase is attributable to a rise in food and fuel prices due to persistent supply chain disruptions and rising global energy prices.

INFLATION EVOLUTION

Liquidity

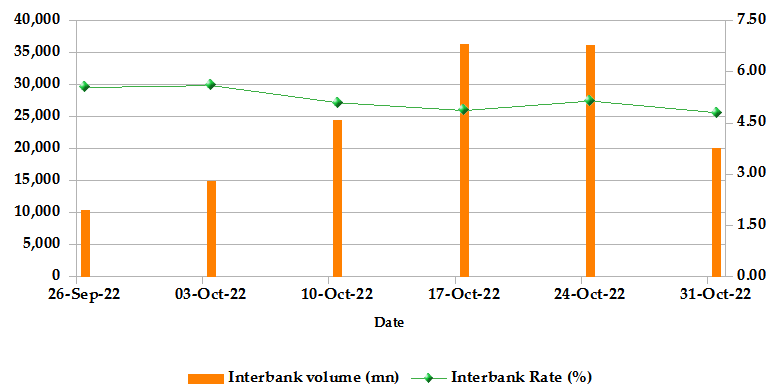

During the month, liquidity increased as a result of government payments which more than offset tax remittances. The inter-bank rate decreased to 4.80% down from 5.68%. The volume of inter-bank transactions increased from Kshs 8.69 billion to Kshs 20.20 billion. Commercial banks excess reserves increased from Kshs 13.40 billion to Kshs 26.00 billion.

INTER-BANK RATE and VOLUME

FIXED INCOME

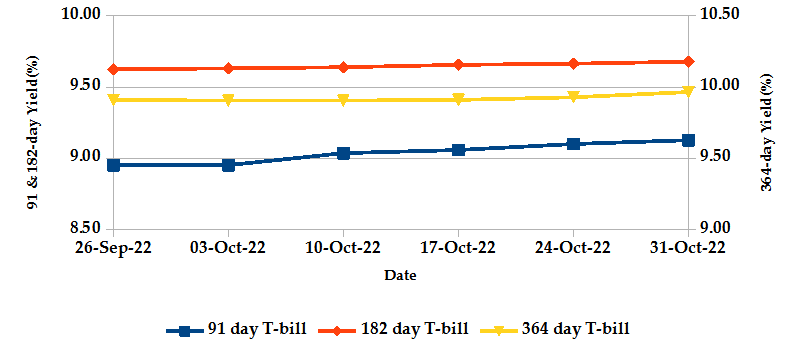

T-Bills

T-bills recorded an overall subscription rate of 105.11% at the end of the month of October, compared to 83.85% recorded in the previous month. The over-subscription is partly attributable to increased liquidity. The performance of the 91-day, 182-day and 364-day papers stood at 373.4%, 69.5% and 33.4% respectively. On a monthly basis, the yields on the 91-day, 182-day and 364-day papers increased by 1.45%, 0.42% and 0.20% respectively to 9.08%, 9.66% and 9.93%.

T-BILLS

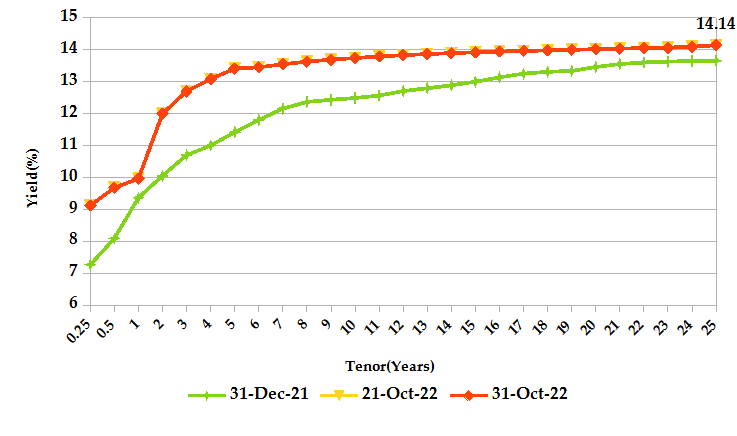

T-Bonds

At the end of the month, T-Bonds registered a turnover of Kshs 2.07 billion from 126 bond deals. This represents a monthly decline of 36.22% and an increase of 12.50% respectively. The yields on government securities in the secondary market slightly increased during the month of October.

In the primary market, CBK issued a 14-year infrastructure bond; IFB1/2022/14 seeking to raise Kshs 60 billion. The bond’s interest rate is set to be market-determined.

In the international market, yields on Kenya’s Eurobonds declined by an average of 63 basis points.

YIELD CURVE

EQUITIES

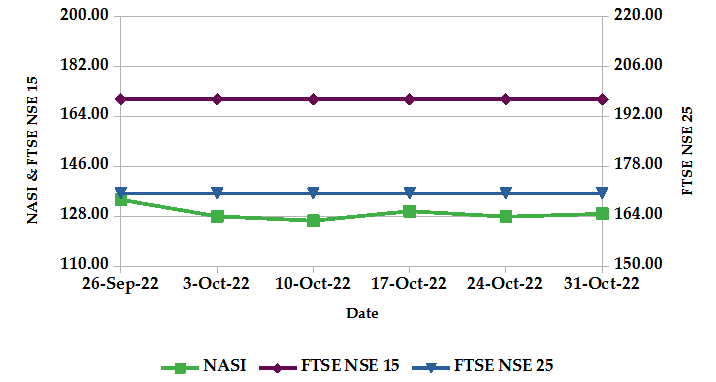

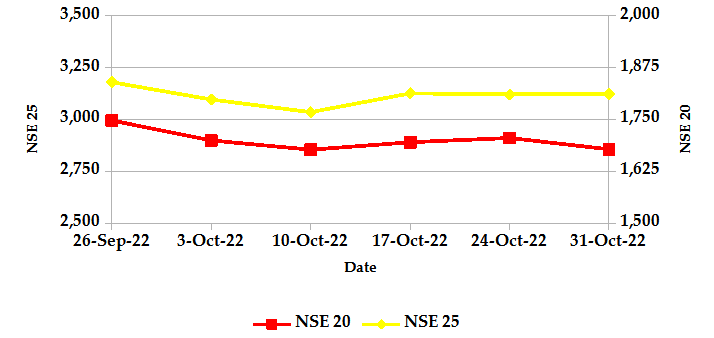

During the month of October, market capitalization increased by 0.30% to Kshs 2.01 trillion. Total shares traded and equity turnover plunged by 18.42% and 25.17% to Kshs 46 million shares and Kshs 1.1 billion respectively. NASI and NSE 25 increased by 0.3% and 0.6% respectively, while NSE 20 declined by 2.3% on a monthly basis. On a weekly basis, the NASI and NSE 25 gained by 0.8% and 0.1% respectively while NSE 20 dropped by 1.6%. The mixed performance is a result of an appreciation of large-cap stocks such as EABL and Standard Chartered, which were weighed down by losses recorded by KCB and ABSA.

NASI, FTSE NSE 15 and FTSE NSE 25

NSE 20 and NSE 25

ALTERNATIVE INVESTMENTS

- The derivatives market over the month recorded 141 contracts having a turnover of Kshs 8.3 million which was a decrease from 145 contracts having a turnover of Kshs 16.3 million recorded in the previous month.

- I-REIT market over the month recorded a turnover of Kshs 2.2 million with 166 deals which was an increase from Kshs 1.3 million with 150 deals recorded in the previous month.

- The ETF market over the month recorded a turnover of Kshs 120.5 million with 2 deals which was an increase from Kshs 44.4 million with a similar 2 deals recorded in the previous month.

GLOBAL AND REGIONAL MARKETS

| Global Markets | Weekly Change | Monthly Change |

|---|---|---|

| S&P 500 | 1.97% | 7.99% |

| STOXX Europe 600 | 2.58% | 6.28% |

| Shanghai Composite (SSEC) | -2.82% | -4.33% |

| MSCI Emerging Market Index | 0.64% | -3.15% |

| MSCI World Index | 2.19% | 7.11% |

| Regional Markets | Weekly Change | Monthly Change |

|---|---|---|

| FTSE ASEA Pan African Index | -1.44% | -2.67% |

| JSE All Share | 2.68% | 4.60% |

| NSE All Share (NGSE) | -1.40% | -10.58% |

| DSEI (Tanzania) | -0.23% | 0.45% |

| ALSIUG (Uganda) | 0.75% | -0.45% |

- During the month, major global markets gained reflecting investors’ relief following a report that indicated that the Federal Reserve’s rate hikes were expected to slow in December. In the USA, the S&P 500 and Dow Jones indices rose by 7.99% and 13.94% respectively from the previous month. In Europe, the continental index of STOXX Europe 600 and the UK’s FTSE 100 gained 6.28% and 2.91%, rising above troubled political and fiscal policies.

- On a regional front, markets recorded mixed performance, picking up on global inflationary pressure that rippled to rising food and energy costs. The FTSE ASEA Pan African index, representing the overall African markets declined by 2.67% from the month of September. South Africa’s JSE All Share gained 4.60%, Nigeria’s All Share Index declined by 10.58%, Tanzania’s DSEI rose 0.45% and Uganda’s All Share Index declined by 0.45%.

- On the global commodities markets, the oil futures indices gained following OPEC’s decision to make supply cuts. Elevated inflation numbers, tightened monetary policies around the globe, tension from the Russia-Ukraine war and the lingering COVID-19 pandemic have kept energy prices high. The Crude Oil WTI futures and ICE Brent Crude Oil rose 9.92% and 7.81% respectively from the previous month.

Get future reports

Please provide your details below to get future reports: