Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,939 million (3.88 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar but strengthened against the Sterling Pound and the Euro to exchange at KES 125.08, KES 152.06 and KES 134.73 respectively. The observed depreciation against the Dollar is attributed to increased demand from importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 1.34% | 0.39% |

| Sterling Pound | 2.24% | -0.73% |

| Euro | 2.34% | -1.23% |

Liquidity

Liquidity in the money markets slightly increased with the average interbank rate dropping from 6.49% to 6.46%, as government payments offset tax remittances. Remittance inflows totaled $349.40 million in January 2023, a 2.21% decline from $357.30 in December 2022 and a 3.16% increase from $338.70 in January 2022. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.49% | 6.46% |

| Interbank volume (billion) | 29.93 | 16.05 |

| Commercial banks’ excess reserves (billion) | 11.80 | 12.40 |

Fixed Income

T-Bills

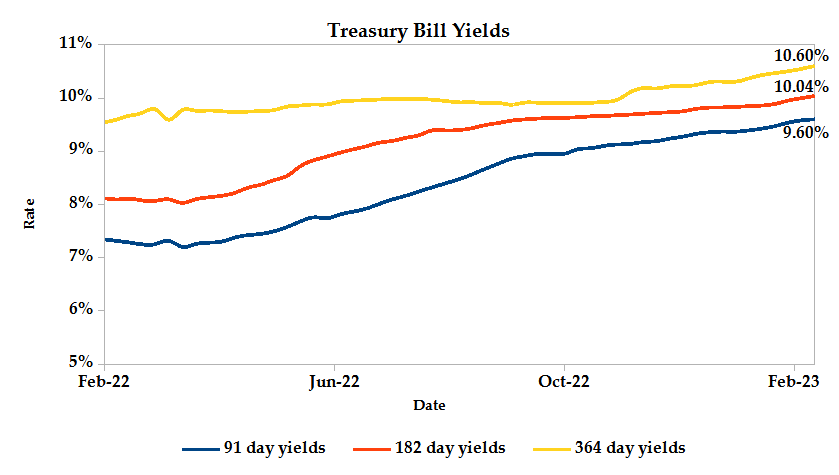

T-Bills remained over-subscribed during the week, with the overall subscription rate coming in at 187.09%, down from 208.85% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 779.97% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 93.26% and 43.76% respectively. The acceptance rate rose by 39.90% to close the week at 90.51%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover declined by 12.57% from KES 11.43 billion in the previous week to KES 10.00 billion. Total bond deals declined by 9.40% from 638 in the previous week to 578.

In the primary market, CBK released auction results for the reopened FXD1/2017/010 and the newly issued FXD1/2023/010 which sought to raise KES 50.0 billion. The issues received bids worth KES 19.54 billion, representing a subscription rate of 39.09%. KES 16.75 billion worth of bids were accepted at a weighted average rate of 13.88% for the reopened paper and 14.15% for the new issue.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average 0.29% compared to the previous week, declined by 0.04% month to date and 0.58% year to date. The yield on the 10-year Eurobond for Ghana declined while that of Angola increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | -2.12% | -0.44% | 0.15% |

| 2018 10-Year Issue | 0.38% | 0.68% | 0.96% |

| 2018 30-Year Issue | -0.38% | -0.12% | 0.10% |

| 2019 7-Year Issue | -0.68% | -0.22% | 0.11% |

| 2019 12-Year Issue | -0.56% | -0.10% | 0.18% |

| 2021 13-Year Issue | -0.09% | -0.02% | 0.23% |

Equities

NASI dropped 0.77% while NSE 20 and NSE 25 edged 0.46% and 0.11% higher compared to the previous week bringing the year to date performance to 0.71%, -0.21% and 1.42% respectively. Market capitalization settled 0.76% lower from the previous week, closing at KES 2.00 trillion and recording a year to date gain of 0.72%. The performance was driven by losses recorded by Safaricom of 2.45%. These were however mitigated by gains recorded by large-cap stocks such as KCB, ABSA, Co-operative and EABL of 1.44%, 1.21%, 1.20% and 1.12% respectively.

The Banking sector had shares worth KES 667M transacted which accounted for 48.27% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 186M transacted which represented 13.51% and Safaricom, with shares worth KES 483.6M transacted represented 34.98% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| HF Group | 12.70% | 9.57% |

| Express Kenya | 3.67% | 9.09% |

| Liberty | -0.99% | 8.48% |

| NCBA | -3.59% | 5.77% |

| Williamson Tea | 8.91% | 5.61% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Trans-Century | 15.15% | -10.24% |

| Uchumi | -9.52% | -9.52% |

| EA Cables | 3.53% | -7.37% |

| Unga | -18.75% | -7.14% |

| Home Afrika | -5.88% | -5.88% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.23 | 0.82 | -33.32% |

| Derivatives Contracts | 12 | 15 | 25.00% |

| I-REIT Turnover (million) | 0.70 | 1.48 | 110.95% |

| I-REIT deals | 57 | 113 | 98.25% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 6.96% | -1.11% |

| Dow Jones Industrial Average (DJI) | 2.22% | -0.16% |

| FTSE 100 (FTSE) | 4.35% | -0.24% |

| STOXX Europe 600 | 5.46% | -0.63% |

| Shanghai Composite (SSEC) | 4.63% | -0.08% |

| MSCI Emerging Markets Index | 5.31% | -2.41% |

| MSCI World Index | 7.04% | -1.31% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 1.59% | 2.46% |

| JSE All Share | 6.81% | -1.44% |

| NSE All Share (NGSE) | 5.29% | 0.21% |

| DSEI(Tanzania) | 2.27% | 0.39% |

| ALSIUG (Uganda) | -0.32% | -0.03% |

US indices pared losses in a week dominated by hawkish commentary by Federal Reserve officials and release of earnings reports from a number of the S&P 500 counters. Energy stocks kept losses in check, with oil prices rising amid news of Russia’s plans to cut crude supplies.

European stocks took a dip after data from December’s economic check revealed that the UK economy narrowly evaded technical recession. Industrial stocks gave the biggest boost to the STOXX 600 index supported by better than expected production numbers and corporate earnings reports.

Asia Pacific indices traded lower over the week, tracking the US market. Hong Kong’s Hang Seng index sank nearly 2%, weighed down by technology stocks anticipating a downturn in the chip industry as tensions persist between US and China.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 8.95% and 8.07% higher at $79.75 and $86.39 respectively. Gold futures prices settled 0.01% lower at $1,862.80.

Week’s Highlights

- The National Treasury submitted Supplementary budget documents to Parliament which projected an increase in the total budget estimates for 2022/23 from KES 3.36 trillion captured in the original budget presented to parliament in April, to KES 3.37 trillion. The change is mainly driven by a 6.62% increase in recurrent expenditure estimates from KES 1.40 trillion to KES 1.50 trillion. Additionally, to adhere to set debt limits, the overall fiscal deficit has been revised downwards from 6.2% originally projected to 5.7% of GDP.

- CMA facilitated an engagement with Sanduku Investment Initiative, Association of Pension Trustees and Administrators of Kenya and the NSE towards the creation of a Kenya National Real Estate Investment Trust (KNR). The collaboration is aligned with the Government’s Economic Transformation Agenda towards delivering affordable housing units and is set to unlock access to capital through capital markets. The Fund Managers Association and the RBA will work with trustees of pension funds in reviewing investment mandates to facilitate their participation in REITs as an alternative asset class.

- Acorn Holdings Limited announced a KES 6.7 billion green financing partnership with Absa Bank for the development of an additional 12,000 units of affordable student housing in Nairobi and its environs. The facility is part of a KES 11 billion financing package, with the balance to be covered by Equity through the Acorn Student Accommodation REITs.

- China’s year on year inflation rate rose to 2.1% in January 2023 from 1.8% in December, as prices edged higher due to the surge in spending over the Lunar New Year festival and relaxed pandemic measures. The economy still faces headwinds including an ailing property sector, weakening external demand reported by Chinese exporters and high levels of youth unemployment. Monthly PPI declined by 0.4%, suggesting that the manufacturing sector is yet to pick up with lower factory-gate prices affected by falling input prices, lower crude and domestic coal prices.

- Russia announced plans to voluntarily reduce production by 500,000 barrels per day starting March, in response to price caps imposed by major economies. The cut, an estimated 5% of Russian oil output, is expected to contribute to restoration of market relations. The lower production coupled with anticipated elevated demand amid China’s reopening will tighten oil markets further over the coming quarters.

- UK’s economy recorded zero growth in the fourth quarter of 2022 after a 0.3% contraction in the third quarter. GDP is estimated to have risen by 0.5% in October, followed by 0.1% in November but fell 0.5% in December. Output was 0.8% below pre-pandemic levels, compared to other major economies whose growth and recovery have been restored. Business investment, however, is back to the same level as three years earlier, but future growth will be stifled by a steep increase in taxation on profits taking effect in April.

Get future reports

Please provide your details below to get future reports: