Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,235 million (4.05 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover. However, it does not meet EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at KES 121.78, KES 122.20 and KES 139.92 respectively. The observed depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 7.64% | 0.23% |

| Euro | -4.60% | 2.82% |

| Sterling Pound | -8.15% | 2.21% |

Liquidity

Liquidity in the money markets eased with the average interbank rate declining from 4.41% to 3.84%, as government payments offset tax remittances. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 4.41% | 3.84% |

| Interbank volume (billion) | 19.82 | 12.30 |

| Commercial banks’ excess reserves (billion) | 25.00 | 28.80 |

Fixed Income

T-Bills

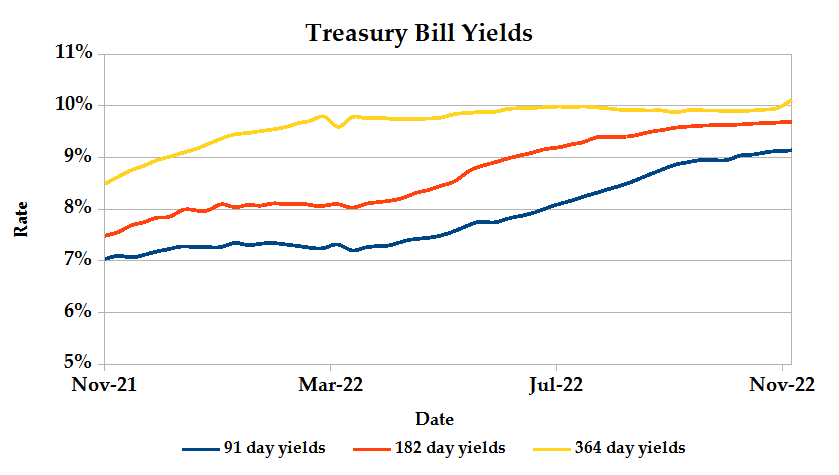

T-Bills remained over-subscribed during the week with an increase in the overall subscription rate from 181.88% recorded in the previous week to 204.53%. The 91-day T-Bill received the highest subscription rate at 662.83% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 138.92% and 86.83% respectively. The acceptance rate dropped by 13.63% to close the week at 78.10%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 53.19% from KES 8.36B in the previous week to KES 12.81B. Total bond deals declined by 34.77% from 512 in the previous week to 334.

In the primary bond market, CBK released auction results for the 14-year infrastructure bond, IFB1/2022/14, which sought to raise KES 60 billion. The issue was over-subscribed, receiving bids worth KES 91.85 billion, out of which KES 75.57 billion was accepted at a weighted average rate of 13.94%. The performance is mainly attributed to the tax incentive attached to infrastructure bonds.

Eurobonds

In the international market, yields on Kenya’s Eurobonds declined by an average 2.39% compared to the previous week, 2.41% month to date and increased 5.30% year to date. The yields on the 10-year Eurobond for Ghana increased while that of Angola declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 8.39% | -2.91% | -2.87% |

| 2018 10-Year Issue | 5.73% | -2.18% | -2.07% |

| 2018 30-Year Issue | 3.54% | -1.57% | -1.55% |

| 2019 7-Year Issue | 5.66% | -3.10% | -3.18% |

| 2019 12-Year Issue | 4.93% | -2.39% | -2.26% |

| 2021 12-Year Issue | 3.55% | -2.30% | -2.40% |

Equities

NASI gained by 0.42% while NSE 20 and NSE 25 dropped by 0.55% and 0.15% respectively compared to the previous week bringing the year to date performance to -23.35%, -12.95% and -17.79% respectively. Market capitalization gained by 0.42% from the previous week to close at KES 2.0 trillion recording a year to date decline of 23.33%. The performance was driven by losses recorded by large-cap stocks such as EABL, Equity and KCB of 4.26%, 1.31% and 1.08% respectively. These were however boosted by gains recorded by ABSA, Safaricom and Co-op of 2.63%, 1.81% and 0.85% respectively.

The Banking sector had shares worth KES 273M transacted which accounted for 22.37% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 387M transacted which represented 31.68% and Safaricom, with shares worth KES 486M transacted represented 39.80% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Olympia | 40.00% | 8.13% |

| Longhorn | -12.85% | 7.45% |

| ABSA New Gold ETF | 7.18% | 7.18% |

| Home Afrika | -10.00% | 5.88% |

| Uchumi | 13.04% | 4.00% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| NBV | -39.44% | -12.02% |

| Flame Tree | -14.40% | -10.08% |

| TP Serena | -10.82% | -9.33% |

| Williamson Tea | 16.15% | -8.35% |

| Eaagads | -18.52% | -8.33% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 3.26 | 1.58 | -51.48% |

| Derivatives Contracts | 47 | 30 | -36.17% |

| I-REIT Turnover | 0.17 | 0.19 | 11.69% |

| I-REIT Deals | 27 | 36 | 33.33% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -16.75% | 5.90% |

| Dow Jones Industrial Average (DJI) | -7.75% | 4.15% |

| FTSE 100 (FTSE) | -2.49% | -0.23% |

| STOXX Europe 600 | -11.78% | 3.66% |

| Shanghai Composite (SSEC) | -15.01% | 0.54% |

| MSCI Emerging Markets | -27.88% | 0.52% |

| MSCI World Index | -18.66% | 5.16% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -28.82% | 0.19% |

| JSE All Share | -0.85% | 5.87% |

| NSE All Share (NGSE) | 2.19% | -0.68% |

| DSEI (Tanzania) | -2.59% | -0.61% |

| ALSIUG (Uganda) | -14.98% | -2.78% |

All major US indices closed sharply higher extending the streak that started on Thursday after release of the annual inflation data which eased to 7.7% in October from 8.2% in September, affirming hopes of less aggressive interest rate hikes. Technology stocks boosted Nasdaq’s gains, healthcare stocks weighed on the Dow while S&P gains were led by energy and communication stocks.

European stocks ended the week mixed, with export-oriented FTSE 100 slipping 0.23% on the back of a stronger Sterling Pound following a better than expected contraction of the economy and the Dollar plunging after US inflation report. STOXX 600 gains were led by financial service, mining and retail stocks.

Asia Pacific stocks rallied with technology-heavy index Hang Seng recording the best performance at 7.21% week on week gains after US inflation data and China’s withdrawal of some Covid related restrictions.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 4.04% and 2.74% lower respectively. Gold futures prices rose by 5.76% to settle at $1,773.15.

Week’s Highlights

- The International Monetary Fund (IMF) reached a staff-level agreement with Kenyan authorities on the fourth reviews of the country’s economic program supported by IMF’s Extended Fund Facility (EFF) and Extended Credit Facility (ECF). Upon approval of the agreement, Kenya will have access to USD 433 million, bringing the total financial support under these arrangements to USD 1,548 million. This comes at a time when the country has defaulted on KES 84.6 billion debt repayment obligations in the year ending June 2022.

- Acorn Holdings received KES 1.79 billion from the sale of Qwetu Aberdare Heights hostel, which was transferred to Acorn Student Accommodation I-Reit last month. Part of the proceeds are expected to be used to repay KES 800 million out of its outstanding KES 5.7 billion green bond. The early redemption is set to significantly reduce the property developer’s finance costs in terms of interest payments.

- The African Development Bank, in partnership with the Eastern and Southern African Trade and Development Bank (TDB), launched an equity instrument set to catalyze financing for sustainable development in the continent at the ongoing global Climate Change Conference (COP 27). The African Development Bank made an investment commitment of USD 15 million in TDB’s Class C Green+ shares, having taken the lead in the Class B shares which targets institutional investors such as pension funds and sovereign wealth funds.

- US Bureau of Labor Statistics released October inflation data, indicating that the annual rate dropped to 7.7% from 8.2% in September, settling below 8% for the first time in eight months. Gains in the index were attributed to rising energy, food and housing prices by 1.8%, 0.6% and 0.8% respectively. The report sparked a rally on Wall Street, sent Treasury yields on a nosedive and the dollar dipped against a basket of major currencies, with the Bloomberg Dollar Spot Index indicating a 2% drop.

- UK economy contracted by 0.2% in the third quarter, the first GDP drop since the beginning of 2021, signaling what might be the start of a prolonged recession. The slump is reported to be as a result of continued weaknesses in household and business confidence, higher inflation and higher interest rates in the economy.

- Credit Rating Agency, Fitch Ratings revised Egypt’s Long-Term Foreign-Currency Issuer Default Rating (IDR) from Stable to Negative, affirming it at ‘B+’. The revision reflects the country’s dwindling liquidity, reduced prospects for bond market access and decline in foreign exchange reserves to less than USD 32 billion in October from USD 35 billion in March and USD 40 billion in February.

Get future reports

Please provide your details below to get future reports: