Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,682 million (4.43 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover, and the EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at Ksh 119.31, Ksh 122.89 and Ksh 145.42 respectively. The observed overall depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 5.46% | 0.18% |

| Euro | -4.06% | 1.30% |

| Sterling Pound | -4.54% | 0.63% |

Liquidity

Liquidity in the money markets tightened, partly reflecting tax remittances which offset government payments. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 5.25% | 5.60% |

| Interbank volume (billion) | 20.9 | 30.3 |

| Commercial banks’ excess reserves (billion) | 27.4 | 27.2 |

Fixed Income

T-Bills

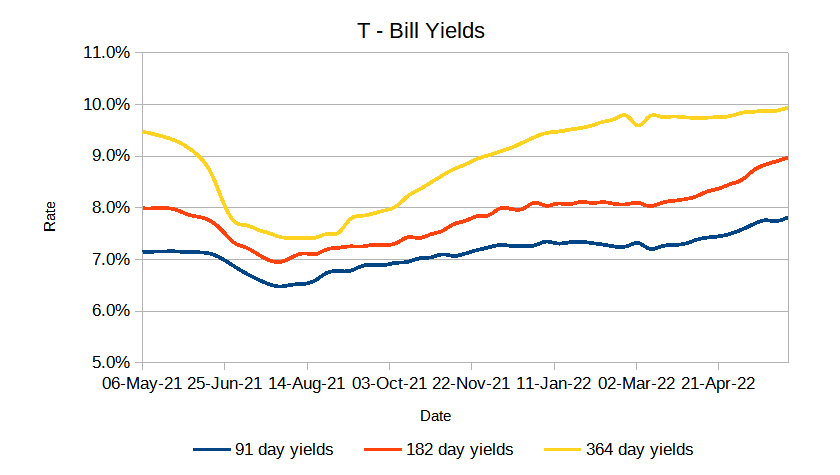

T-Bills were over-subscribed during the week with an increase in the overall subscription rate from 48.27% recorded in the previous week to 72.36%. The 91-day T-Bill got the highest subscription rate at 299.8% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 39.3% and 36.9% respectively. The acceptance rate increased by 1.1% to close the week at 99.69%.

T-Bonds

The bonds market had a lower demand for the week’s bond offers. Bonds turnover decreased by 45.84% from 3.67B in the previous week to 1.99B. Total bond deals decreased by 23.01% from 113 in the previous week to 87.

In the primary bond market, the Central Bank released results for the two re-opened fifteen year treasury bonds ; FXD2/2013/15 and FXD2/2018/15 each receiving bids worth 5.45B and 5.12B respectively.

Eurobonds

In the international market, the yields on the 10-year Eurobonds for Angola decreased and increased for Ghana. Yields on Kenya’s Eurobonds generally decreased by 2.49% compared to the previous week, -2.383% and 5.688% month to date and year to date respectively. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 7.79% | -2.56% | -3.13% |

| 2018 10-Year Issue | 6.43% | -2.41% | -2.55% |

| 2018 30-Year Issue | 3.40% | -1.92% | -1.86% |

| 2019 7-Year Issue | 7.41% | -3.06% | -3.15% |

| 2019 12-Year Issue | 5.45% | -1.75% | -1.82% |

| 2021 12-Year Issue | 3.65% | -2.60% | -2.40% |

Equities

NASI, NSE 20 and NSE 25 increased by 3.43%, 4.22% and 3.59% compared to last week bringing the year to date performance to -12.10%, -6.00% and -9.02% respectively. The market capitalization increased by 3.44% from the previous week to close at 2.289 trillion recording a year to date decline of -12.04%. The performance was driven by gains recorded by large-cap stocks. Top gains were recorded in Co-operative Bank, ABSA Bank, Equity Group Holdings and Safaricom which increased by 7.56%, 5.26%, 4.66%, 3.49% respectively.

The Banking sector had shares worth Ksh 432M transacted which accounted for 39.75% of the week’s traded value, Manufacturing & Allied sector had shares worth Ksh 33.6M transacted which represented 3.09% and Safaricom, with shares worth Kshs 561M transacted represented 51.71% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Uchumi supermarket | 17.39% | 12.50% |

| TPS Eastern Africa | 11.15% | 10.78% |

| Scangroup plc | -4.63% | 9.83% |

| Limuru Tea company | 58.44% | 9.74% |

| Trans-century plc | 8.33% | 8.33% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| B.O.C Kenya | 1.79% | -2.73% |

| Sasini | 11.23% | 0.95% |

| Sameer | 24.56% | 0.00% |

| EA portland | 17.54% | 0.00% |

| I&M Holdings | -20.56% | 0.00% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.41 | 0.39 | -4.40% |

| Derivatives Contracts | 19 | 14 | -26.32% |

| I-REIT Turnover | 0.028 | 0.56 | -57.04% |

| I-REIT Deals | 3 | 11 | -94.18% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -10.77% | 3.26% |

| Dow Jones Industrial Average (DJI) | -7.72% | 2.93% |

| FTSE 100 (FTSE) | -0.06% | 0.82% |

| STOXX Europe 600 | -10.02% | 1.18% |

| Shanghai Composite (SSEC) | -9.79% | 1.55% |

| MSCI Emerging Markets | -17.57% | 1.39% |

| MSCI World Index | -12.55% | 3.00% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -20.17% | 0.64% |

| JSE All Share | -4.52% | 1.40% |

| NSE All Share (NGSE) | 15.43% | -2.09% |

| DSEI (Tanzania) | 1.56% | 0.86% |

| ALSIUG (Uganda) | -4.84% | 3.16% |

US stocks closed the week higher as gains in the Technology, Consumer goods and services sectors led shares higher. Signs that inflation may have peaked in July increased investor confidence that a bull market could be underway and spurred the S&P 500 and Nasdaq. Annual inflation moderated to 8.5 percent in July compared to 9.1 percent in June raising prospects of a less aggressive rate hike by the US Federal Reserve than previously expected.

European stocks closed the higher in cautious trading after the UK economy contracted in the second quarter with gains in the Healthcare and Leisure sector with each gaining 0.2% and 3.9% respectively. STOXX 600 notched weekly gains of 1.2% as positive earnings and a softer-than-expected US inflation reading calmed nerves amid aggressive rate hikes by the Federal Reserve.

Asia Pacific stocks closed the week mixed. Japan stocks rose with gains in the Power, Chemical, Petroleum and Plastic sectors led shares higher. Chinese and Australian stocks closed the week low as a result of the COVID-19 lock down in the major provinces with the manufacturing stocks being hit the hardest.

On the global commodities markets, Crude Oil WTI closed the week higher by 3.81% and the ICE Brent Crude increased by 3.16%. Gold futures prices increased by 0.01% to settle at $1,815.5.

Week’s Highlights

- The Energy and Petroleum Regulatory Authority (EPRA) issued a statement on the prices of fuel for the next 30 days where it said the prices will remain unchanged with petrol, diesel and kerosene standing at Ksh 159.12, Ksh 140 and Ksh 127.94 per litre. The state will pay oil marketers an estimated Ksh 24 billion to keep the pump prices unchanged easing public anger over the rising cost of living.

- Kenyans will have to dive deeper into their pockets as the cost of flour is set to shoot up with the subsidy program expected to end next week. The program was started to cushion consumers from the heavy prices up from Ksh 210 to Ksh 100 for a two kilogram of flour.

- Savings and Credit Cooperatives (SACCOs) topped banks by offering more competitive interest rates to members compared to the banks. According to the Sacco Societies Regulatory Authority (SASRAS), SACCOs offered between 6.83 percent in the year ended December and paid a range of between 5.63 percent and 8.26 percent on savings account while banks on the other hand paid an interest rate of 4.02 percent.

- The number of banks selling insurance products declined by 70 percent to eight lenders down from twenty seven in 2021 following regulatory reforms in the sector. The sharp decline being attributed to the introduction of new rules requiring bancassurrance companies to increase minimum capital to Ksh 5 million which is higher than what is required of brokers Ksh 1 million and also the raised registration fees from Ksh 1000 to Ksh 20,000. The firms are also required to provide a Ksh 10 million bank guarantee of government bond.

- Tanzania is set to sell its first bond seeking Tsh 130 billion ($55.6 million) from a 5-year fixed rate bond to its citizens and members from the East and Southern African trade blocs. The 5 year paper will be auctioned by the bank of Tanzania at a coupon rate of 8.6%.

- Money held by the Kenya Depository Insurance Corporation (KDIC) rose by 23 percent to Ksh 155 billion in the year ended December 2021 enhancing its capacity to compensate customers by providing a safety net to deposits by protecting them against the loss of all their funds in case of a bank collapse. According to the latest industry supervision report, total deposits in the banking sector rose by 11 percent from Ksh 4 trillion in 2020 to 4.5 trillion in 2021 due to deposit mobilisation through agency banking and mobile phone platforms with 99 percent of bank accounts fully insured.

- Egypt’s inflation increased to 13.6% in July from 13.2% in June as rising food prices and fuel costs added more pressure to consumers. Rwanda’s Central Bank hiked interest rate to 6% as inflation soared with annual urban inflation rising to 15.6% in July. Spain’s inflation rose to 10.8% in July largely driven by the rising cost of food, non-alcoholic beverages and electricity, this being the highest level since 1984. UK’s GDP shrank in Q2 2022 to 0.1% from 0.8% in Q1 2022 attributed to a decline in spending by households.

Get future reports

Please provide your details below to get future reports: