Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 7,067 million (3.80 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, Sterling Pound and Euro to exchange at KES 146.79, KES 182.38 and KES 156.58 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | 18.93% | 0.45% |

| Sterling Pound | 22.63% | 0.12% |

| Euro | 18.93% | 0.12% |

Liquidity

Liquidity in the money markets marginally increased, with the average interbank rate decreasing from 12.39% to 11.97%, as government payments more than offset tax remittances. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 12.39% | 11.97% |

| Interbank volume (billion) | 50.01 | 22.27 |

| Commercial banks’ excess reserves (billion) | 11.30 | 11.20 |

Fixed Income

T-Bills

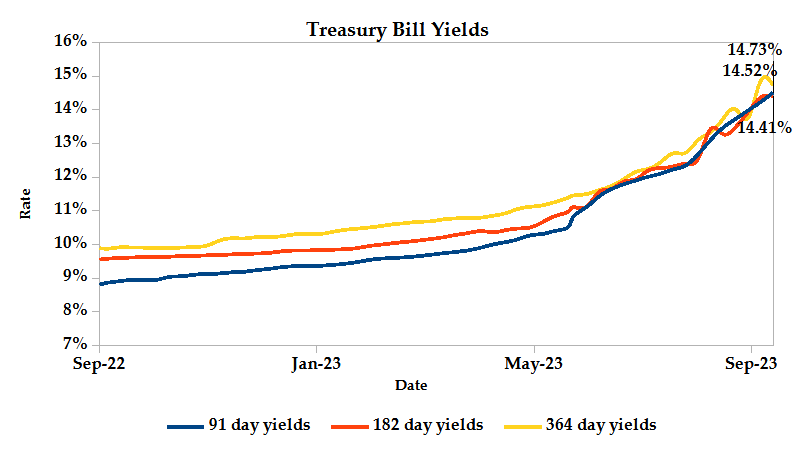

T-Bills were under-subscribed during the week, with the overall subscription rate recorded as 92.11%, down from 161.83% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 450.01% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 6.99% and 34.07% respectively. The acceptance rate decreased by 11.51% to close the week at 95.66%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 16.70% from KES 14.08 billion in the previous week to KES 16.44 billion. Total bond deals increased by 21.04% from 423 in the previous week to 512.

In the primary bond market, CBK released auction results for the reopened FXD1/2023/002 and FXD1/2016/010 through a tap sale which sought to raise KES 35.0 billion. The issues received bids worth KES 34.01 billion, representing a subscription rate of 97.17%. Of these, KES 21.63 billion worth of bids were accepted at a weighted average rate of 17.45% and 17.93% respectively.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average 0.18% compared to the previous week, increased by 0.07% month to date and 1.01% year to date. The yields on the 10-year Eurobonds for Ghana and Angola also declined.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 0.65% | -0.26% | -1.10% |

| 2018 10-Year Issue | 1.35% | 0.11% | -0.03% |

| 2018 30-Year Issue | 0.61% | 0.10% | 0.02% |

| 2019 7-Year Issue | 1.43% | 0.31% | 0.04% |

| 2019 12-Year Issue | 0.76% | 0.07% | -0.02% |

| 2021 13-Year Issue | 1.26% | 0.12% | 0.01% |

Equities

NASI settled 0.23% higher while NSE 25 and NSE 20 settled 0.16% and 0.71% lower compared to the previous week bringing the year-to-date performance to -22.31%, -18.91% and -8.63% respectively. Market capitalization gained 0.24% from the previous week to close at KES 1.55 trillion, recording a year-to-date decline of 22.10%. The performance was driven by gains recorded by large-cap stocks such as Safaricom and Co-operative of 1.61% and 1.27%. These were however weighed down by losses recorded by NCBA and KCB of 6.50% and 4.50% respectively.

The Banking sector had shares worth KES 487M transacted which accounted for 43.91% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 15.3M transacted which represented 1.39% and Safaricom, with shares worth KES 569M transacted represented 51.33% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| EA Portland | 8.82% | 18.97% |

| TR Serena | 9.62% | 16.80% |

| Longhorn | -15.00% | 15.91% |

| Jubilee | 0.38% | 13.51% |

| Express | 1.51% | 12.98% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| FAHARI I-REIT | 15.04% | -16.67% |

| Standard Group | -24.21% | -8.97% |

| Crown Paint | -11.33% | -8.00% |

| Liberty | -26.39% | -7.25% |

| NCBA | -3.98% | -6.50% |

Alternative Investments

| Losers | Week (previous) | Week (ending) | % Change |

|---|---|---|---|

| Derivatives Turnover (million) | 1.41 | 0.78 | -44.61% |

| Derivatives Contracts | 37.00 | 26.00 | -29.73% |

| I-REIT Turnover (million) | 0.59 | 0.38 | -34.23% |

| I-REIT deals | 49 | 41 | -16.33% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 16.37% | -0.16% |

| Dow Jones Industrial Average (DJI) | 4.48% | 0.12% |

| FTSE 100 (FTSE) | 2.08% | 3.12% |

| STOXX Europe 600 | 6.39% | 1.60% |

| Shanghai Composite (SSEC) | 0.04% | 0.03% |

| MSCI Emerging Markets Index | 2.33% | 1.14% |

| MSCI World Index | 13.84% | 0.41% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -17.62% | -15.75% |

| JSE All Share | 0.98% | 1.48% |

| NSE All Share (NGSE) | 30.62% | -1.10% |

| DSEI (Tanzania) | -5.38% | -0.03% |

| ALSIUG (Uganda) | -22.23% | -0.91% |

The US stock market was volatile during the week, primarily due to uncertainty about the Federal Reserve’s plans to raise interest rates more quickly than anticipated in an effort to combat inflation. Increased oil prices on the back of more stimulus measures, and economic data released during the last session, including the retail sales report, showed a resilient consumer spending, that further improved investor sentiment.

European stock markets closed the week on a positive note, as investors found comfort in indications that the European Central Bank (ECB) is nearly done raising interest rates. The ECB increased its benchmark interest rate to a record high of 4% while indicating that this would likely be the last increase. Better-than-expected Chinese statistics also helped luxury companies and boosted investor sentiment. Data revealed that China’s manufacturing output and retail sales increased more quickly in August, which is a reprieve to the global economy.

Asia Pacific indices ended the week on an upward trajectory, as investors bet that the US Fed will not hike interest rates as aggressively as expected. In addition, In Japan, investors’ sentiment has shifted towards stocks, with fear that the Bank of Japan will need to continue maintaining negative interest rates for the foreseeable future.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 3.73% and 3.62% higher at $90.77 and $93.93 respectively. Gold futures prices settled 0.18% higher at $1946.20.

Week’s Highlights

- The Energy and Petroleum Regulatory Authority (EPRA) released its latest monthly statement on the maximum retail prices of petroleum products, effective from 15th September 2023 to 14th October 2023. The pump price of Super Petrol has increased by KES 16.96 to KES 211.64 per litre, Diesel by KES 21.32 to KES 200.99 per litre and Kerosene by KES 33.13 to KES 202.61 per litre. This continues to pile pressure on households that are grappling with the high cost of living.

- The government launched a new central securities depository infrastructure, DhowCSD, which provides world-class levels of registry, custodial, and settlement services for both primary and secondary market operations. The DhowCSD is transforming Kenya’s financial markets by making them more efficient, transparent and accessible, thus making it easier for investors to participate in them. This will enhance participation in the Kenyan capital market.

- OPEC expects global oil demand to increase by 2.4 million barrels per day in 2023 and 2.2 million barrels per day in 2024. The non-OECD region, particularly China, India, and the Middle East, is anticipated to be the main driver of this expansion. While both groups are anticipated to produce more oil in 2024, the increase in the non-OPEC liquids supply is expected to be a relatively higher in 2023 than the growth of the OPEC liquids supply. August saw an increase in OPEC crude oil production and disruptions in production of the same poses a threat of slowdown in the world economy.

- US inflation rose 0.6% in August 2023, in line with market expectations. This was the largest monthly increase since March. The gasoline index, which reported a 10.6% increase compared to a 0.2% increase in July, was responsible for more than half of the increase. All the major energy component indices climbed, causing the overall energy index to rise by 5.6%. The shelter index, which increased for the 40th consecutive month, continued to rise and was another factor in the increase.

- The Bank of England increased its benchmark interest rate by 25 basis points to 5.25% in August 2023, the 14th consecutive hike. This brought borrowing costs to their highest level since 2008, as the central bank continues to curb high inflation. The Monetary Policy Committee approved the quarter-point rise by a vote of 6-3, with two members favouring a second consecutive 50 bps increase and one opting to keep the rates steady. The current monetary policy stance, according to policymakers, is constrictive given the large rise in interest rates since the start of the tightening cycle. However, they stated that they will keep rates high for as long as necessary to bring inflation back to its 2% target in the medium term. The central bank anticipates inflation to return to the 2% target by Q2 2025 and decrease further this year, to roughly 5% by year’s end, which is a faster decline than it had predicted in May.

- The British economy contracted by 0.5% month on month in July 2023, marking the year’s largest monthly decline and reversing a 0.5% monthly rise in June. The results were worse than the 0.2% decline prediction fueled by the services sector, which fell by 0.5% compared to 0.2% in June. The human health activities business had the biggest decline, falling by 3.4%, as appointments and operations were cancelled due to strikes in the National Health Service. Computer programming, consulting, and related activities also fell by 3.4%. In contrast, output in consumer-facing services showed no growth, with retail trade making the biggest contribution to the decline of -1.2%. Production decreased by 0.7%, while manufacturing shrank by 0.8%, driven mostly by the production of rubber and plastic products. The construction industry saw a 0.5% decline, production decreased by 0.7%, while manufacturing shrank by 0.8%. In the three months leading up to July, the GDP however, increased by 0.2%.

Get future reports

Please provide your details below to get future reports: