Foreign Exchange Reserves

The usable foreign exchange reserves stood at at USD 6,875 million (3.84 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar but strengthened against the Sterling Pound and the Euro to exchange at KES 125.63, KES 151.12 and KES 134.35 respectively. The observed depreciation against the Dollar is attributed to increased demand from importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 1.78% | 0.44% |

| Sterling Pound | 1.69% | -0.62% |

| Euro | 2.04% | -0.28% |

Liquidity

Liquidity in the money markets slightly increased with the average interbank rate dropping from 6.46% to 6.23%, supported by government payments which offset tax remittances. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.46% | 6.23% |

| Interbank volume (billion) | 16.05 | 22.05 |

| Commercial banks’ excess reserves (billion) | 12.40 | 16.10 |

Fixed Income

T-Bills

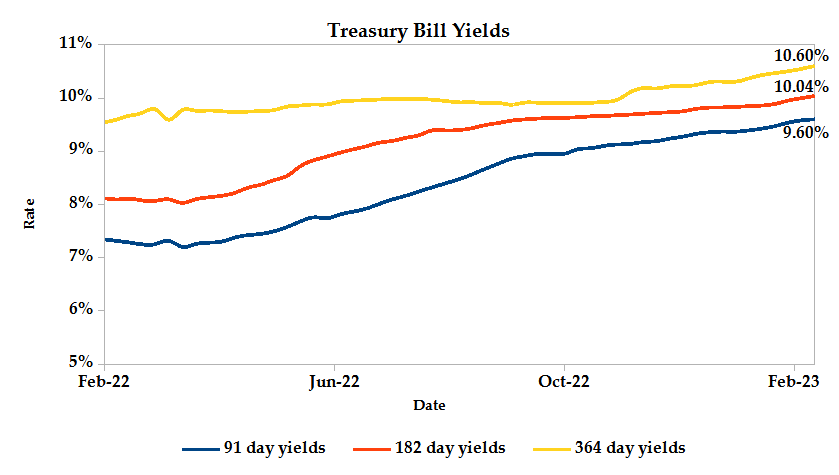

T-Bills remained oversubscribed this week, with the overall subscription rate increasing to 191.31%, from 187.09% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 552.22% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 175.27% and 62.98% respectively. The acceptance rate increased by 7.62% to close the week at 97.40%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 29.55% from KES 10.00 billion in the previous week to KES 12.95 billion. Total bond deals declined by 10.55% from 578 in the previous week to 517.

In the primary market, CBK released auction results for the reopened FXD1/2017/010 and the newly issued FXD1/2023/010 which sought to raise KES 10.0 billion. The issues received bids worth KES 12.46 billion, representing a subscription rate of 124.63%. KES 12.20 billion worth of bids were accepted at a weighted average rate of 13.88% for the tap sale on the reopened paper and 14.15% for the new issue.

Additionally, Central Bank issued a new 17-year amortized infrastructure bond; IFB1/2023/017 seeking KES 50.0 billion. The coupon rate is set to be market determined with the period of sale running from 15th February to 7th March 2023.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average 0.36% compared to the previous week, 0.33% month to date and declined 0.21% year to date. The yields on the 10-Year Eurobonds for Ghana and Angola also increased . Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | -1.20% | 0.47% | 0.92% |

| 2018 10-Year Issue | 0.04% | 0.34% | -0.34% |

| 2018 30-Year Issue | -0.07% | 0.20% | 0.32% |

| 2019 7-Year Issue | -0.11% | 0.35% | 0.57% |

| 2019 12-Year Issue | -0.15% | 0.31% | 0.41% |

| 2021 13-Year Issue | 0.22% | 0.29% | 0.31% |

Equities

NASI dropped 0.18% while NSE 20 and NSE 25 edged 0.52% and 0.23% higher compared to the previous week bringing the year to date performance to 0.53%, 0.30% and 1.65% respectively. Market capitalization settled 0.18% lower from the previous week, closing at KES 1.99 trillion and recording a year to date gain of 0.53%. The performance was driven by gains recorded by large-cap stocks such as Standard Chartered and Equity of 2.06% and 1.75%. These were however weighed down by losses recorded by Safaricom and KCB of 1.05% and 0.52% respectively.

The Banking sector had shares worth KES 563M transacted which accounted for 42.71% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 244M transacted which represented 18.53% and Safaricom, with shares worth KES 486.7M transacted represented 36.91% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Flame Tree | 8.18% | 19.00% |

| BAT | 4.29% | 7.81% |

| NBV | -3.81% | 5.28% |

| Nation Media | -1.90% | 4.73% |

| I&M | 5.57% | 4.35% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Unga | -31.72% | -15.96% |

| Kengen | -17.08% | -6.32% |

| Home Afrika | -11.76% | -6.25% |

| Express | -2.59% | -6.04% |

| Limuru Tea | -4.76% | -4.76% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.82 | 0.56 | -31.32% |

| Derivatives Contracts | 15 | 12 | -20.00% |

| I-REIT Turnover (million) | 1.48 | 0.39 | -73.83% |

| I-REIT deals | 113 | 56 | -50.44% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 5.92% | -0.98% |

| Dow Jones Industrial Average (DJI) | 1.46% | -0.75% |

| FTSE 100 (FTSE) | 5.92% | 1.51% |

| STOXX Europe 600 | 6.94% | 1.40% |

| Shanghai Composite (SSEC) | 3.45% | -1.12% |

| MSCI Emerging Markets Index | 5.05% | -0.25% |

| MSCI World Index | 7.29% | 0.24% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 0.71% | -0.87% |

| JSE All Share | 7.13% | 0.29% |

| NSE All Share (NGSE) | 4.28% | -0.96% |

| DSEI(Tanzania) | 2.68% | 0.40% |

| ALSIUG (Uganda) | -0.16% | 0.17% |

US indices closed the week lower, with S&P 500, Dow Jones and Nasdaq 0.25%, 0.23% and 0.5% respectively. Big Techs such as Alphabet, Microsoft, Facebook, and Apple have all dropped more than 1%. This loss is the result of growing concerns that the Federal Reserve will raise interest rates more aggressively than expected, despite recent economic data indicating elevated inflation, a tight labor market, and consumer spending resilience.

European shares rose as upbeat corporate earnings helped France’s blue-chip index reach a new high, overshadowing concerns about US interest rates remaining high. European banks rose 2.1% to lead gains among STOXX 600 sectors, while industrials also contributed significantly to the index.

The Asian stock market fell, with the technology sector among the worst performers. The Hang Seng index in Hong Kong, the KOSPI in South Korea, and the Taiwan Weighted index all fell between 0.4% and 0.8% as more hawkish signals from the Federal Reserve fueled fears that interest rates would continue to rise. Furthermore, recent Chinese economic indicators revealed that certain aspects of the country were still struggling to recover from the Covid-19 pandemic’s impact.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 8.95% and 8.07% higher at $79.75 and $86.39 respectively. Gold futures prices settled 0.01% lower at $1,862.80.

Week’s Highlights

- As part of the government’s plan to improve the exchequer’s chances of fiscal consolidation, the National Treasury will now cap expenditure growth at 75% of Kenya’s revenue growth rate. The Ministry of Planning will also limit revenue growth projections in order to avoid overly ambitious tax targets, which have plagued previous budgets when not met, resulting in larger fiscal deficits.

- According to an EPRA press release on the maximum retail prices for the period 15th February 2023 to 14th March 2023, the price of Diesel has been cross-subsidized with Super Petrol, while a subsidy of KES 19.41/litre has been maintained for Kerosene to cushion customers from the otherwise high prices. The government is expected to use the Petroleum Development Levy to compensate oil marketers for the cost difference.

- The Kenya Revenue Authority (KRA) reported KES 152.14 billion in tax revenue collection in January, making it the third highest-earning month in the fiscal year 2022/23. According to a gazette notice, tax revenue amounted to KES 1.1 trillion in the first half of fiscal year 2022/23, accounting for 53.3% of the full-year target of KES 2 trillion. This accomplishment is attributed to ongoing tax policies and revenue administration reforms.

- Acorn Holdings, a student hostel developer, intends to launch a new real estate investment trust (Reit) to develop apartments for young urban professionals. The company, which raised Sh2.1 billion from investors in its debut Reit in 2021 with a target of Sh7.5 billion, now says it will return to the market for another issuance as it continues to fund projects with a mix of debt and equity. According to Acorn’s CEO, Edward Kirathe, the property developer could list the Reit within the next 12 to 18 months, depending on the timing of approval from the Capital Markets Authority (CMA).

- According to OPEC’s most recent monthly oil market report, oil demand will increase by 2.32 million barrels per day (bpd) in 2023 to 101.87 million bpd, with some minor upward adjustments due to China’s expected better performance following its reopening from Covid-19 restrictions.

- The IMF and the Ukrainian authorities have reached an agreement at the staff level on the first and final reviews under the Program Monitoring with Board Involvement (PMB). This agreement, which is subject to IMF Management approval, clears the way for discussions to begin on a full-fledged Fund-supported program. This agreement would help Kyiv’s economy and its bid to join the European Union.

- In February, China kept its benchmark lending rates unchanged for the sixth consecutive month. The one-year loan prime rate (LPR) remained at 3.65%, while the five-year LPR remained at 4.30%. New bank loans in China increased more than expected to a record 4.9 trillion yuan in January as the central bank seeks to kick-start recovery, while new home prices rose for the first time in a year as Beijing increased support for the property sector, which accounts for a quarter of the domestic economy.

Get future reports

Please provide your details below to get future reports: