Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 6,560 million (3.66 months of import cover). This falls short of CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Sterling Pound and the Euro to exchange at KES 129.88, KES 156.51 and KES 137.77 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 5.23% | 0.77% |

| Sterling Pound | 5.23% | 2.23% |

| Euro | 4.64% | 1.23% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate increasing to 6.97% from 6.59%, as tax remittances more than offset government payments. Remittance inflows totaled $309.20 million in February 2023, an 11.51% decline from $349.40 in January 2023 and a 3.84% decline from $321.53 in February 2022. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.59% | 6.97% |

| Interbank volume (billion) | 31.17 | 29.07 |

| Commercial banks’ excess reserves (billion) | 14.90 | 2.70 |

Fixed Income

T-Bills

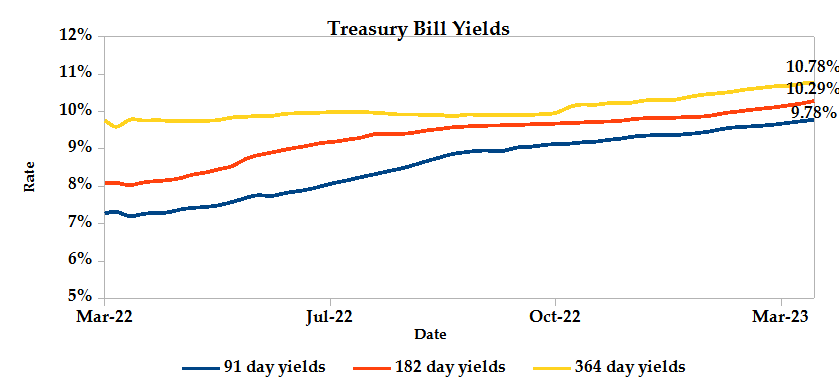

T-Bills remained over-subscribed during the week, with the overall subscription rate recorded as 121.63%, down from 148.47% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 182.28% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 174.66% and 44.33% respectively. The acceptance rate increased by 9.16% to close the week at 98.61%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 119.74% from KES 8.40 billion in the previous week to KES 18.45 billion. Total bond deals increased by 133.92% from 401 in the previous week to 938.

In the primary bond market, CBK reopened the 17-year amortized infrastructure bond; IFB1/2023/017, through a tap sale which sought to raise KES 20 billion. The issue had a performance rate of 63.56%, receiving bids worth KES 12.71 billion. Of these, KES 12.71 billion worth of bids were accepted at an average yield of 14.40% that was determined in the first auction.

In addition, CBK reopened three bonds. The first bond; FXD2/2018/10, seeks to raise KES 20.0 billion and has a tenor of 5.8 years with a coupon rate of 12.50%. The period of sale for this issue runs from 16th March 2023 to 4th April 2023. The other two bonds; FXD1/2022/03 & FXD1/2019/15 seek to raise KES 30.0 billion with effective tenors 2.1 and 10.9 years and coupon rates of 11.77% and 12.86% respectively. The period of sale for these issues will run from 16th March 2023 to 18th April 2023.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average 1.56% compared to the previous week, 2.34% month to date and 1.80% year to date. The yields on the 10-Year Eurobonds for Ghana and Angola also increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 1.07% | 2.75% | 2.16% |

| 2018 10-Year Issue | 2.36% | 2.66% | 1.63% |

| 2018 30-Year Issue | 1.39% | 1.66% | 0.96% |

| 2019 7-Year Issue | 2.51% | 2.97% | 2.36% |

| 2019 12-Year Issue | 1.71% | 2.18% | 1.16% |

| 2021 13-Year Issue | 1.73% | 1.80% | 1.07% |

Equities

NASI, NSE 20 and NSE 25 settled 12.28%, 4.87% and 9.71% lower compared to the previous week bringing the year to date performance to -18.79%, -8.67% and -13.76% respectively. Market capitalization lost 12.31% from the previous week to close at KES 1.61 trillion recording a year to date decline of 18.84%. The performance was driven by losses recorded by large-cap stocks such as Safaricom, KCB, Equity, NCBA and ABSA of 20.63%, 17.22%, 11.28%, 7.47% and 4.38% respectively. These were however mitigated by the gains recorded by Stanbic and EABL of 1.61% and 0.44% respectively.

The Banking sector had shares worth KES 431M transacted which accounted for 14.74% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 71M transacted which represented 2.44% and Safaricom, with shares worth KES 2.3B transacted represented 81.42% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Olympia | -9.46% | 8.50% |

| Liberty | -4.76% | 6.43% |

| Kenya Power | -10.49% | 5.07% |

| Standard Group | -10.05% | 4.44% |

| FAHARI I-REIT | -7.37% | 3.63% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Safaricom | -32.02% | -20.63% |

| Unga | -48.13% | -17.62% |

| KCB | -19.17% | -17.22% |

| Jubilee | -23.77% | -13.80% |

| Equity | -15.32% | -11.28% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.26 | 9.01 | 616.16% |

| Derivatives Contracts | 23 | 45 | 95.65% |

| I-REIT Turnover (million) | 0.42 | 0.35 | -15.21% |

| I-REIT deals | 52 | 50 | -3.85% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 2.42% | 1.43% |

| Dow Jones Industrial Average (DJI) | -3.85% | -0.16% |

| FTSE 100 (FTSE) | -2.89% | -5.33% |

| STOXX Europe 600 | 0.49% | -3.89% |

| Shanghai Composite (SSEC) | 4.30% | 0.63% |

| MSCI Emerging Markets Index | -1.14% | -0.39% |

| MSCI World Index | 2.13% | -0.05% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -4.82% | -3.30% |

| JSE All Share | -1.99% | -5.22% |

| NSE All Share (NGSE) | 6.47% | -1.54% |

| DSEI (Tanzania) | -1.91% | -2.05% |

| ALSIUG (Uganda) | -5.14% | -1.51% |

US indices ended the week mixed, due to concerns over a potential banking crisis which began with the collapse of Silicon Valley Bank, despite the massive rescue package for the banking sector. Global equities were under pressure and gold prices rallied, while US Treasury yields fell and oil prices hit 15-month lows. Consumer sentiment in the US also fell for the first time in four months.

European stock markets ended the week lower, with banks leading the decline, amidst growing concerns over a banking crisis in the US and uncertainty around monetary policy. Investors remain cautious as they monitor developments in the banking sector and look for signs of a clearer path forward in the months ahead.

Asian stock markets closed the week on a positive note, recovering from sharp losses earlier in the week as a result of the troubled Swiss lender Credit Suisse Group AG receiving a credit facility of up to $54 billion from the Swiss National Bank, while US officials also intervened to protect depositors. This government and institutional support to avert a banking crisis boosted market sentiment. Traders also factored in a less hawkish stance from the Federal Reserve, which helped boost the markets more further.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 12.96% and 11.85% lower at $66.74 and $72.97 respectively. Gold futures prices settled 5.69% higher at $1,973.50.

Week’s Highlights

- The Energy and Petroleum Regulatory Authority (EPRA) released the monthly statement on maximum retail prices of petroleum products which will be in force from 15th March 2023 to 14th April 2023. The pump price of Super Petrol increased by KES 2.00 to KES 179.30 per litre while that of Diesel and Kerosene remained unchanged at KES 162.00 per litre and KES 145.94 per litre respectively. The subsidy of Kerosene has been maintained at KES 23.49 per litre while the price of Diesel has been cross-subsidized with that of Super Petrol.

- The World Bank has increased Kenya’s loan kitty by KES 32.3 billion ($250 million) to a total of KES 129 billion ($1 billion) through its Development Policy Operations (DPO) facility. This funding will help to address Kenya’s budget deficit in the 2022/23 fiscal year and provide much-needed resources. The loan will also offer significant relief at a time when interest rates for loans in dollars are relatively high and Kenya’s foreign exchange reserves have been decreasing.

- The National Treasury gazetted the actual revenues and expenditure for the 8 months of the financial year 2022/23 ending 28th February. Total revenue collected during the month amounted KES 1.28 trillion, accounting for 59.80% of the original KES 2.14 trillion estimates for the FY2022/23. The figure lies below the KES 1.43 trillion prorated amount expected for the first eight months of the year. Total expenditure amounted KES 1.83 trillion, translating to 51.60% of the original estimates. The deficit was plugged by a total KES 549.81 billion in financing.

- The Kenya Revenue Authority (KRA) is requesting a KES 12 billion budget allocation for the fiscal year to support its technology-driven revenue mobilization plan; e-TIMS. The allocation is subject to approval in the 2023 Budget Policy Statement. If approved, KRA’s request will raise the National Treasury’s budget ceiling from KES 130 billion as stated in the draft budget. This funding will be crucial for the success of KRA’s e-TIMS plan.

- Kenya’s currency continues to face pressure as the shortage of US dollars drives up the price of buying the currency to a record high of KES 145 per unit, leading to a wide spread between the official and open market rates, creating a black market for the currency. Local oil companies have turned to paying for imported oil in Kenyan shillings to ease the pressure. The upcoming dividend season for blue-chip companies with foreign ownership, such as Safaricom and Standard Chartered, is expected to exacerbate the shortage, as they seek hundreds of millions of dollars for payment to offshore investors, further straining the forex market.

- The European Central Bank (ECB) has increased interest rates by 0.5%, further pushing borrowing costs to the highest level since late 2008, in order to help mitigate the region’s persistently high inflation. The main refinancing operations, as well as the marginal lending facility and the deposit facility interest rates, were all raised to 3.50%, 3.75% and 3.00%, respectively. According to the ECB, inflation is expected to average 5.3% in 2023, 2.9% in 2024, and 2.1% in 2025. At the same time, underlying price pressures are anticipated to remain high, with core inflation expected to average 4.6% in 2023, a higher forecast from what was projected in December.

- US inflation fell to 6% in February 2023, the lowest level since September 2021, which is consistent with market expectations and down from 6.4% in January. Food prices increased but at a slower rate of 9.5% compared to the previous 10.1%, while used car and truck prices continued to drop. In addition, the cost of energy and fuel oil sharply declined, with gasoline prices falling 2% after rising 1.5% in January. Core inflation, which excludes food and energy prices, edged lower on a year to year basis from 5.6% to 5.5%. This core inflation rate, however, rose to 0.5% on a monthly basis, exceeding the 0.4% estimate. Inflation in the US remains three times above the Fed’s target of 2%.

Get future reports

Please provide your details below to get future reports: