Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,191 million (4.03 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover. However, it does not meet EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Euro and the Sterling Pound to exchange at KES 122.03, KES 126.31 and KES 144.84 respectively. The observed depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 7.86% | 0.20% |

| Euro | -1.39% | 3.37% |

| Sterling Pound | -4.92% | 3.51% |

Liquidity

Liquidity in the money markets tightened with the average interbank rate rising from 3.84% to 4.37%, as tax remittances more than offset government payments. Remittance inflows totaled USD 332.6 million in October 2022, a 4.59% increase from USD 318.0 in September and a 1.42% drop from USD 337.4 million in October 2021. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 3.84% | 4.37% |

| Interbank volume (billion) | 12.30 | 28.99 |

| Commercial banks’ excess reserves (billion) | 28.80 | 5.70 |

Fixed Income

T-Bills

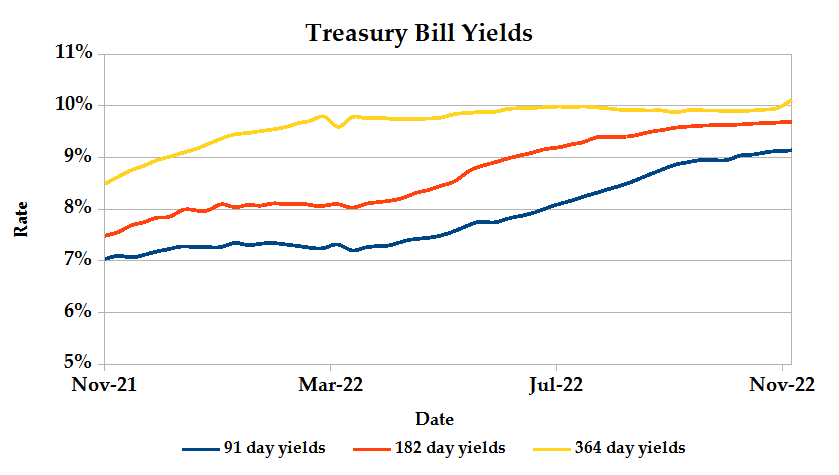

T-Bills remained over-subscribed during the week with a decline in the overall subscription rate from 204.53% recorded in the previous week to 170.84%. The 91-day T-Bill received the highest subscription rate at 406.30% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 158.03% and 89.46% respectively. The acceptance rate dropped by 6.04% to close the week at 73.38%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 13.15% from KES 12.81B in the previous week to KES 14.50B. Total bond deals increased by 125.45% from 334 in the previous week to 753.

In the primary bond market, CBK reopened the 14-year infrastructure bond, IFB1/2022/14 whose initial auction closed last week, seeking to raise KES 5.0 billion. The tap sale is expected to run from 16th to 22nd November 2022, with bids priced at the average accepted rate of 13.94%

Eurobonds

In the international market, yields on Kenya’s Eurobonds declined by an average 0.94% compared to the previous week, 3.35% month to date and increased 4.36% year to date. The yields on the 10-year Eurobond for Ghana and Angola also declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 7.05% | -4.25% | -1.34% |

| 2018 10-Year Issue | 4.38% | -3.53% | -1.35% |

| 2018 30-Year Issue | 2.81% | -2.30% | -0.73% |

| 2019 7-Year Issue | 4.87% | -3.89% | -0.79% |

| 2019 12-Year Issue | 3.89% | -3.43% | -1.04% |

| 2021 12-Year Issue | 3.14% | -2.72% | -0.41% |

Equities

NASI and NSE 25 edged up by 0.73% and 1.35% respectively while NSE 20 lost 0.10% compared to the previous week bringing the year to date performance to -22.79%, -16.68% and -13.03% respectively. Market capitalization gained by 0.73% from the previous week to close at KES 2.01 trillion recording a year to date decline of 22.77%. The performance was driven by gains recorded by large-cap stocks such as KCB, EABL and Equity of 5.58%, 4.92% and 3.77% respectively. These were however weighed down by losses recorded by NCBA, Stanbic and Diamond Trust of 3.47%, 2.50% and 2.27% respectively.

The Banking sector had shares worth KES 337M transacted which accounted for 17.25% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 353M transacted which represented 18.04% and Safaricom, with shares worth KES 1.2B transacted represented 63.57% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| NBV | -32.22% | 11.92% |

| Flame Tree | -8.00% | 7.48% |

| KCB | -14.82% | 5.58% |

| EABL | -0.15% | 4.92% |

| Eaagads | -14.81% | 4.55% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| Jubilee | -40.73% | -10.60% |

| Sameer | -15.79% | -10.45% |

| Trans-Century | -10.83% | -10.08% |

| BOC Kenya | 2.86% | -10.00% |

| Kapchorua | 5.53% | -8.70% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.58 | 1.38 | -12.42% |

| Derivatives Contracts | 30 | 30 | 0.00% |

| I-REIT Turnover | 0.19 | 0.12 | -36.90% |

| I-REIT Deals | 36 | 28 | -22.22% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -17.33% | -0.69% |

| Dow Jones Industrial Average (DJI) | -7.76% | -0.01% |

| FTSE 100 (FTSE) | -1.59% | 0.92% |

| STOXX Europe 600 | -11.57% | 0.25% |

| Shanghai Composite (SSEC) | -14.73% | 0.32% |

| MSCI Emerging Markets | -23.55% | 0.78% |

| MSCI World Index | -17.97% | -0.57% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -26.97% | 2.60% |

| JSE All Share | -1.19% | -0.34% |

| NSE All Share (NGSE) | 3.41% | 1.19% |

| DSEI (Tanzania) | -1.45% | 1.18% |

| ALSIUG (Uganda) | -13.22% | 2.07% |

US indices slumped compared to the previous week, with S&P 500 edging up 0.48% on Friday driven by gains in defensive sectors such as utilities, real estate and healthcare. These were however overshadowed by energy stock declines of 0.9% as oil prices dropped.

European stocks recorded week on week gains, reflecting improved consumer confidence as reported by GfK’s Autumn Statement and rallied by retailers and automakers. These were weighed down by energy stocks reflecting falling oil prices driven by fears of weaker demand in China and ongoing Covid restrictions.

Asia Pacific stocks ended the week slightly positive amid investor optimism over the easing of Covid-19 restrictions. Japan’s Nikkei 25 index closed Friday 1.29% lower week on week following consumer inflation reading that indicated a 40-year surge in October to 3.6%. This, coupled with weakening economic growth fed investor speculation of tightened policies in Bank of Japan’s December meeting.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 9.74% and 8.33% lower respectively. Gold futures prices settled 1.23% lower at $1,751.30.

Week’s Highlights

- The Energy and Petroleum Regulatory Authority (EPRA) released their monthly statement on the maximum retail prices of petroleum products which will be in force from 15th November to 14th December 2022. These are KES 177.30 per litre for Super Petrol, KES 162.00 per litre for Diesel and KES 145.94 per litre for Kerosene, all trimmed by KES 1 per litre from their previous prices. The subsidy on Kerosene has been maintained at KES 17.68 per litre while the price of Diesel has been cross-subsidized with that of Super Petrol.

- The National Treasury, in its Quarterly Economic and Budgetary Review Report for the period ending 30th September 2022, revealed that total government expenditure amounted to KES 759.5 billion, exceeding its KES 694.0 billion target by KES 65.5 billion. This widens the budget deficit expected to be covered by borrowing, with net domestic borrowing already missing its KES 175.5 billion target, amounting to KES 101.6 billion.

- CMA granted approval to TransCentury Plc to undertake a rights issue on the basis of five new ordinary shares for every one existing share, to raise KES 2.06 billion by offering 1,876,013,830 new ordinary shares at a discounted price of KES 1.10 per share. The funds raised will be used to settle debt and unlock working capital, restructure the business to accelerate return to profitability and increase shareholder value.

- The African Exchanges Linkage Project (AELP), set to integrate African capital markets by facilitating cross-border trading, went live. The infrastructure harmonization is expected to ease trading of exchange-listed securities across 7 stock exchanges, which represent about 85% of Africa’s securities market capitalization. These include Nairobi Stock Exchange (NSE), Stock Exchange of Mauritius (SEM), Johannesburg Stock Exchange (JSE), Nigerian Stock Exchange Limited (NGX) among others. AELP is designed to link exchange and broker trading systems as well as aggregate market data, providing clarity of market depth and liquidity from a local and foreign investor position.

- The Organization of Petroleum Exporting Countries (OPEC) released its Monthly Oil Market Report which highlighted that global oil demand growth forecast for 2022 stands at 2.5 million barrels per day (mb/d), while that of 2023 stands at 2.2 mb/d, a 0.1 mb/d downward revision for both periods. This is mainly attributed to the zero-Covid policy in China, ongoing geopolitical uncertainties and weaker economic activities. Main supply drivers are expected to be the US, Norway, Brazil, Canada, Kazakhstan and Guyana while oil production is expected to decline in Russia following looming EU sanctions on imports.

- UK Consumer Price Index (CPI) rose by 11.1% in October 2022, up from 10.1% in September, the highest annual CPI inflation rate since January 1997. The main drivers were housing and household services, food and non-alcoholic beverages and transport. Gas and electricity prices had the largest upward change despite the introduction of the government’s Energy Price Guarantee which fixed the unit cost of electricity and gas.

Get future reports

Please provide your details below to get future reports: