Foreign Exchange Reserves

The CBK’s usable foreign exchange reserves remained adequate at USD 7,448 million (4.24 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover. However, it does not meet EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar but gained against the Euro and the Sterling Pound to exchange at Ksh 120.56, Ksh 119.23 and Ksh 136.51 respectively. The observed overall depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 6.56% | 0.12% |

| Euro | -6.92% | -0.91% |

| Sterling Pound | -10.39% | -0.13% |

Liquidity

Liquidity in the money markets decreased, partly reflecting tax remittances which offset government payments. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 4.0% | 4.5% |

| Interbank volume (billion) | 27.3 | 24.1 |

| Commercial banks’ excess reserves (billion) | 20 | 12.3 |

Fixed Income

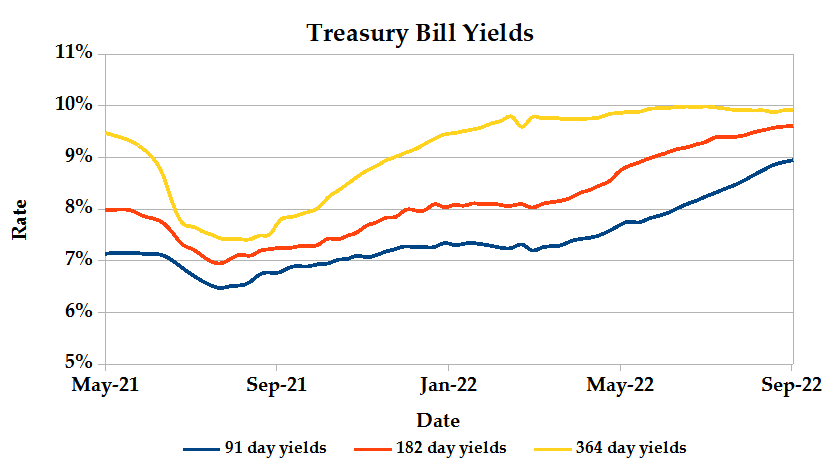

T-Bills

T-Bills remained under-subscribed during the week with a decrease in the overall subscription rate from 97.02% recorded in the previous week to 46.59%. The 91-day T-Bill got the highest subscription rate at 117.8% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 54.3% and 10.4% respectively. The acceptance rate decreased by 14.05% to close the week at 88.64%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bonds turnover increased by 84.76% from 7.5B in the previous week to 13.9B. Total bond deals increased by 82.03% from 345 in the previous week to 628. In the primary bond market, the treasury has issued a new bond FXD1/2022/025 and has reopened two papers: FXD1/2017/010 and FXD1/2020/15 as it targets to raise Kshs 60billion. There has been a low uptake of bonds both from local banks and foreign investors, given higher rates offered in the US that are considered a safe haven.

Eurobonds

In the international market, the yields on the 10-year Eurobonds for Angola and Ghana increased. Yields on Kenya’s Eurobonds generally increased by 0.47% compared to the previous week, -0.92% and 6.28% month to date and year to date respectively. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 8.38% | -2.45% | 0.83% |

| 2018 10-Year Issue | 6.81% | -0.72% | 0.39% |

| 2018 30-Year Issue | 4.03% | -0.38% | 0.28% |

| 2019 7-Year Issue | 7.54% | -1.40% | 0.38% |

| 2019 12-Year Issue | 6.10% | -0.40% | 0.41% |

| 2021 12-Year Issue | 4.83% | -0.17% | 0.55% |

Equities

NASI and NSE 25 increased by 1.90% and 1.21% respectively, while NSE 20 decreased by 0.10% compared to last week bringing the year to date performance to -19.29%, -8.79% and -15.01% respectively. The market capitalization also increased by 1.91% from the previous week to close at 2.10 trillion recording a year to date decline of -19.26%. The performance was driven by gains recorded by large-cap stocks. Top gains were recorded in Safaricom plc, Standard Chartered Bank and KCB group which gained by 3.20%, 1.10% and 0.26% respectively.

The Banking sector had shares worth Ksh 1.2B transacted which accounted for 48.55% of the week’s traded value, Manufacturing & Allied sector had shares worth Ksh 197M transacted which represented 7.94% and Safaricom, with shares worth Kshs 987M transacted represented 39.71% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Olympia Capital | 57.89% | 16.28% |

| EA Portland | 14.77% | 10.03% |

| BK Group | 5.69% | 9.86% |

| NCBA | 26.97% | 8.37% |

| Sasini | 27.81% | 8.14% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| TP Serena | -8.20% | -14.63% |

| Sanlam Kenya | 13.42% | -13.04% |

| Liberty Holdings | 10.76% | -10.00% |

| Eveready | -30.48% | -8.75% |

| Sameer | 10.88% | -8.41% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 6.34 | 4.75 | -25.11% |

| Derivatives Contracts | 38 | 43 | 13.16% |

| I-REIT Turnover | 0.49 | 0.42 | -14.67% |

| I-REIT Deals | 48 | 44 | -8.33% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | -23.00% | -4.65% |

| Dow Jones Industrial Average (DJI) | -19.11% | -3.99% |

| FTSE 100 (FTSE) | -6.48% | -3.01% |

| STOXX Europe 600 | -20.32% | -4.37% |

| Shanghai Composite (SSEC) | -14.98% | -1.22% |

| MSCI Emerging Markets | -23.20% | -2.70% |

| MSCI World Index | -20.74% | -3.11% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -25.05% | -0.21% |

| JSE All Share | -14.79% | -4.84% |

| NSE All Share (NGSE) | 13.95% | -0.91% |

| DSEI (Tanzania) | -2.03% | -0.76% |

| ALSIUG (Uganda) | -12.21% | -2.02% |

US stocks closed the week lower due to a decline in the Energy sector and Consumer stocks and further decline of the Dollar, which increased fears that a deeper global recession would hurt energy demand. The Federal Reserve’s chair also made remarks that the Federal Reserve was keen to curb inflation rather than promote economic growth.

European stocks closed the week lower as investors digested a series of interest rate hikes in the region, ahead of a fiscal update by the new UK administration. The Bank of England hiked its benchmark rate by 0.50%for the seventh consecutive time, which may further hurt the European equities market. The impact of Russia – Ukraine war on supply chain, food and fuel prices and continued tightening of the monetary policies by central banks continue to hinder growth and promote inflation.

Asia Pacific stocks closed the week lower due to losses from Technology stocks, as rising interest rates globally continue to destabilize economic growth and reduce investors’ risk appetite.

On the global commodities markets, Crude Oil WTI closed the week lower by 7.04% and the ICE Brent Crude decreased by 5.17%. Gold futures prices decreased by 1.90% to settle at $1,651.45.

Week’s Highlights

- Lending to the private sector declined towards the general elections period, due to subdued business activity. According to data from the central bank, credit growth stood at 12.5% from 14.2% recorded in July. More banks have been given an approval of risk-based pricing of loans, thus expected to boost lending towards the private sector.

- Commercial lenders to Kenya declined to 14% from 15.5% in the year to June 2022, indicating the difficulty in accessing international credit due to high lending rates. This has led to a decline in commercial loans from Kshs1.195 trillion to Kshs 1.181 trillion. The government has further increased domestic borrowing from Kshs 302.4 billion in June last year to Kshs2.3 billion in June 2022.

- The insurance industry is tapping into the climate risk sector, to develop products including covers against the climate change – related risk. This move will improve the growth of the under-performing insurance sector, which has fallen below 2.5% of the GDP according to Minet Insurance Brokers.

- Private Wealth Capital Limited (PWCL) has been admitted by the NSE, following the approval of the Capital Markets Authority, to act as an authorised securities dealer (ASD) for the listed fixed income securities. This is the first non-bank ASD in Kenya, which will also allow trading of offshore bonds, thus giving Kenyan retail investors an opportunity to carry out offshore bond trading in the Eurobond market. The Central Depository and Settlement Corporation (CDSC) on the other hand has appointed Family Bank as a central depository agent, with the mandate of listing new clients and maintaining CDS accounts in respect to the trades done at the NSE.

- Egypt is set to raise transit fees for vessels and tankers passing through the Suez Canal by 15% for tankers carrying oil and 10% for dry bulk carriers and cruise ships, effective as from January 2023. This was attributed to the current global inflation rates which have increased its operation costs.

- South Africa’s inflation slowed down to 7.6% in August compared to 7.8% in July, despite signals that that the benchmark rate would rise to 5.61% by the end of the year. This was fuelled by a decline in fuel prices which made the transport index to reduce by 1.0% during the same period under review.

- The Bank of England has raised its its base rate by 50 basis points to a 14 year high of 2.25%, which is lower than the expected raise of 75 basis points. UK’s inflation in August stood at 9.9% year on year due to increase in food and energy prices, and is expected to peak in October. However, government caps on energy would further curb inflation.

Get future reports

Please provide your details below to get future reports: