Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 7,153 million (3.91 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar but appreciated against the Sterling Pound and Euro to exchange at KES 144.87, KES 183.10 and KES 156.88 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | 17.38% | 0.48% |

| Sterling Pound | 23.11% | -0.49% |

| Euro | 19.16% | -0.16% |

Liquidity

Liquidity in the money markets tightened, with the average interbank rate increasing from 11.90% to 12.08%, as tax remittances more than offset government payments. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 11.90% | 12.08% |

| Interbank volume (billion) | 21.93 | 24.57 |

| Commercial banks’ excess reserves (billion) | 3.40 | 5.80 |

Fixed Income

T-Bills

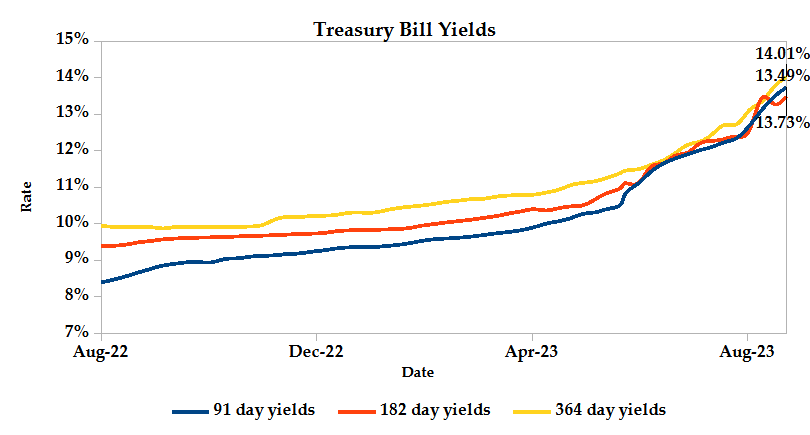

T-Bills were under-subscribed during the week, with the overall subscription rate recorded as 95.80%, down from 186.16% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 455.4% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 25.8% and 22.0% respectively. The acceptance rate decreased by 9.09% to close the week at 88.67%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover decreased by 41.02% from KES 13.86 billion in the previous week to KES 8.18 billion. Total bond deals decreased by 24.14% from 551 in the previous week to 418.

In the primary bond market, CBK released auction results for the reopened FXD1/2023/002 and FXD1/2023/005 through a tap sale which sought to raise KES 21.0 billion. The issues received bids worth KES 23.60 billion, representing a subscription rate of 112.38%. Of these, KES 23.50 billion worth of bids were accepted at a weighted average rate of 16.97% and 17.95% respectively.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average of 0.39% compared to the previous week and increased by 0.51% month to date and 0.64% year to date. The yields on the 10-year Eurobonds for Angola also declined while that of Zambia increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 0.04% | 0.46% | -1.21% |

| 2018 10-Year Issue | 1.02% | 0.68% | -0.22% |

| 2018 30-Year Issue | 0.36% | 0.38% | -0.15% |

| 2019 7-Year Issue | 0.96% | 0.58% | -0.39% |

| 2019 12-Year Issue | 0.52% | 0.51% | -0.19% |

| 2021 13-Year Issue | 0.95% | 0.47% | -0.20% |

Equities

NASI, NSE 20 and NSE 25 settled 1.94%, 0.65% and 2.11% lower compared to the previous week bringing the year-to-date performance to -21.96%, -9.13% and -18.25% respectively. Market capitalization lost 1.94% from the previous week to close at KES 1.55 trillion recording a year-to-date decline of 22.02%. The performance was driven by losses recorded by large-cap stocks such as KCB, ABSA and Safaricom of 13.45%, 6.72% and 3.13% respectively. These were however mitigated by gains recorded by EABL and Standard Chartered of 7.19% and 5.99% respectively.

The Banking sector had shares worth KES 251M transacted which accounted for 54.65% of the week’s traded value, the Manufacturing & Allied sector had shares worth KES 43M transacted which represented 9.41% and Safaricom, with shares worth KES 111M transacted represented 24.17% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Home Afrika | 0.00% | 9.68% |

| BK Group | 20.00% | 9.09% |

| E.A.B.L | -21.03% | 7.19% |

| Nairobi Business Venture | -17.51% | 6.56% |

| Standard Chartered | 9.83% | 5.99% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Williamson Tea | 28.59% | -15.59% |

| KCB | -37.94% | -13.45% |

| E.A Portland | -8.53% | -11.14% |

| Olympia | -0.68% | -9.54% |

| Kapchorua Tea | 82.51% | -9.24% |

Alternative Investments

| Losers | Week (previous) | Week (ending) | % Change |

|---|---|---|---|

| Derivatives Turnover (million) | 1.21 | 1.13 | -7.15% |

| Derivatives Contracts | 37.00 | 37.00 | 0.00% |

| I-REIT Turnover (million) | 0.58 | 0.95 | 62.41% |

| I-REIT deals | 52 | 30 | -42.31% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 15.21% | 0.82% |

| Dow Jones Industrial Average (DJI) | 3.66% | -0.45% |

| FTSE 100 (FTSE) | -2.85% | 1.05% |

| STOXX Europe 600 | 3.97% | 0.66% |

| Shanghai Composite (SSEC) | -1.68% | -2.17% |

| MSCI Emerging Markets Index | 0.88% | 0.68% |

| MSCI World Index | 11.96% | 0.50% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -5.16% | -1.35% |

| JSE All Share | -0.29% | 0.80% |

| NSE All Share (NGSE) | 27.06% | 1.26% |

| DSEI (Tanzania) | -6.80% | -0.34% |

| ALSIUG (Uganda) | -21.03% | -2.21% |

The US stock market was volatile during the week as investors weighed the prospect of further rate hikes as per comments by the Federal Reserve’s Chair relating to restrictive monetary policy to curb high inflation. Weekly figures on unemployment insurance show a tightened labour market, providing no relief for the Fed. The S&P recorded gains following investors buying into the tech dip as a result of rising Treasury yields.

European stocks closed the week in the green, boosted by a rise in energy sector stocks as they tracked high crude prices. Comments by the Fed Chair pressured equities, particularly financial services and technology stocks, as well as a rise in eurozone yields.

Asia Pacific indices edged lower during the week as investors turned risk-averse ahead of more cues on monetary policy from the Jackson Hole Symposium. Positive results from Nvidia offered some support to regional tech stocks, whose investor sentiments remain dim amid prospects of high-interest rates and worsening economic conditions.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 1.75% and 0.38% lower at $79.83 and $84.48 respectively. Gold futures prices settled 1.22% higher at $1939.90.

Week’s Highlights

- According to the State of the Banking Industry Report (SBIR) 2023 by the Kenya Bankers Association (KBA), the banking sector’s total assets grew by 8.2% to KES 6.5 trillion in 2022. This was mainly driven by a 17.70% growth in total operating income on the back of foreign exchange gains that supported income from loans, advances and investment in government securities. As part of their focus towards reducing debt vulnerabilities in the economy, the industry saw an introduction of banks’ risk-based credit pricing models and the Credit Repair Framework. In terms of outlook, the sector continues to monitor the evolution of emerging risks such as elevated inflation, concerns about public debt sustainability, fragile economic recovery and unstable global financial markets.

- The BRICS (Brazil, Russia, India, China and South Africa) bloc of major emerging countries, focused on economic development and increasing its members’ voice in global forums, held its annual summit during the week. Major deliberations included admitting Saudi Arabia, Iran, United Arab Emirates, Argentina, Egypt and Ethiopia as members effective 1st January 2024. The group now includes six of the nine largest oil producers in the world, further pushing the shift towards de-dollarization. 90% of oil sales are settled in US dollars, with Saudi Arabia, Iran and UAE, being top oil producers, likely to adopt the local currency initiative embraced by the group. The forum’s discussions also entailed unlocking intra-market access to facilitate entrepreneurship and open up new markets through the African Continental Free Trade Agreement (AfCFTA).

- Federal Reserve Chair, this week, further highlighted the need for raising interest rates further to combat inflation and bring it back to the 2% target. The decision would be based on a careful evaluation of inflation indicators, economic performance and the labour market. However, the Fed could keep interest rates steady at its September meeting, pending a comprehensive review of incoming data and evolving market conditions.

- The S&P Global US Composite PMI declined to 50.4 in August 2023, falling short of market expectations of 52.0. This was the weakest upturn in private sector activity since February. The decline was driven by a deepening contraction in the manufacturing sector as well as slower growth in service sector output. Total new orders fell for the first time in six months, and the pace of job creation eased to an over-three-year low. Inflationary pressures remained elevated, with input cost inflation quickening due to greater fuel, wage, and raw material costs. However, selling price inflation eased. Despite the slowdown in activity, US firms were more optimistic in their outlook for output over the coming year. This was fueled by hopes of a stabilization in interest rates, increased client demand, and a moderation in price pressures.

- The Eurozone Composite PMI declined to 47.0 in August 2023 from the previous month’s 48.6, falling below market expectations of 48.5. This indicates a significant deceleration in the region’s private sector since November 2020. This contraction was notable in both the manufacturing and services sectors, with manufacturing output experiencing its second-largest contraction in 11 years after the initial COVID-19 lockdowns. For the third month in a row, new orders declined at an accelerated rate, employment growth slowed, and inflationary pressures rose in terms of average selling prices and input costs. Additionally, companies’ outlook on future output levels for the next year dropped for the sixth straight month, hitting the lowest point since the previous December. The sharp contraction in private sector activity suggests that the eurozone economy is facing increasing headwinds.

- The S&P Global/CIPS United Kingdom PMI declined to 47.9 in August 2023 from 50.8 in July, falling short of market expectations of 50.3. This was the deepest pace of contraction in the country’s private sector since January 2021. The decline was primarily caused by a severe contraction in the service sector, which reached its joint-fastest pace of contraction in 31 months. The manufacturing sector also contracted, extending the current period of decline to six months. New business inflows declined the most since November 2022, and backlogs of work dropped at the fastest pace since June 2020. Private sector employment rose only slightly and at the slowest pace since March. On the pricing front, average cost burdens increased at the slowest pace since February 2021, and the inflation of prices charged moderated to its lowest level in two and a half years. Moreover, business confidence regarding year-ahead growth prospects slipped to its weakest level since December 2022. The sharp contraction in private sector activity in August suggests that the UK economy is facing increasing headwinds.

Get future reports

Please provide your details below to get future reports: