Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 7,232 million (3.80 months of import cover). This falls short of CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover as well as the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Sterling Pound and the Euro to exchange at KES 133.47, KES 166.37 and KES 142.63 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | -14.98% | 1.55% |

| Sterling Pound | -16.75% | 1.94% |

| Euro | -17.87% | 2.06% |

Liquidity

Liquidity in the money markets tightened, with the average inter-bank rate increasing from 13.71% to 13.88%, as tax remittances more than offset government payments. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 13.71% | 13.88% |

| Interbank volume (billion) | 21.13 | 20.75 |

| Commercial banks’ excess reserves (billion) | 30.4 | 22.6 |

Fixed Income

T-Bills

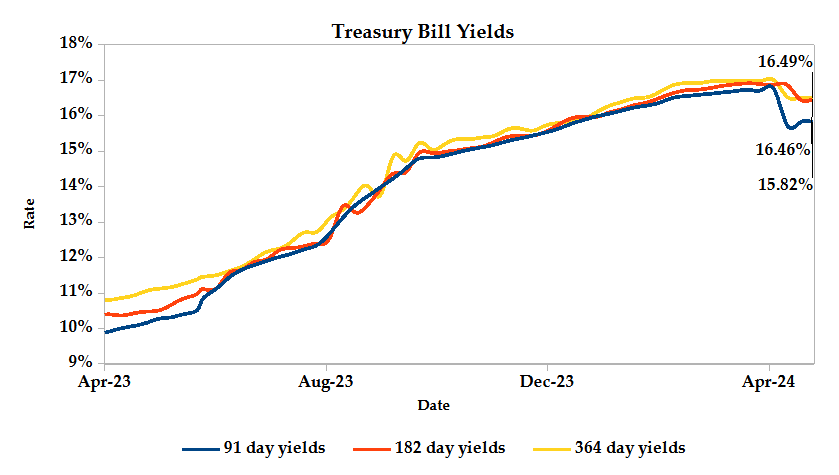

T-Bills were under-subscribed during the week, with the overall subscription rate decreasing to 98.18%, down from 108.70% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 149.65% while the 182-day T-Bill and 364-day T-Bill had subscription rates of 69.33% and 106.44% respectively. The acceptance rate decreased by 0.67% to close the week at 98.89%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 42.06%, from KES 22.31 billion in the previous week to KES 31.70 billion. Total bond deals increased by 12.73% from 652 in the previous week to 735.

In the primary bond market, CBK re-opened a 10-year bond FXD1/2024/10, targeting to raise KES 25.0 billion. The coupon rate is 16.00% and the sale runs from 25/04/2024 to 02/05/2024.

Eurobonds

In the international market, yields on Kenya’s Eurobonds increased by an average of 0.13% compared to the previous week, 0.58% month-to-date and decreased by 0.44% year-to-date. The yields on the 10-year Eurobonds for Angola and 12-Year Eurobond for Zambia increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2018 10-Year Issue | -0.88% | 0.43% | 0.13% |

| 2018 30-Year Issue | -0.21% | 0.76% | 0.02% |

| 2019 7-Year Issue | -1.18% | 0.68% | 0.16% |

| 2019 12-Year Issue | -0.20% | 0.53% | 0.14% |

| 2021 13-Year Issue | 0.25% | 0.57% | 0.15% |

| 2024 6-Year Issue | -0.43% | 0.53% | 0.17% |

Equities

NASI, NSE 25 and NSE 10 settled 0.19%, 1.31% and 2.15% higher, while NSE 20 settled 0.06% lower compared to the previous week, bringing the year-to-date performance to 16.96%, , 19.72%, 23.49% and 11.90% respectively. Market capitalization gained 0.91% from the previous week to close at KES 1.68 trillion, recording a year-to-date increase of 16.96%. The performance was driven by gains recorded by large-cap stocks such as KCB, ABSA and Stanbic of 7.87%, 4.30% and 4.22% respectively. This was however weighed down by losses recorded by Standard Chartered of 11.91%.

The Banking sector had shares worth KES 1B transacted which accounted for 74.12% of the week’s traded value, Energy and Petroleum sector had shares worth KES 78.8M transacted which represented 5.41% and Safaricom, with shares worth KES 11.8M transacted, represented 13.22% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| Sanlam | 10.00% | 10.00% |

| NBV | -2.44% | 9.59% |

| Total | 8.06% | 8.36% |

| KCB | 37.36% | 7.87% |

| EA Cables | 2.04% | 7.53% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Stanchart | 7.33% | -11.91% |

| Olympia | -5.20% | -9.62% |

| TP Serena | 11.69% | -9.48% |

| I&M Holdings | -1.15% | -9.45% |

| Transcentuary | 26.92% | -5.71% |

Alternative Investments

| Losers | Week (previous) | Week (ending) | % Change |

|---|---|---|---|

| Derivatives Turnover (million) | 3.98 | 1.90 | -52.20% |

| Derivatives Contracts | 14.00 | 19.00 | 35.71% |

| I-REIT Turnover (million) | 0.00 | 0.00 | 0.00% |

| I-REIT deals | 0.00 | 00.00 | 0.00% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 7.53% | 2.67% |

| Dow Jones Industrial Average (DJI) | 1.39% | 0.67% |

| FTSE 100 (FTSE) | 5.42% | 3.09% |

| STOXX Europe 600 | 6.16% | 1.74% |

| Shanghai Composite (SSEC) | 4.27% | 1.24% |

| MSCI Emerging Markets Index | 1.64% | 3.72% |

| MSCI World Index | 5.23% | 2.44% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -12.18% | -4.16% |

| JSE All Share | 0.03% | 3.04% |

| NSE All Share (NGSE) | 29.20% | -1.37% |

| DSEI (Tanzania) | 1.17% | 0.48% |

| ALSIUG (Uganda) | 18.37% | -0.85% |

The US stock market closed the week in the green zone, as investors digested strong earnings reports from tech giants like Alphabet and Microsoft. This positive sentiment outweighed concerns about persistent inflation, especially after inflation data confirmed the Fed’s preferred inflation gauge remained elevated.

The European stock market closed the week on an upward trajectory, buoyed by strong corporate earnings. Investor focus now shifts to Germany’s April inflation data, seen as crucial for the ECB’s upcoming interest rate decisions.

Asian stock markets closed the week on a positive note, extending their rally across most sectors. This positive momentum was fueled by optimism that China will implement more expansionary economic policies to stimulate a robust recovery in 2024, following a sluggish start to the year.

Week’s Highlights

- Kenya has secured a significant USD500 million investment from the Abu Dhabi Developmental Holding Company (ADQ), a United Arab Emirates (UAE) sovereign wealth fund, aiming to fund key projects in the region. This strategic partnership goes beyond just funding, establishing a framework for future collaboration and enabling the exploration of potential investments and joint ventures across Kenya’s diverse economy. This aligns with country’s position as a pioneer in African-UAE trade relations, having initiated bilateral trade negotiations in 2022. The deal strengthens the already robust economic ties between the two nations. Earlier in 2024, Kenya and the UAE signed a Comprehensive Economic Partnership Agreement (CEPA) to facilitate trade in various sectors, including food production, mining, technology and logistics.

- Kenya announced a partnership with Microsoft, Eco-Cloud and G42 to construct a massive 1-gigawatt (GW) data centre in Naivasha. This project positions the country as a gateway to Africa for data storage and processing, with the facility powered by clean energy from the nearby Menengai and Olkaria geothermal plants. The data centre’s strategic location capitalizes on the recently completed SGR railway line connecting Naivasha to Mombasa port, improving logistics and attracting further investment. This is evident with the launch of the first Japanese car auction in Naivasha’s Special Economic Zone, alongside interest from electric vehicle manufacturer Basigo. The project is expected to boost Kenya’s tech sector, create jobs and diversify the economy.

- Kenya Power announced an investment worth KES 258 million investment in e-mobility over the next three years. This initiative focuses on both building charging infrastructure and promoting electric vehicle adoption. Kenya Power has already launched its second charging station and allocated a budget for further expansion across the country. Additionally, they will be incorporating electric vehicles into their own operations, including heavy-duty models. This comprehensive approach positions Kenya Power as a leader in Kenya’s transition to clean transportation.

- The East African Community (EAC) has initiated plans for a 256-kilometer expressway connecting Kenya and Uganda. To assess the project’s viability and pave the way for its success, the African Development Bank (AfDB) has commissioned a USD1.5 million feasibility study to be conducted by a German-Kenyan consortium: GOPA Infra GmbH and ITEC Limited. This project aims to improve the existing Northern Corridor, a vital trade route that provides landlocked East African nations with faster access to Mombasa Port. This upgrade would transform the route from a two-lane single-carriageway to a modern dual-carriageway with improved bitumen standards.

- The HCOB Eurozone Composite PMI increased to 51.4 in April 2024 from 50.3 in March, the second consecutive month of expansion and exceeding market expectations of 50.8. This marks the strongest growth since May 2023, driven by a surge in service sector output – the fastest in 11 months. Although manufacturing production remains in contraction, the rate of decline has slowed to its weakest in a year. Notably, Germany exited its nine-month slump, while France experienced its slowest output decline in 11 months.

- The S&P Global US Composite PMI decreased to 50.9 in April 2024, down from 52.1 the previous month. This indicates a modest expansion in the country’s private sector activity, marking the softest growth since December 2023. The slowdown affected both the manufacturing and services sectors, with activity expanding at the slowest pace in three and five months, respectively. Additionally, backlogs of work declined for the third consecutive month. The rate of increase for input costs and output charges moderated but remained elevated. Finally, business sentiment fell to a five-month low.

- US GDP increased at a modest annualized rate of 1.6% in Q1 2024, marking a significant slowdown from the 3.4% growth of the previous quarter and falling short of analyst expectations of 2.5%. Consumer spending softened, with a notable decline in goods consumption of 0.4%. However, spending on services remained steady at 4%. Non-residential investment growth also eased, while government spending decreased to 1.2% from 4.6%. Trade trends pointed towards a more cautious environment, with exports growing at a slower pace and imports surging. Notably, residential investment saw a double-digit growth rate of 13.9% from 2.8% in Q4 2023.

Get future reports

Please provide your details below to get future reports: