Foreign Exchange Reserves

The usable foreign exchange reserves remained adequate at USD 7,381 million (4.13 months of import cover). This meets CBK’s statutory requirement to endeavor to maintain at least 4.0-months of import cover. However, it does not meet EAC region’s convergence criteria of 4.5-months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar and the Sterling Pound while strengthening against the Euro to exchange at KES 123.55, KES 148.56 and KES 131.09 respectively. The observed depreciation against the Dollar is attributable to increased Dollar demand from energy and commodity importers.

| YTD Change | W-o-W Change | |

|---|---|---|

| Dollar | 0.10% | 0.14% |

| Euro | -0.43% | -0.13% |

| Sterling Pound | -0.12% | 0.06% |

Liquidity

Liquidity in the money markets slightly increased with the average interbank rate dipping to 6.24% from 6.49%, as government payments offset tax remittances. Open market operations remained active.

| Week (previous) | Week (ending) | |

|---|---|---|

| Interbank rate | 6.49% | 6.24% |

| Interbank volume (billion) | 25.49 | 0.87 |

| Commercial banks’ excess reserves (billion) | 10.60 | 12.70 |

Fixed Income

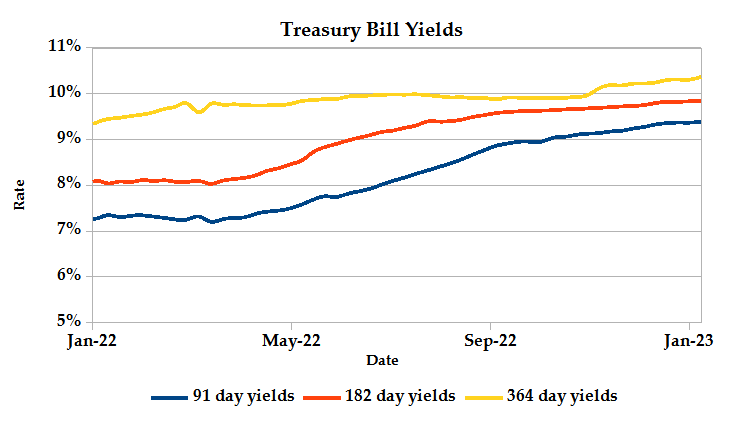

T-Bills

T-Bills were over-subscribed during the week, with the overall subscription rate coming in at 131.65% from 17.94% recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 482.94% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 77.97% and 44.83% respectively. The acceptance rate picked up 0.76% to close the week at 99.36%.

T-Bonds

In the secondary bond market, there was a lower demand for the week’s bond offers. Bond turnover dropped 17.93% from KES 2.37B in the previous week to KES 1.94B. Total bond deals declined by 13.89% from 216 in the previous week to 186.

Eurobonds

In the international market, yields on Kenya’s Eurobonds declined by an average 0.13% compared to the previous week. The yields on the 10-year Eurobond for Ghana and Angola also declined. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | -0.15% | -0.15% | -0.14% |

| 2018 10-Year Issue | -0.10% | -0.10% | -0.06% |

| 2018 30-Year Issue | -0.09% | -0.09% | -0.11% |

| 2019 7-Year Issue | -0.28% | -0.28% | -0.28% |

| 2019 12-Year Issue | -0.10% | -0.10% | -0.10% |

| 2021 13-Year Issue | -0.09% | -0.09% | -0.09% |

Equities

NASI settled 0.49% lower while NSE 20 and NSE 25 gained 1.74% and 0.67% compared to the previous week bringing the year to date performance to -0.38%, 1.79% and 0.52% respectively. Market capitalization lost 0.49% from the previous week to close at KES 1.98 trillion recording a year to date decline of 0.39%. The performance was driven by gains recorded by large-cap stocks such as Standard Chartered, EABL, KCB and Equity of 5.43%, 3.73%, 2.89% and 2.36% respectively. These were weighed down by losses recorded by Safaricom and ABSA of 2.69% and 2.03%.

The Banking sector had shares worth KES 594M transacted which accounted for 77.23% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 45M transacted which represented 5.89% and Safaricom, with shares worth KES 113M transacted represented 14.70% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| NBV | 18.27% | 23.61% |

| Trans-Century | 14.14% | 21.51% |

| EA Portland | 9.71% | 9.71% |

| Home Afrika | 2.94% | 9.38% |

| Longhorn | 8.33% | 8.33% |

| Top Losers | YTD Change | W-o-W |

|---|---|---|

| Sanlam | -17.12% | -17.12% |

| Liberty | -7.54% | -16.79% |

| Standard Group | -16.36% | -16.36% |

| Crown Paints | -8.43% | -9.20% |

| Olympia | -8.11% | -8.11% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 0.08 | 0.00 | -100.00% |

| Derivatives Contracts | 2.00 | 0.00 | -100.00% |

| I-REIT Turnover | 0.14 | 0.22 | 58.20% |

| I-REIT Deals | 22.00 | 23.00 | 4.55% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 1.86% | 1.45% |

| Dow Jones Industrial Average (DJI) | 1.49% | 1.46% |

| FTSE 100 (FTSE) | 1.92% | 3.32% |

| STOXX Europe 600 | 2.36% | 4.60% |

| Shanghai Composite (SSEC) | 1.32% | 2.21% |

| MSCI Emerging Markets | 2.71% | 3.38% |

| MSCI World Index | 1.88% | 1.81% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | -1.92% | -1.47% |

| JSE All Share | 3.58% | 5.76% |

| NSE All Share (NGSE) | -0.72% | -0.06% |

| DSEI (Tanzania) | 0.76% | 1.15% |

| ALSIUG (Uganda) | 0.00% | 0.22% |

US indices ended Friday’s session green, with S&P 500 gains led by materials, rate-sensitive technology stocks (buoyed by declining Treasury yields which continue to price in the step down interest rate changes), energy and healthcare of 3.44%, 2.99%, 1.68% and 0.89% respectively. Investors’ expectations of a less hawkish Federal Reserve were revived by an unexpected contraction of the services sector, pointing to weakness in the economy.

European stocks ended the week higher, with STOXX 600’s 4.6% gain the best performance in 9 months, boosted by miners amid higher copper prices and energy stocks supported by rising oil prices. Euro zone’s improved December optimism across all sectors and a decline in inflation expectations helped brighten sentiments.

Asia Pacific indices posted weekly gains, with markets cheering Beijing’s end to lockdowns and travel quarantine. Travel and leisure stocks continued their gains following a rather optimistic sector recovery.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 8.43% and 8.54% lower at $73.69 and $78.57 respectively. Gold futures prices settled 2.38% higher at $1,869.70.

Week’s Highlights

- Stanbic Bank Kenya’s headline PMI figure rose to a three-month high of 51.6 in December from 50.9 in November. The improvement in private sector activity reflected easing inflation as well as higher demand and favorable weather conditions. Agriculture, manufacturing, wholesale & retail sectors recorded expansion in their output while construction and services sector output fell. Output expectations fizzled amid uncertainties in the global economy that slowdown exports and business activity.

- The amendment of Capital Gains Tax charged on net gains realized from disposal of land, property, unquoted shares and buildings came into effect, tripling to 15% from the previous 5%. This comes in the wake of rising home prices in Nairobi and land costs in satellite towns as a result of renewed demand from buyers.

- NSE extended the suspension from trading of Kenya Airways Plc shares for an additional twelve months, with effect from 5th January 2023. The move seeks to allow the firm complete its operational and corporate restructure process as the government leans towards sale of its entire stake to private investors.

- World food prices declined for the ninth consecutive month in December 2022. The Food and Agriculture Organization (FAO) reported a 1.9% decline in the Food Price Index, which averaged 132.4 points in December from 134.9 in November. The drop was attributed to a steep decline in international prices of edible oils amid sluggish global import demand. For 2022, the index averaged 143.7 points, 14.3% higher than the average value over 2021.

- Euro zone inflation cooled to 9.2% year on year in December, from 10.1% in November, aided by decline in energy costs following mild weather patterns that drove down consumption. Germany’s lower inflation figure was partly attributed to their government’s relief plan that saw a one-off payment of household energy bills.

Get future reports

Please provide your details below to get future reports: