Foreign Exchange Reserves

The usable foreign exchange reserves stood at USD 7,532 million (4.15 months of import cover). This meets CBK’s statutory requirement to endeavour to maintain at least 4.0 months of import cover. The World Bank loan facility boosted reserves, lifting the coverage above the shortfall experienced since November 2022. However, it still falls short of the EAC region’s convergence criteria of 4.5 months of import cover.

Currency

The Kenyan Shilling depreciated against the Dollar, the Sterling Pound and the Euro to exchange at KES 139.22, KES 173.85 and KES 149.63 respectively. The observed depreciation against the Dollar is attributed to a high demand for the currency, which has caused a market shortage.

| Currency | YTD Change | W-o-W Change |

|---|---|---|

| Dollar | 12.80% | 0.44% |

| Sterling Pound | 16.89% | 1.45% |

| Euro | 13.65% | 1.07% |

Liquidity

Liquidity in the money markets eased, with the average interbank rate decreasing from 9.36% to 9.20%, as government payments more than offset tax remittances. Open market operations remained active.

| Liquidity | Week (previous) | Week (ending) |

|---|---|---|

| Interbank rate | 9.36% | 9.20% |

| Interbank volume (billion) | 31.79 | 14.25 |

| Commercial banks’ excess reserves (billion) | 27.70 | 28.30 |

Fixed Income

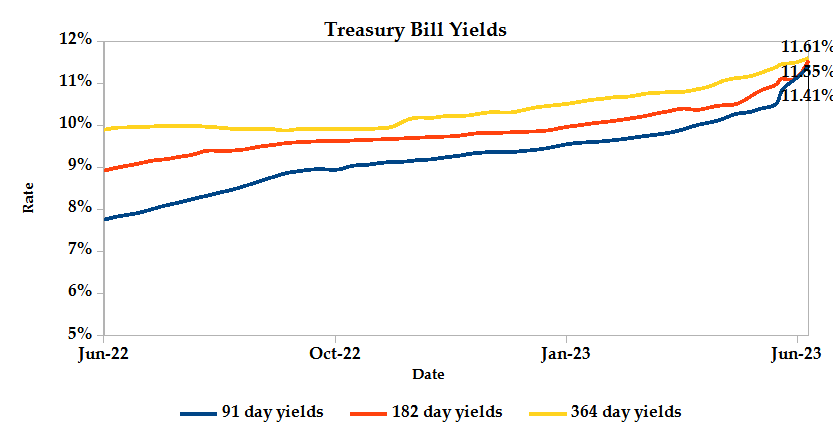

T-Bills

T-Bills were over-subscribed during the week, with the overall subscription rate recorded as 137.95%, up from 98.19% performance recorded in the previous week. The 91-day T-Bill received the highest subscription rate at 725.50% while the 182-day T-Bill and 364-day T-Bill had a subscription rate of 18.94% and 21.95% respectively. The acceptance rate increased by 10.78% to close the week at 97.06%.

T-Bonds

In the secondary bond market, there was a higher demand for the week’s bond offers. Bond turnover increased by 51.07% from KES 4.91 billion in the previous week to KES 7.41 billion. Total bond deals increased by 29.39% from 313 in the previous week to 405.

Eurobonds

In the international market, yields on Kenya’s Eurobonds decreased by an average of 0.52% compared to the previous week, 0.52% month to date and increased 0.99% year to date. The yields on the 10-Year Eurobonds for Angola declined while that of Ghana increased. Below is a summary analysis of performance for individual bonds.

| Bond | YTD Change | M-o-M Change | W-o-W Change |

|---|---|---|---|

| 2014 10-Year Issue | 1.48% | -1.13% | -1.13% |

| 2018 10-Year Issue | 1.09% | -0.38% | -0.38% |

| 2018 30-Year Issue | 0.37% | -0.29% | -0.29% |

| 2019 7-Year Issue | 1.38% | -0.66% | -0.66% |

| 2019 12-Year Issue | 0.76% | -0.33% | -0.33% |

| 2021 13-Year Issue | 0.84% | -0.35% | -0.35% |

Equities

NASI, NSE 25 and NSE 20 settled 0.70%, 2.41% and 1.46% higher compared to the previous week bringing the year-to-date performance to -16.88%, -4.86% and -12.73% respectively. Market capitalization gained 0.70% from the previous week to close at KES 1.65 trillion recording a year-to-date decline of 16.93%. The performance was driven by gains recorded by large-cap stocks such as NCBA, EABL and Stanbic of 7.84%, 6.79% and 5.01% respectively. These were however weighed down by the loss recorded by Safaricom of 2.06%.

The Banking sector had shares worth KES 336.8M transacted which accounted for 54.83% of the week’s traded value, Manufacturing & Allied sector had shares worth KES 61.7M transacted which represented 10.06% and Safaricom, with shares worth KES 167.0M transacted represented 27.19% of the week’s traded value.

Top Gainers and Losers in the Equities Markets

| Top Gainers | YTD Change | W-o-W |

|---|---|---|

| NBV | -15.48% | 30.08% |

| Longhorn | 15.33% | 15.45% |

| Sameer | 16.98% | 14.29% |

| Home Afrika | 2.94% | 12.90% |

| Umeme | 112.57% | 11.97% |

| Losers | YTD Change | W-o-W |

|---|---|---|

| Eveready | 125.00% | -6.90% |

| Car & General | -48.98% | -5.48% |

| Unga | -40.63% | -5.00% |

| Safaricom | -30.98% | -2.06% |

| TPS | -4.62% | -0.80% |

Alternative Investments

| Week (previous) | Week (ending) | % Change | |

|---|---|---|---|

| Derivatives Turnover (million) | 1.03 | 0.83 | -22.99% |

| Derivatives Contracts | 27 | 18 | -50.00% |

| I-REIT Turnover (million) | 0.22 | 0.16 | -67.74% |

| I-REIT deals | 47 | 56 | -32.00% |

Global and Regional Markets

| Global Markets | YTD Change | W-o-W |

|---|---|---|

| S&P 500 | 12.41% | 0.39% |

| Dow Jones Industrial Average (DJI) | 2.24% | 0.34% |

| FTSE 100 (FTSE) | 0.11% | -0.59% |

| STOXX Europe 600 | 5.95% | -0.46% |

| Shanghai Composite (SSEC) | 3.40% | -0.24% |

| MSCI Emerging Markets Index | 4.13% | 1.83% |

| MSCI World Index | 10.95% | 0.43% |

| Continental Markets | YTD Change | W-o-W |

|---|---|---|

| FTSE ASEA Pan African Index | 0.80% | -0.86% |

| JSE All Share | 4.74% | -0.54% |

| NSE All Share (NGSE) | 8.40% | 0.19% |

| DSEI (Tanzania) | -2.62% | -0.12% |

| ALSIUG (Uganda) | -13.71% | 0.14% |

US indices edged higher this week, fueled by Tesla Inc’s impressive performance, achieving its longest winning streak since January 2021, following the strategic partnership with General Motors to access their supercharging network. Tech companies such as Apple, Advanced Micro Devices and Nvidia also saw share price increases. The rally in mega-cap stocks, driven by stronger-than-anticipated earnings, coupled with the belief that the Federal Reserve is nearing the end of its rate-hiking cycle, provided support to Wall Street amidst concerns of a potential recession and persistent inflation.

European stock markets declined this week, as rate-sensitive technology shares and export-heavy consumer staples underperformed, reflecting concerns about potential interest rate hikes by major central banks. The telecommunication sector was negatively impacted by a significant drop in Vodafone shares, further contributing to the overall downturn. Furthermore, concerns deepened over the economic recovery in China, a key growth driver for the region and a crucial export market for numerous European companies, due to weak inflation data.

Asian Pacific indices ended the week on a downward trajectory, as traders exercised caution with riskier assets ahead of the upcoming Federal Reserve meeting. Market sentiment remained divided on whether the central bank would raise or maintain interest rates, given mixed signals concerning the state of the U.S. economy. Furthermore, the persistent decline in imports raised concerns about the sustainability of China’s economic recovery amidst weakened global demand for its goods.

On the global commodities markets, Crude Oil WTI and ICE Brent Crude closed the week 2.19% and 1.76% lower at $70.17 and $74.79 respectively. Gold futures prices settled 0.39% higher at $1977.20.

Week’s Highlights

- Kenya has shortlisted four banks, namely Citigroup, JP Morgan, Standard Bank and Standard Chartered Bank, as potential lead arrangers for its planned return to the global financial markets in the 2023/2024 fiscal year. This move is aimed at alleviating pressure in settling its forthcoming $2.0 billion Eurobond maturity. The selection process commenced in April, initiated by the Treasury’s request for expressions of interest from international lead managers to oversee the issuance of a sovereign bond. Economic challenges, including unfavorable global financial conditions and rising yields, led the government to postpone its initial plan of issuing another Eurobond in the current financial year.

- The Stanbic Kenya PMI reached a four-month high of 49.4 in May 2023, indicating a slight improvement but still reflecting the fourth consecutive month of contraction. Despite a softer decline in output and new orders, sales were adversely affected by the cost of living crisis and limited purchasing power. However, firms managed to slightly increase inventories as a precautionary measure against potential price hikes and supply shortages. Stockpiling efforts were supported by improved supplier delivery times for the second consecutive month. Additionally, hiring activity picked up in May, resulting in the fastest growth in employment numbers since November 2021.

- Old Mutual, Zimele and CIC have secured regulatory approval from the Retirement Benefits Authority (RBA) to handle Tier II contributions from employers who opt out of the National Social Security Fund (NSSF). These contributions will be managed through Old Mutual Pensions, Zimele Personal Pension Plan & Zimele Guaranteed Personal Pension Plan and CIC Umbrella & CIC Jipange Retirement Benefit Schemes.

- The Organisation for Economic Co-operation and Development’s (OECD) June Economic Outlook indicates a modest improvement in the global economy, although the recovery is expected to be weak. The 2023 GDP growth forecast has been slightly revised upward to 2.7%, while the outlook for 2024 remains unchanged at 2.9%. The report highlights ongoing risks, including the war in Ukraine and inflation concerns. Factors that aided energy demand reduction this year, like a mild European winter, may not be repeated next year. The US economy is projected to grow at 1.6% in 2023, slowing to 1% in 2024 due to tight monetary and financial conditions. In the Eurozone, declining inflation is expected to boost real incomes and contribute to an increase in GDP growth. China is anticipated to experience strong GDP growth following the lifting of the zero-COVID policy.

- The Food and Agriculture Organization (FAO) Food Price Index reached a 2-year low of 124.3 in May 2023, with notable declines in vegetable oil and cereal prices. Vegetable oil prices fell for the 6th consecutive month, driven by decreases in palm, soy, rapeseed and sunflower oils. The decline in cereal prices was attributed to declined wheat prices. On the other hand, meat prices rose for the 4th consecutive month, driven by increased demand for poultry and bovine meat. Sugar prices extended their upward trend, amidst concerns over the impact of the El Niño phenomenon on future crops and lower-than-expected global availabilities.

- The S&P Global US Composite PMI remained stable at 54.3 in May 2023, indicating the fastest expansion in business activity in over a year. The service sector was the main driver of growth, compensating for weaker manufacturing production. Despite a significant decline in overseas goods trade, total new business continued to rise, employment showed solid growth and backlogs of work decreased. Additionally, there was a relief in inflationary pressures.

- The Eurozone Composite PMI was revised downward to 52.8 in May 2023, signalling a growth slowdown with the weakest expansion in three months. Manufacturing production declined sharply, while services activity continued to grow at a slower rate. Total new business almost stagnated, with export sales falling for the 15th consecutive month. Job creation remained solid but weaker than in April. Cost pressures eased and business sentiment weakened to a five-month low.

- In the UK, the Bank of England raised the bank rate to 4.5% in May 2023, marking the twelfth consecutive increase as part of the fight against double-digit inflation. Borrowing costs reached their highest level since 2008. The central bank expects inflation to decrease to 5.1% in Q4 2023 and aims to achieve the 2% target by late 2024. The economy is projected to stall in Q1 and Q2 but is anticipated to grow by 0.25% in 2023, showing improvement compared to the previous contraction. Government budget measures are expected to contribute 0.5% to GDP. Policymakers will closely monitor signs of persistent inflationary pressures, including labor market conditions, wage growth and services price inflation. Further monetary policy tightening may be necessary if evidence of sustained pressures emerges.

Get future reports

Please provide your details below to get future reports: